Personal Injury Protection, or PIP, is a type of no-fault car insurance that pays for your own medical bills and lost wages after a crash, regardless of who caused it. In 15 jurisdictions, drivers are required to purchase PIP, and in a standard policy such as Minnesota's, coverage often provides up to $40,000 per person per accident, split into $20,000 for medical costs and $20,000 for non-medical costs like lost wages.

Right after a crash, people involved aren't thinking about insurance theory. They're thinking about the ambulance bill, the ER discharge papers, the missed shift, the childcare they can't manage, and the stack of forms already starting to grow on the kitchen counter.

That's where PIP matters. If you're asking what is personal injury protection coverage, the practical answer is this: it's often the first money available to keep your life from sliding further off track while the larger injury claim unfolds. Before any lawsuit, before settlement talks, before the at-fault driver's insurer accepts anything, your own PIP benefits may be the first source of payment for treatment and basic financial stability.

PIP can also be confusing fast. Coverage rules change by state. Billing coordination with health insurance can go wrong. A paperwork mistake can delay benefits you need now, not months from now. If you're sorting out treatment bills in Oregon, this guide for Oregon accident medical costs gives a useful overview of how those expenses often start piling up after a wreck.

Your First Financial Lifeline After a Crash

A crash creates two problems at once. There's the injury itself, and then there's the money problem that starts immediately.

PIP is financial first aid. It steps in through your own auto policy and pays certain accident-related expenses without making you prove the other driver was at fault first. That no-fault structure is the reason PIP matters so much in the first days and weeks after a collision.

Why PIP matters so early

The at-fault driver's liability carrier usually doesn't move fast enough to protect you from immediate fallout. Bills arrive anyway. Your doctor still expects payment. Your employer still tracks missed time. If your injuries keep you from driving, cleaning, or caring for your kids, life gets more expensive, not less.

PIP is designed for that gap.

In many situations, it applies to you and your passengers, and in some jurisdictions it can also extend to pedestrians or bicyclists hit by a car. That makes it broader than many people expect. It isn't just a policy add-on. It can be the first step in preserving your financial footing after an accident.

Practical rule: Use PIP first if it's available under your policy. It exists to handle immediate economic losses while fault and liability are still being sorted out.

What's at stake if it's mishandled

A bad start with PIP can create problems that spread through the rest of the injury case. Unpaid providers may send bills to collections. Wage loss documents can go missing. Health insurance may reject bills that were supposed to go through auto coverage first. Then you're not just recovering from injuries. You're fixing preventable administrative damage.

That's why understanding what personal injury protection coverage is really means understanding what it does in real life. It buys time, keeps treatment moving, and helps prevent a short-term crisis from becoming a long-term financial mess.

What PIP Insurance Actually Covers and Excludes

The day after a crash often looks the same. The ER bill posts before fault is decided. A physical therapist wants insurance information. Your employer asks when you can return. PIP is the part of the auto policy meant to keep those early expenses from turning into missed treatment, credit damage, or pressure to settle too cheaply.

PIP usually pays specific economic losses caused by the collision. It works before the liability claim is resolved, and that timing matters. In practice, I tell clients to treat it as the first payment source for accident-related bills if their policy or state law makes it available, because mistakes at this stage can spill into the health insurance claim and the injury case later.

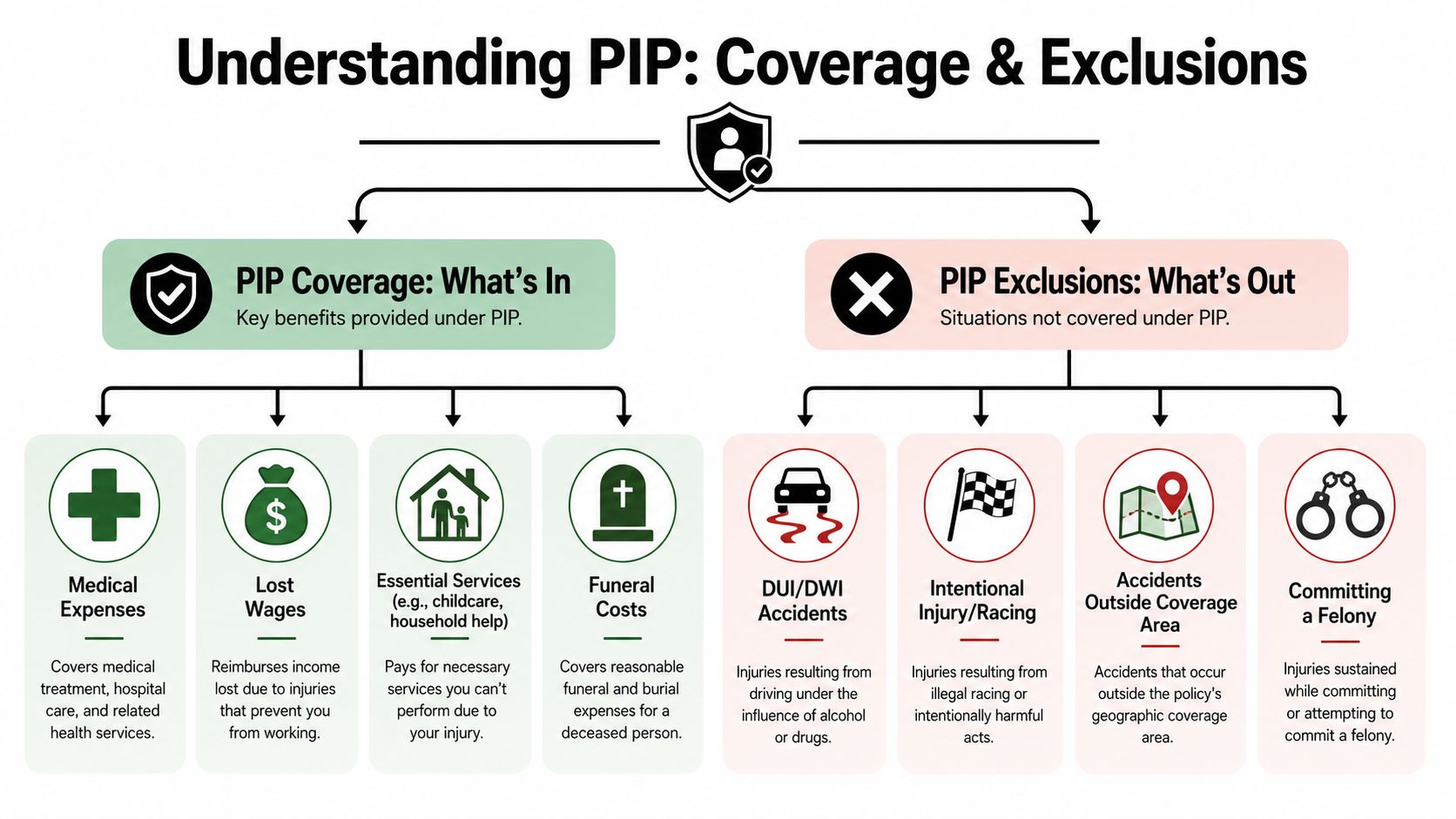

What PIP usually pays for

The exact benefits depend on the policy and the state, but PIP often includes:

- Medical treatment: Ambulance charges, emergency care, doctor visits, diagnostic testing, rehabilitation, and other reasonable accident-related treatment. The Insurance Information Institute explanation of no-fault and PIP coverage outlines the kinds of medical expenses PIP commonly addresses.

- Lost income: If injuries keep you from working, PIP may pay part of your wage loss for a limited period.

- Replacement services: Some policies pay for outside help with tasks you ordinarily handled yourself, such as housekeeping, transportation, or similar day-to-day duties.

- Childcare or dependent care: In some states and under some policies, PIP can pay for care you need because your injuries prevent you from handling it yourself.

- Funeral expenses: Many PIP systems include a death benefit or burial-related benefit after a fatal crash.

Some states define these benefits broadly. Others keep them narrow, cap them quickly, or tie payment to strict treatment rules. If you are trying to figure out how these rules work in a no-fault framework, this explanation of whether Colorado is a no-fault state helps show why people get confused about PIP from one state to another.

One more practical point matters here. PIP and health insurance do not always pay in the same order. Some health plans require auto coverage to be billed first for crash injuries. Some providers bill the wrong carrier, then treatment gets delayed or denied. That is how a manageable claim becomes an administrative mess.

What PIP does not cover

PIP pays bills tied to injury. It usually does not pay for the full range of losses that follow a serious wreck.

PIP generally does not cover:

- Vehicle repairs: Property damage is usually handled through collision coverage or the at-fault driver's property damage liability coverage.

- Pain and suffering: PIP focuses on measurable financial losses, not noneconomic damages.

- The other driver's injuries or losses: Your PIP is for covered people under your policy or under the state's no-fault rules, not for the person who hit you.

- Every medical bill without limits: Deductibles, payment caps, utilization review rules, and deadlines can all reduce what gets paid.

- The full value of your injury case: If another driver caused the crash, a liability claim may still be necessary to recover damages PIP does not pay.

That last point is where people get hurt financially. A client sees some bills paid and assumes the insurance problem is handled. It usually is not. PIP may keep treatment going and wages partially replaced, but it does not measure long-term suffering, permanent impairment, future care, or the full income loss from a major injury.

Florida is a good example of how state-specific these limits can be. If you want a state-focused overview, Florida personal injury protection explains how one no-fault system handles early injury expenses.

The trade-off that matters

PIP gives speed. It also gives only limited relief.

That trade-off is the part many injured drivers miss. Quick access to some benefits can protect your finances in the first days and weeks after a crash. It does not remove the need to document treatment carefully, coordinate with health insurance, and preserve the liability claim if another driver was at fault.

How PIP Rules Change from State to State

Two drivers can walk away from nearly identical crashes and face completely different insurance rules before the first medical bill even arrives. That difference often starts with state law, not the injury.

PIP is one of the most state-specific parts of auto coverage. In one state, it is the first source of payment for medical care and lost wages. In another, it is optional and easy to overlook on the declarations page. In a third, it is not part of the system at all.

Why the state matters right away

State rules control more than whether PIP exists. They shape who must file with their own insurer first, what benefits are available, how quickly notice must be given, and when an injured person can step outside the no-fault system and pursue the at-fault driver for more damages.

That changes strategy from the first week after a crash. A person with mandatory PIP usually needs to open that claim promptly to keep treatment and wage-loss benefits moving. A person in an optional-PIP state may learn, only after the collision, that the coverage was rejected years ago. And in a state without a traditional PIP system, health insurance, MedPay, and the liability claim often take on a larger role immediately.

A few states show how different the rules can be

| State | PIP Mandatory? | Typical Starting Point | Why It Matters |

|---|---|---|---|

| Florida | Yes | State-specific limits and conditions apply | Early medical expenses often run through PIP first. This Florida personal injury protection overview gives a useful state-specific explanation. |

| Texas | No, but must generally be offered | Often offered at a modest default amount | Many drivers do not know whether they rejected it in writing until they request the policy after a crash. |

| Kentucky | Yes | State-specific no-fault structure | Benefit levels and options can affect how much immediate help is available. |

| Minnesota | Yes | Baseline benefits set by statute | The coverage structure includes separate categories and caps that can affect payment timing. |

| New York | Yes | Mandatory no-fault benefits | The claim process is paperwork-heavy, and deadlines can cause real payment problems. |

| Colorado | No traditional PIP system | Not applicable | Colorado uses a different liability-based framework. |

Texas, Colorado, and New York create different practical problems

Texas is a good example of why policy review matters. PIP is not mandatory there in the same way it is in a classic no-fault state, but it is commonly offered unless the insured rejects it. After a crash, that single detail can determine whether there is immediate money for treatment while the liability case develops.

Colorado presents a different issue. Drivers there are not working within a traditional PIP system, so the first layer of financial recovery may come from health insurance, MedPay, or a claim against the at-fault driver. If you need a quick explanation of that distinction, this guide on whether Colorado is a no-fault state explains the framework clearly.

New York shows the other side of the problem. Benefits may be available, but they do not pay themselves. Strict forms, notice requirements, and medical documentation often decide whether bills get covered on time or get denied and pushed elsewhere.

The practical effect on your injury claim

The critical question is how your state defines PIP, who qualifies for it, what it pays first, and what deadlines control the claim.

That is not a technical insurance point. It affects the whole recovery path. If PIP should have paid first and the claim is delayed, providers may bill health insurance incorrectly, send balances to collections, or pressure you for payment while you are still treating. If your state limits lawsuits unless the injury meets a threshold, a weak early PIP file can also hurt the liability case later.

A good starting point is simple. Check the declarations page, confirm the state rules that apply to the crash, and find out immediately whether PIP, MedPay, health insurance, or the at-fault driver's coverage should be paying first. People get into trouble when they assume the term "PIP" means the same thing everywhere.

A Step by Step Guide to Using Your PIP Benefits

PIP works best when you treat it like a live claim file from day one. Small delays can create billing problems that are hard to unwind later.

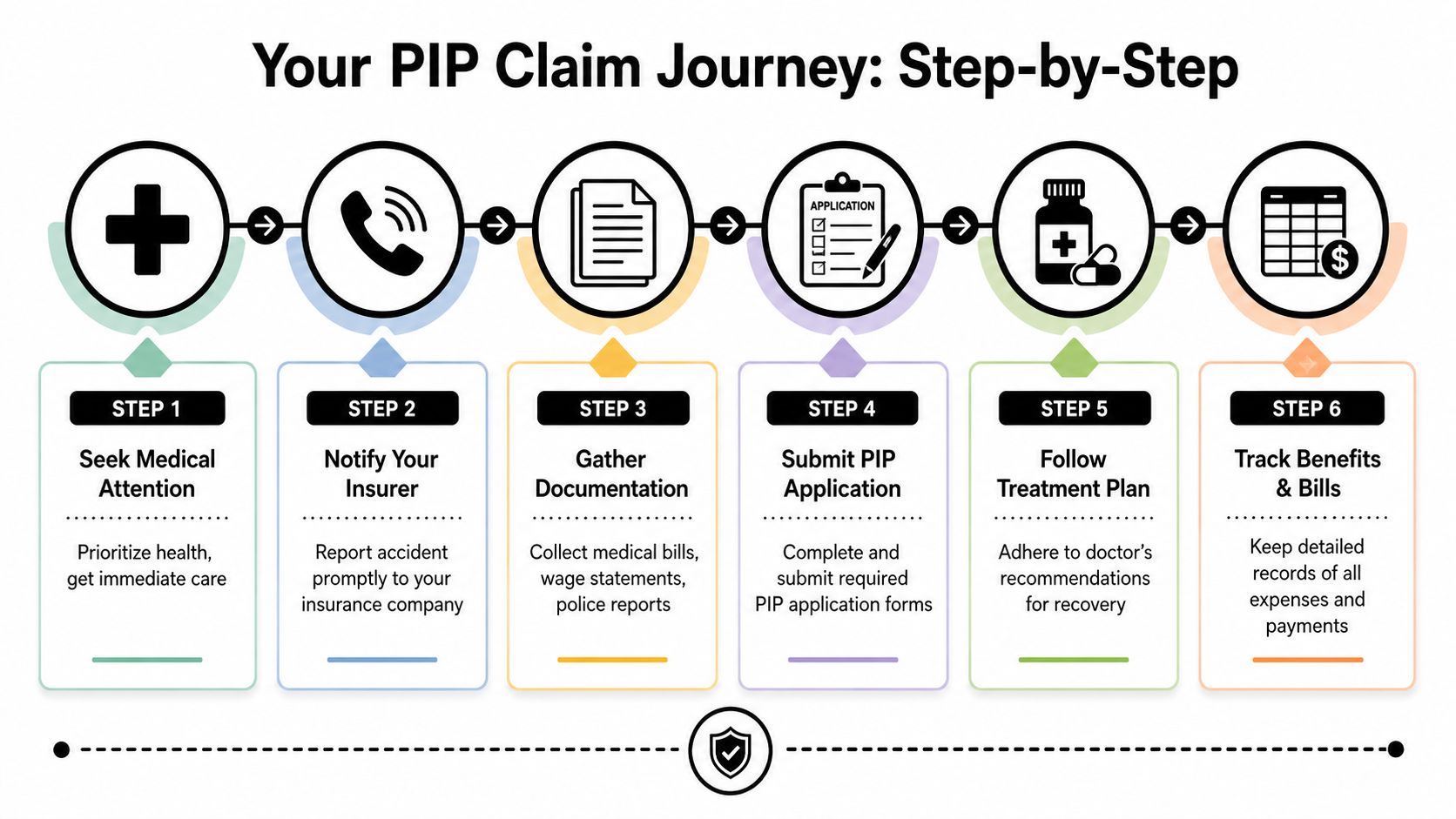

Start with medical care and notice

Your first move is medical attention. If you need emergency care, get it. If your symptoms show up later, get evaluated anyway. Prompt treatment protects your health, and it also creates the records that tie your injuries to the crash.

Then notify your own insurer quickly. Don't wait until bills pile up. Tell them there was a collision, you were injured, and you want to open any available PIP claim.

Build the claim file carefully

After the claim opens, focus on paperwork. At this stage, many valid claims start to wobble.

- Complete the PIP application fully. Don't guess. If you don't know an answer, say that and follow up with the correct information.

- Gather every accident-related record. That usually includes medical bills, discharge papers, work notes, wage verification, and any crash report available.

- Keep copies of everything. If you send a document once and the adjuster says it never arrived, you need to be able to resend it fast.

- Use writing whenever possible. Email creates a record of what you reported, when you sent it, and what the insurer said back.

If you want a sense of how insurers evaluate claims generally, this overview of an insurance company investigation helps explain why complete documentation matters so much.

Track bills and wage loss as they happen

PIP claims aren't one-and-done. Treatment continues. Wage loss may continue too. That means your file needs ongoing maintenance.

Use a basic folder system, digital or paper, with separate sections for:

- Medical bills

- Explanation of benefits forms

- Prescription receipts

- Doctor work-status notes

- Payroll records and missed-time verification

- Insurer letters and emails

Keep this simple: If a bill, note, or receipt relates to the crash, save it the same day.

What works and what usually backfires

What works is consistency. Report promptly, submit documents as they come in, and follow your treatment plan.

What backfires is silence. If you miss appointments, ignore insurer requests, or let providers bill the wrong carrier for months, the claim gets harder to fix. PIP is often available to help quickly, but it still requires active management.

Common PIP Claim Pitfalls and Costly Mistakes

Most denied or delayed PIP claims don't fall apart because the injury was fake. They fall apart because billing, coordination, or documentation went sideways.

The PIP exhaust problem

One of the least understood issues is PIP exhaust. In Massachusetts, if you have private health insurance, your auto insurer may cover only the first $2,000 in bills, and mishandling that handoff can lead to denials and major out-of-pocket exposure, as explained in this discussion of Massachusetts PIP exhaust.

That's not a small technicality. It affects who gets billed first, who pays next, and whether a provider later claims the wrong carrier was responsible. When that coordination fails, injured people can end up caught in the middle while each insurer points at the other.

If your treatment providers don't understand the billing order, correct it early. A preventable billing mistake can follow a case for months.

PIP doesn't only apply inside the car

Another common misunderstanding is thinking PIP applies only if you were sitting in the vehicle at the moment of impact. In some states and policy structures, coverage can extend to pedestrians or bicyclists struck by a motor vehicle, and in certain jurisdictions it can also protect resident relatives and passengers, as described in this GEICO explanation of PIP basics.

That matters because people sometimes fail to open a valid claim at all. They assume they were “outside the car,” so PIP can't help. That assumption can cost time and money.

Other mistakes that hurt the whole injury case

Some errors don't just weaken the PIP claim. They damage the larger personal injury case too.

- Giving broad recorded statements too early: Adjusters often ask questions before you understand the full extent of your injuries.

- Poor wage-loss proof: If you're paid hourly, self-employed, or miss intermittent time, your losses need careful support.

- Settling before treatment patterns are clear: Early pressure to “wrap things up” can leave later bills unpaid.

- Ignoring reimbursement issues: If one insurer pays bills another carrier should have paid, disputes can arise later. If you need a plain-English explanation of how reimbursement fights work, this guide on what is a subrogation claim is worth reading.

The practical takeaway

The biggest PIP mistakes usually come from treating it like a simple add-on benefit. It isn't. It sits at the intersection of auto insurance, health insurance, wage loss proof, and the future liability case.

What works is early organization and careful billing coordination. What doesn't is assuming the system will sort itself out.

When to Call an Attorney for Your PIP Claim

Some PIP issues are routine. Others are warning signs that the case is already moving beyond what one should handle alone.

Situations that usually justify legal help

Call an attorney if your insurer delays payment, denies treatment, disputes wage loss, or keeps asking for the same documents without making a decision. Those patterns often signal a claim that needs pressure and structured advocacy.

Legal help also makes sense when injuries are serious enough that available benefits may run out quickly. The more complex the medical picture, the more important it becomes to protect both the immediate benefit claim and the larger liability case.

You should also get guidance when more than one coverage source may apply. PIP, private health insurance, workers' compensation, and liability coverage don't always cooperate cleanly. When they overlap, mistakes get expensive.

Why timing matters

Many people wait until there's a formal denial. That can be too late. By then, deadlines may be close, providers may be unpaid, and the paper trail may already be messy.

An attorney can help by:

- Reviewing the policy language

- Identifying claim deadlines

- Coordinating billing and records

- Pushing back on wrongful denials

- Protecting the separate injury claim against the at-fault driver

The right time to get help is often when the claim becomes confusing, not when it becomes hopeless.

PIP is only one part of recovery

Even when PIP works properly, it usually addresses only the front-end financial damage. A full injury claim may still involve long-term treatment, liability disputes, and damages beyond what PIP pays. For a broader patient-centered look at how injury claims affect recovery, these insights on injury claims offer a helpful perspective.

If you're spending more time fighting paperwork than focusing on medical recovery, that's a strong sign the process needs legal support.

Your First Step Toward Financial Recovery

PIP can be one of the most useful parts of an auto policy after a crash. It gives injured people a way to access payment for immediate economic losses through their own coverage instead of waiting for a liability fight to play out.

But useful doesn't mean simple. State rules differ. Billing coordination can break down. Wage-loss proof has to be done correctly. A mistake at the beginning can ripple through the rest of the case.

If you came here asking what is personal injury protection coverage, the practical answer is this: it's often the first financial bridge between the crash and your recovery. Used properly, it helps you get treatment, keep records straight, and avoid preventable financial damage while the larger injury claim develops.

If the process feels overwhelming, or if the insurer is making it harder than it should be, get guidance early. The sooner you understand your coverage and protect the claim, the better position you'll be in to recover physically and financially.

If you were hurt in a crash and need clear answers about PIP, liability insurance, or unpaid medical bills, Nares Law Group LLC can help you understand your options and protect your rights. A free consultation can give you clarity on what coverage applies, what steps to take next, and how to avoid costly mistakes while your case is still taking shape.