It’s one of the first questions drivers ask after a crash, and the answer is critical. So let's get right to it: No, Colorado is not a no-fault state.

We operate under what’s known as an “at-fault” or “tort” system. In simple terms, this means the driver who caused the collision is financially responsible for the harm they caused.

Understanding Colorado’s At-Fault Car Accident System

Knowing that Colorado is a fault-based state directly shapes what you can do after an accident. It gives injured people the right to demand full compensation from the driver whose carelessness turned their life upside down. This is a world away from how no-fault systems work.

Think of it this way. In a no-fault state, your own insurance policy acts like a first-aid kit, paying your initial medical bills no matter who was to blame. In Colorado, however, the person who made the mess is expected to clean it up. Their liability insurance is on the hook for the damages you’ve suffered.

Key Differences At a Glance

This distinction isn't just a technicality—it changes everything. In Colorado, you aren’t restricted to the limits of your own insurance policy for your injuries. You have the right to file a claim or lawsuit against the at-fault driver to cover the full extent of your losses.

The entire principle of Colorado’s at-fault law is built on accountability. The driver who caused the accident is responsible for the consequences, including the medical bills, lost income, and pain and suffering of those they hurt.

To make this even clearer, here’s a simple breakdown of how the two systems handle a claim.

Colorado's At-Fault System vs No-Fault Insurance

| Feature | Colorado's At-Fault System | Traditional No-Fault System |

|---|---|---|

| Who Pays for Injuries? | The at-fault driver's liability insurance covers the victim's damages. | Your own Personal Injury Protection (PIP) insurance covers your initial medical bills. |

| Right to Sue | Victims can file a lawsuit against the at-fault driver for full damages. | The right to sue is often restricted unless injuries meet a certain "severity threshold." |

| Claim Focus | Proving the other driver was negligent and caused the accident. | Filing a claim with your own insurer to access your pre-paid benefits. |

At the end of the day, Colorado’s at-fault rules put more power in the hands of injured people. They create a clear path for you to hold a negligent driver accountable and recover the compensation you truly need to put your life back together.

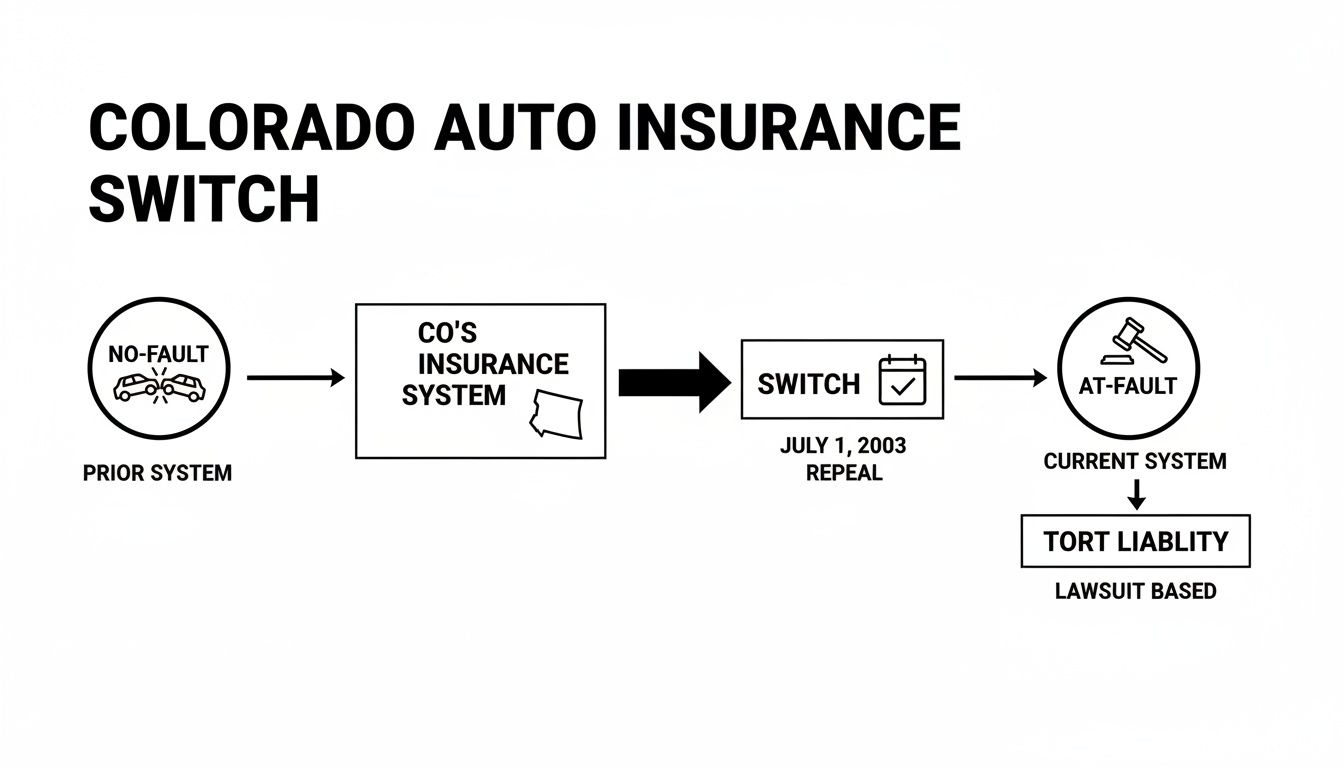

Why Colorado Ditched Its No-Fault System

It’s hard to imagine now, but for almost three decades, Colorado handled car accidents completely differently. From 1974 all the way to 2003, we were a "no-fault" state. If you were injured in a crash, you had to turn to your own insurance company first, no matter who was to blame.

So what happened? Why the dramatic change?

The original idea behind no-fault was to keep small injury claims out of court and get money into victims' hands faster. But in reality, the system created a whole new set of problems for everyday Coloradans, with one standing out above the rest: runaway insurance costs that became some of the highest in the country.

Think of the old no-fault law like this: every driver was forced to buy their own separate, expensive first-aid kit. After a crash, you weren’t allowed to get help from the person who hurt you; you could only use your own kit, even if it wasn't your fault at all.

A System That Penalized Good Drivers

This setup, while well-intentioned, backfired. Because everyone’s own policy paid for their initial injuries, there was no immediate financial consequence for the driver who actually caused the crash. This created a system that felt fundamentally unfair and, ultimately, became unsustainable.

The biggest issues were:

- Skyrocketing Premiums: The mandatory Personal Injury Protection (PIP) coverage became incredibly expensive, driving up rates for everyone—including the safest drivers on the road.

- Lack of Accountability: The system effectively shielded negligent drivers from the initial financial fallout of their actions, placing the burden on the victim’s policy instead.

- New Inefficiencies: Instead of simplifying things, the law just shifted the arguments. Fights erupted over what medical care was "reasonable and necessary," creating delays and new administrative headaches.

The financial strain on Colorado families and individuals simply became too much. Lawmakers saw that the system wasn't delivering on its promise and decided a complete overhaul was needed to give drivers some relief.

Returning to Common-Sense Accountability

On July 1, 2003, Colorado officially repealed its no-fault law. We moved to the tort-based, "at-fault" system we have today—a change designed to restore personal responsibility and lower costs for consumers.

The effect was immediate. State records revealed that drivers saw an average premium reduction of 22% right after the switch, based on filings from the state's largest insurance carriers. You can even find details about these post-reform rate decreases from the Colorado Division of Insurance.

The switch from no-fault to at-fault wasn’t just a policy change; it was a return to a core principle. The person who causes the harm should be the one responsible for fixing it.

This shift gave power back to crash victims. It affirmed their right to seek full and fair compensation directly from the at-fault driver's insurance. It ensures that careless drivers—not their victims—are held accountable for the damage they cause.

How Colorado's At-Fault System Actually Works

So, what does it actually mean for you that Colorado is an “at-fault” state? In simple terms, it means the person who causes a car crash is responsible for the harm that follows. This is sometimes called a “tort” system, and it’s built on a fundamental idea: accountability.

Instead of being forced to turn to your own insurance for limited medical coverage, you have the right to seek full compensation from the driver who was negligent. This isn't just about covering some of your ER bills. It's about recovering everything you've lost—from the cost of your damaged car and ongoing physical therapy to the wages you couldn't earn and the real, human toll of your pain and suffering.

Understanding Modified Comparative Negligence

Of course, real-world accidents are rarely black and white. Sometimes, the fault isn't all on one person. Colorado law recognizes this reality with a rule called Modified Comparative Negligence.

Think of it like a pie. After a crash, a jury or insurance adjuster will determine how to slice up the responsibility. If you’re found to be partially at fault, your final compensation is reduced by that percentage. For example, if you have $100,000 in damages but are found 20% responsible, your award would be cut by $20,000, leaving you with $80,000.

But there’s a sharp, unforgiving cutoff.

Under Colorado law (C.R.S. § 13-21-111), if your share of the fault is determined to be 50% or more, you get nothing. You are completely barred from recovering any compensation at all. This 50% bar is exactly why insurance companies fight so hard to shift even a tiny sliver of blame onto an injury victim.

This is a critical concept, and you can learn more about how comparative fault in Colorado can make or break your case.

As this graphic shows, Colorado made a deliberate choice to move to this system, leaving the old "no-fault" model behind on July 1, 2003.

This change was all about putting responsibility back where it belongs: on the driver who caused the collision.

Why State Minimum Insurance Is Rarely Enough

For an at-fault system to offer any real protection, drivers must carry liability insurance. The problem is, Colorado's legal minimums are dangerously low and haven't been updated to reflect the staggering cost of modern medical care.

Every driver is required to have at least this much coverage:

- $25,000 for bodily injury to one person in one crash.

- $50,000 for total bodily injuries if multiple people are hurt.

- $15,000 for property damage.

Let that sink in for a moment. A single MRI and a short hospital stay can easily burn through the entire $25,000 bodily injury limit. If the driver who hit you only has minimum coverage, you could be left with a mountain of medical debt, even after you’ve proven they were 100% at fault.

This gap is precisely why your own Uninsured/Underinsured Motorist (UIM) coverage is one of the most important purchases you can make. It’s often the only safety net you have when the other driver’s policy comes up short.

What to Do Immediately After a Car Accident in Colorado

The moments after a crash are a blur of adrenaline and confusion. It’s hard to think straight. But what you do next is critical, especially since Colorado’s at-fault system means every action can affect your ability to get compensation later. Your first priority is always your health, followed closely by protecting your legal rights.

Check on yourself and everyone in your car. If anyone seems hurt or the crash looks serious, call 911 right away. If you can, move your vehicle out of traffic to a safer spot, but never, ever leave the scene of the accident.

Document Everything at the Scene

Once you've made sure everyone is as safe as possible, your role shifts. You need to become an evidence collector. The information you gather in these first few minutes is the foundation for proving fault. Your smartphone is the best tool you have.

Start taking pictures and videos of everything. Don't hold back.

- Vehicle Damage: Get close-ups of the damage on all vehicles involved. Then, step back and capture wider shots showing where the cars ended up.

- The Surrounding Area: Photograph traffic lights, stop signs, slick roads, skid marks, and any debris scattered on the pavement. These details tell a story.

- Injuries: If you have any visible cuts, scrapes, or bruises, take pictures of them immediately.

Next, you'll need to exchange information with the other driver. Get their full name, address, phone number, and—most importantly—their insurance company and policy number. If anyone stopped to help or saw what happened, ask for their contact info. An unbiased witness account can be incredibly powerful.

Even if the other driver seems apologetic and admits they were at fault, do not rely on a verbal promise. Get their insurance details. People often change their story after they’ve had a chance to talk to their insurance company.

Protect Your Legal and Financial Interests

After you’ve documented the scene, a few more steps can protect you from common mistakes that insurance companies often use against injured people. Always report the crash to the police. A formal police report creates an official, third-party record of the incident, which is vital for your claim.

When you talk to anyone at the scene, including the police officer, stick to the facts. It’s natural to want to be polite, but avoid saying things like "I'm so sorry" or "I didn't see you." These simple phrases can be twisted to sound like an admission of fault.

You’ll also need to notify your own insurance company that an accident happened; it's a requirement in most policies. Give them the basic facts, but you should not give a recorded statement until you've spoken with an attorney. You are under no obligation to speak with the other driver’s insurance adjuster. Their job is to find ways to pay you as little as possible.

For a more in-depth look at what to do, we’ve put together a helpful personal injury case checklist for Colorado injury claims.

Getting Fair Compensation Isn’t Automatic

Knowing Colorado is an at-fault state is one thing. Actually getting the money you’re owed from the other driver’s insurance company is another thing entirely. This isn’t about just filling out paperwork. It's a fight.

Your primary route for compensation is a third-party claim filed against the at-fault driver's liability insurance. You’re the “third party” in this equation, and their policy exists to cover the harm their driver caused. This is where the process begins.

But don’t expect the other driver’s insurance company to just write you a fair check. Their business model is built on paying out as little as possible. Their goal is to protect their profits, not to make you whole.

Getting Your Medical Bills Paid Right Away

While you’re building your case against the at-fault driver, medical bills can show up with terrifying speed. This is where your own insurance policy can throw you a lifeline. In Colorado, your own insurer is required to offer you Medical Payments (MedPay) coverage.

MedPay is a no-fault feature of your own policy. You can use it immediately—regardless of who was at fault—to cover ambulance rides, ER visits, and co-pays. Think of it as your policy’s first-aid kit. It gives you some financial breathing room so you can focus on healing while your larger claim moves forward.

Many people mistakenly believe they can only use one insurance policy. The reality is, a successful claim often means using both: your MedPay for immediate costs and the at-fault driver's liability policy for your total damages.

This two-track approach lets you get the medical care you need without delay, all while holding the person who hurt you responsible for the full extent of the harm they caused—including your pain and suffering.

How Insurance Companies Try to Undercut Your Claim

The insurance adjuster for the other driver is not your friend. Their job is to find ways to pay you less. Since the question of is colorado a no fault state is settled (it's not), their strategy shifts from denying fault to downplaying the value of your injuries.

They rely on a few classic moves:

- The Delay Game: They might go silent for weeks or claim they "lost" your paperwork. They're hoping financial pressure will force you to accept a ridiculously low offer out of desperation.

- The Recorded Statement Trap: An adjuster will ask to record a call with you, hoping you'll say something—anything—they can use to pin some of the blame on you. Even an innocent "I'm sorry it happened" can be twisted.

- The Lowball Offer: They’ll often make a fast, cheap offer, trying to close your case before you even know how serious your injuries are or what future medical care you might need.

These tactics are designed to prey on your vulnerability after a crash. Standing up to them requires a firm grasp of your rights and a clear-eyed view of what your claim is actually worth, which is always more than just the first stack of medical bills.

Hiring an experienced personal injury lawyer completely changes this dynamic. Your attorney becomes your shield, handling the adjusters while they build a powerful case based on evidence. They calculate your true damages—not just medical costs and lost wages, but the real-world impact on your life. An attorney forces the insurer to the negotiating table, and the final settlement is often multiples higher than the company's initial insulting offer.

Common Questions After a Colorado Car Accident

Once you understand the basics of Colorado's at-fault system, the real-world “what ifs” start to surface. The path forward can feel foggy, but getting clear answers to your most urgent questions is the first step toward protecting yourself and your family.

Navigating the aftermath of a crash is about more than just pointing a finger. It’s about knowing how to handle the messy, complicated situations that life throws at you. Let's walk through a few of the most common scenarios we see.

What Happens if the At-Fault Driver Has No Insurance?

It’s a situation every driver dreads, and for good reason. When the person who caused your injuries doesn't have insurance, your own policy becomes your primary lifeline. This is precisely why Uninsured/Underinsured Motorist (UM/UIM) coverage is so important.

While UM/UIM coverage is optional in Colorado, choosing to add it to your policy is one of the most powerful things you can do to protect your financial future.

- How it works: Your UM coverage acts as a stand-in for the at-fault driver's missing insurance. You file a claim with your own insurance company to cover your medical bills, lost income, and pain and suffering, right up to your policy limits.

- Without UM coverage: Your options become incredibly narrow. You could sue the uninsured driver directly, but the hard truth is that someone who can't afford insurance rarely has the assets to pay a judgment. This can leave you holding the bag for all the costs.

Considering that an estimated 16.2% of Colorado drivers were uninsured in recent years, hoping the other driver is covered is a major gamble.

Key Takeaway: Strong Uninsured/Underinsured Motorist coverage isn't just a nice-to-have; it's a critical safety net. It’s the insurance you buy to protect yourself when the other driver hasn't done the responsible thing.

How Long Do I Have to File a Car Accident Claim in Colorado?

Colorado has a firm deadline for filing a lawsuit after a car accident. This deadline is called the statute of limitations. For most car accidents that cause injuries, you have three years from the date of the crash to file your claim.

Three years might sound like a lot of time, but it disappears fast when you're focused on doctor's appointments, treatment, and just trying to get your life back. It is absolutely crucial to respect this deadline.

If you miss that three-year window, you permanently lose the right to seek compensation for your injuries. It doesn't matter how clear the fault is or how serious your injuries are; the court will reject your claim. For a closer look, you can learn more about the statute of limitations for personal injury in Colorado and the nuances that might apply to your case.

Does My Health Insurance Pay for Car Accident Injuries in Colorado?

Yes, your health insurance is a vital piece of the puzzle, but it’s rarely the first to pay. Think of it as a specific payment order designed to use all available resources efficiently.

Here's the typical sequence of how bills get paid:

- Medical Payments (MedPay) Coverage: The first place you turn is your own auto policy's MedPay coverage. It provides immediate, no-fault benefits to cover your initial medical expenses up to your chosen limit.

- Health Insurance: After your MedPay is used up, your personal health insurance takes over. It will cover your ongoing treatment costs, but you'll still be responsible for your deductibles and co-pays.

- The At-Fault Driver's Policy: The end goal is to make the at-fault driver's liability insurance pay for everything, which includes paying back your health insurer.

This brings up a critical term: subrogation. It’s your health insurer's legal right to get reimbursed for the money they spent on your medical care. They will place a lien on your final settlement to recover those costs. An experienced personal injury attorney can often negotiate these liens down, ensuring more of the settlement money stays in your pocket, where it belongs.

Navigating an at-fault claim takes experience, patience, and a deep understanding of how insurance companies operate. If you've been hurt and feel overwhelmed by the process, the team at Nares Law Group LLC is here to bring clarity and fight for the full compensation you are owed. Contact us for a free, no-obligation consultation to discuss your case by visiting nareslawgroup.com.