The crash itself is chaotic enough. You check for injuries, talk to police, exchange information, call family, and try to calm down while your car sits crooked in the roadway.

Then the second hit lands. The driver who caused the wreck has no insurance, or not enough of it.

That moment creates a very specific kind of panic. People usually ask the same questions: Who pays the medical bills? What happens to my lost income? Why is my own insurance company suddenly asking so many questions if I'm the one who got hurt?

An uninsured motorist settlement is supposed to be the answer to that problem. But in Colorado, getting paid isn't as simple as showing your declarations page and waiting for a check. These claims are often technical, document-heavy, and full of avoidable procedural mistakes. The hard part is not just having coverage. The hard part is using it correctly.

The Aftermath of a Crash with an Uninsured Driver

A common scene after a serious wreck looks like this: the at-fault driver admits fault at the roadside, the police report gets started, and you assume the insurance process will move forward the way people expect it to. Then you learn the other driver has no liability coverage at all. What felt like a straightforward injury claim suddenly turns into a fight over your own policy.

That situation is not rare. The problem is growing. As of 2023, more than one in seven drivers nationwide, 15.4%, are uninsured, and insured drivers absorb nearly $13 billion every year in financial burden from uninsured and underinsured crashes, according to the Insurance Information Institute's uninsured motorist facts.

Why this feels backwards

It is a common expectation that the uninsured driver presents the legal problem. Often, the immediate legal problem is proof.

Your own insurer may open a UM claim, but that doesn't mean it accepts your injuries, your treatment, your wage loss, or the value of your pain and suffering. In practical terms, the claim can feel less like a safety net and more like a second round of litigation.

Practical rule: A UM claim is still an injury claim. You still have to prove fault, prove damages, and prove why the amount you're requesting is justified.

What injured people usually need first

Right after this kind of wreck, the priority is clarity. Start with these basics:

- Get medical care promptly. Delays give insurers room to argue that you weren't hurt badly or that something else caused the symptoms.

- Report the crash fully. Police reports, photos, and witness details matter more in UM claims than many people realize.

- Notify your insurer carefully. You need to open the claim, but you also need to avoid casual statements that can later be used to minimize it.

- Preserve every paper trail. Bills, prescriptions, work records, repair estimates, and treatment notes become the spine of your settlement demand.

When the at-fault driver has no coverage, your UM policy is supposed to step in. But the path from opening the claim to receiving a fair uninsured motorist settlement depends on understanding exactly what that coverage does and where the traps are.

Understanding Your Uninsured Motorist Coverage in Colorado

Think of uninsured motorist coverage and underinsured motorist coverage as the backup parachute in your own policy. You hope you never need it. But if the other driver has no insurance, or too little insurance to cover the damage they caused, that backup can be the difference between manageable recovery and long-term financial strain.

Colorado requires insurers to offer UM/UIM coverage equal to your bodily injury liability limits. The minimum framework matters, but so does the actual cost of injury care. In Colorado, insurers must offer this protection at limits equal to your bodily injury liability coverage, and the state minimum is $25,000 per person. A single emergency room visit can exceed that amount, which is why higher limits often matter more than people realize, as explained in this Colorado UM/UIM coverage overview.

How the limits actually work

Insurance policies often use split limits. If your declarations page shows $25,000 per person / $50,000 per accident, that means one injured person can recover up to the per-person limit, while the policy has a separate total cap for everyone injured in the same crash.

That structure confuses many people because they read the page as if the numbers stack automatically. They don't work that way by default. The numbers are limits, not promises.

If you want a clearer breakdown of how these benefits work, this guide to Colorado uninsured motorist coverage is a useful starting point.

The difference between UM and UIM

UM applies when the at-fault driver has no insurance. UIM applies when the at-fault driver has some insurance, but not enough.

Here's the practical version. If the other driver carries liability coverage and that money runs out before your losses are fully covered, your UIM claim may pick up the remaining damages up to your own policy limit. Colorado's framework creates a two-layer recovery path. First from the at-fault driver's policy, then from your own UIM coverage for the uncompensated portion, if the claim is handled correctly.

Your own policy is not extra money floating above the case. It is a contract with conditions, limits, and deadlines. If you ignore those conditions, the backup coverage can disappear when you need it most.

What works and what doesn't

A few patterns show up repeatedly in Colorado UM/UIM claims:

What works

- Reading the declarations page early. You need to know the available limits before strategy decisions get made.

- Treating UIM as procedural. If another insurer is involved, coordination matters.

- Looking beyond the minimum. Low limits can vanish quickly in any case involving imaging, specialist care, or ongoing treatment.

What doesn't

- Assuming your insurer will explain every available option. Carriers explain policy language through their own lens.

- Accepting another driver's limits too fast. That can create problems if your own carrier's rights aren't protected.

- Confusing coverage with entitlement. Coverage opens the door. It doesn't prove value.

The biggest mistake I see is simple: people think buying UM coverage means they've already won half the battle. In reality, the fight usually starts after the claim is opened.

Building Your Claim with Strong Evidence and Documentation

Many injured people are shocked when they learn this part: you are not automatically entitled to your policy limits. Colorado carriers require evidence showing why your claim is worth the amount you demand, and a strong package with itemized medical expenses, verified lost wages, and clear proof of injury gives you the best chance at a settlement that reflects the actual loss, as described in this Colorado UM claim documentation discussion.

That's the hidden burden in an uninsured motorist settlement. Your own insurer may already know the other driver was uninsured. It may still challenge the amount owed.

Economic damages need paperwork

Economic damages are the losses you can usually tie to a document, invoice, bill, or wage record. If the file is thin, the offer is usually thin too.

Here is the core evidence I want clients thinking about early:

Medical charges and records

Emergency care, imaging, orthopedic visits, physical therapy, prescriptions, and future treatment recommendations all matter. Bills alone are not enough. Records must also connect the treatment to the crash.Lost income proof

Wage loss often gets undervalued because people rely on a verbal estimate. Better proof includes pay stubs, tax records, employer letters, missed-day summaries, and, for self-employed people, invoices or prior earnings records.Property loss documents

Repair estimates, photos, total-loss paperwork, and out-of-pocket transportation costs help show the practical impact of the crash.

Non-economic damages need a story supported by facts

Pain, disruption, sleep loss, headaches, anxiety while driving, inability to lift a child, difficulty sitting through work, canceled plans, reduced mobility. Those harms are real, but they are easier for adjusters to minimize because they don't arrive in a neat invoice.

A good uninsured motorist settlement demand doesn't just say you're suffering. It shows how the injury changed daily life.

Keep a simple journal. Short entries about pain levels, missed activities, medication side effects, and work limitations can make your claim more credible because they create a timeline insurers can't easily dismiss as hindsight.

Types of Recoverable Damages in a UM Claim

| Damage Category | What It Includes |

|---|---|

| Medical expenses | Emergency treatment, hospital care, follow-up visits, rehabilitation, prescriptions, and other accident-related care |

| Lost wages | Missed pay, reduced hours, and documented income loss tied to your injuries |

| Property damage | Vehicle repair or replacement costs and related property loss |

| Pain and suffering | Physical pain, emotional distress, inconvenience, and reduced enjoyment of daily life |

| Future losses | Future medical care or reduced earning capacity when supported by evidence and policy terms |

Documentation that strengthens a demand package

A persuasive demand package usually includes more than a stack of records. It organizes the claim so the adjuster can follow the evidence from collision to consequence.

Helpful materials often include:

- A liability summary that explains why the uninsured driver caused the crash.

- A treatment chronology showing what care you received and when.

- A wage-loss section with supporting employment records.

- Photographs of vehicle damage, visible injuries, and recovery aids.

- A narrative of daily impact that connects the records to real limitations.

This is one of the places where legal help can materially change a case. Some people build these packages themselves. Others use counsel, medical billing support, or firms such as Nares Law Group LLC to assemble records, coordinate providers, and present a claim in a form insurers can't easily brush aside.

Poor documentation invites delay. Good documentation narrows the insurer's room to argue.

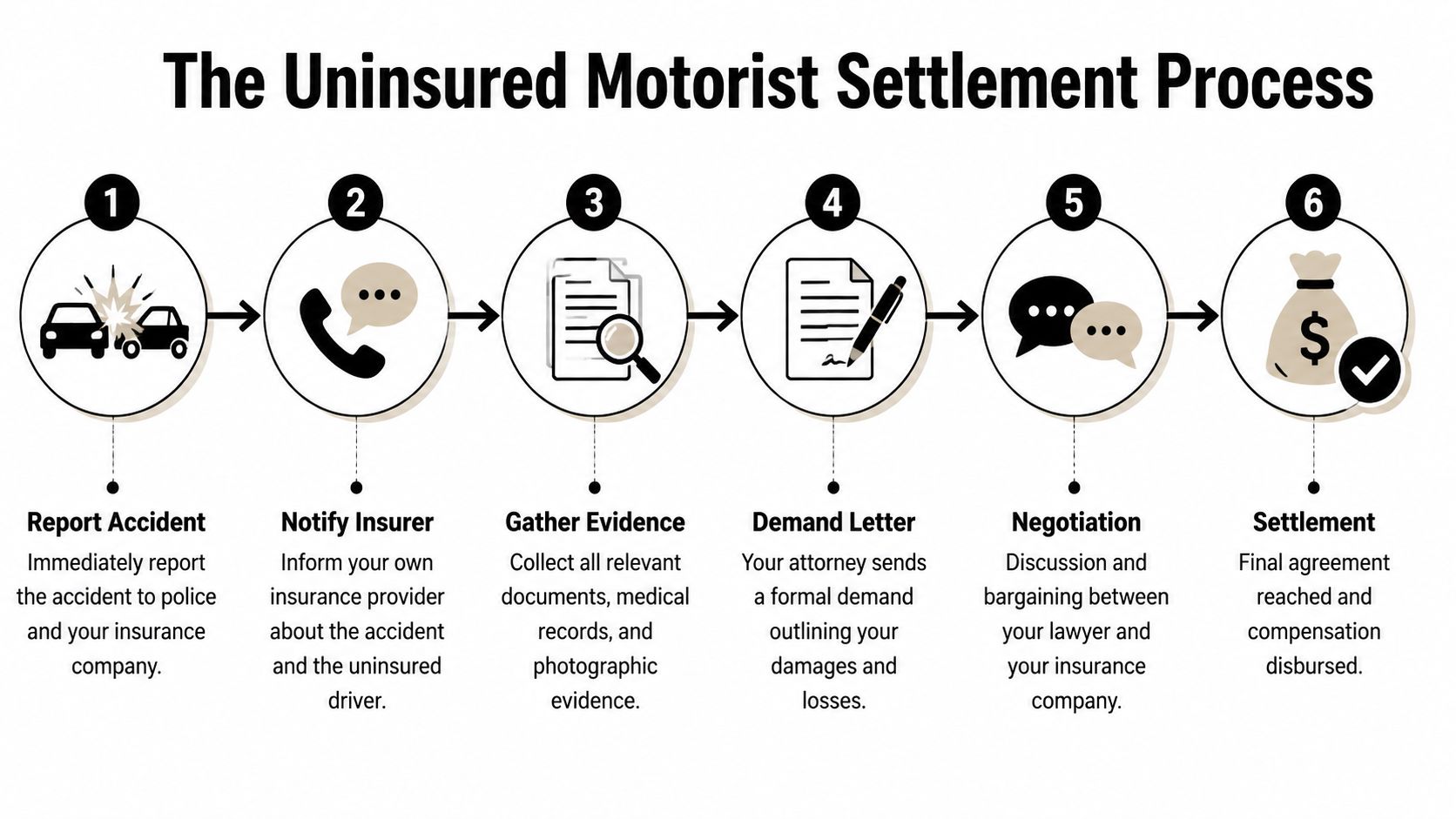

The Uninsured Motorist Settlement Process Step by Step

The uninsured motorist settlement process is easier to manage when you stop viewing it as one giant dispute and start viewing it as a sequence. Each stage has a purpose. Each stage also has a risk if handled casually.

Here's the process flow many Colorado claims follow.

Step one through three

Report the collision

Start with the police report, scene photos, witness information, and prompt notice to your carrier. Early accuracy matters. Small inconsistencies can become big defense themes later.Open the UM or UIM claim

Your insurer needs notice that the at-fault driver had no insurance or inadequate insurance. If you're unsure how much to say to an adjuster in the opening phase, this article on dealing with insurance after a car accident addresses the practical communication issues that often come up.Build the evidence file

This stage usually takes longer than people expect. Treatment has to unfold. Records have to arrive. Wage information has to be verified. A claim sent too early often undervalues future care and ongoing symptoms.

A short visual overview can help if you prefer to see the process laid out before diving into strategy.

Step four through six

Send the demand package

This is the formal presentation of your claim. It typically includes liability facts, medical treatment, economic losses, non-economic damages, and the amount demanded to settle.Negotiate from evidence, not frustration

Insurers rarely respond by paying the demand outright. They review records, ask questions, challenge causation, and compare your evidence to the policy limits. Productive negotiation usually means answering weak points with stronger proof, not repeating that the offer feels unfair.Resolve or escalate

If negotiations produce a fair result, the claim settles. If not, the case may move toward arbitration or litigation, depending on the policy language and disputed issues.

The procedural trap Colorado drivers miss

Colorado UIM claims contain one mistake that can destroy value quickly. If the at-fault driver has some liability coverage and you plan to accept that settlement, you must protect your UIM rights first.

If you settle with the at-fault driver before getting your UIM carrier's written permission, you can lose your ability to recover the additional compensation your own policy might have provided.

That rule catches people because the settlement with the other driver feels like progress. Legally, it can also cut off the second layer of recovery if done in the wrong order. Before any release is signed, the UIM carrier's position needs to be addressed.

What slows the process down

Some delays are normal. Others are warning signs. Common sticking points include:

- Gaps in treatment

- Incomplete wage proof

- Disputes over pre-existing conditions

- Premature settlement discussions before medical improvement is clear

- Authorization or release language that goes too far

A calm, methodical file usually settles better than a rushed one. Speed helps only when the evidence is already there.

What Is a Fair Uninsured Motorist Settlement Value

The question everyone asks is the right one. What is a fair uninsured motorist settlement?

There isn't a formula that works across every case. The value depends on the injuries, the treatment, the wage loss, the long-term consequences, and the coverage available. Typical UM settlement payouts range from $10,000 to $100,000, while severe cases can exceed $250,000 or more, according to this overview of uninsured and underinsured motorist claim values.

What pushes value up

Cases generally move higher when the evidence shows a clear and lasting impact. The strongest value drivers usually include:

- More serious injuries that require substantial treatment or leave lasting limitations

- Higher medical costs supported by records, bills, and physician recommendations

- Documented lost income rather than rough estimates

- Daily life disruption that can be shown through treatment notes, testimony, and consistent reporting

- Future consequences such as ongoing care or reduced ability to work

A settlement offer should make sense in light of the whole picture, not just one medical bill total.

What caps the claim

The biggest ceiling in many UM cases is not the severity of the injury. It is the policy limit.

That can be frustrating because a person may have damages far beyond the available coverage. In that situation, the legal value of the case and the collectible value of the case are not always the same thing. If your policy limit is lower than the full damage picture, the practical recovery may stop there unless another source of coverage exists.

A fair settlement is not just about proving you were hurt. It's about proving the full scope of loss within the boundaries of the insurance contract.

A realistic way to evaluate an offer

When clients assess an offer, I usually suggest three questions:

- Does the offer account for all treatment tied to the crash?

- Does it reflect verified income loss and future impact, if those are part of the case?

- Is the insurer discounting the claim because of actual evidence problems, or because it expects you to give up?

A low offer isn't automatically bad faith. Sometimes it reflects weak documentation. Sometimes it reflects aggressive claim handling. The important part is knowing which problem you're dealing with before you decide whether to push back or settle.

Navigating Negotiations and When to Consider a Lawsuit

UM claims often surprise people because the opposing negotiator may be their own insurance company. That feels personal, and in a way it is. You paid premiums for protection. Now the carrier is evaluating how little it can pay while still closing the file.

That doesn't mean every adjuster is acting unfairly. It does mean you should expect scrutiny.

Common ways insurers reduce value

Insurers often focus on the same pressure points:

- They question medical causation. If you had prior back pain, prior headaches, or any treatment gap, they may argue the crash didn't cause the current complaints.

- They minimize the duration of symptoms. They may accept that you were hurt, but only briefly.

- They use quick offers to create urgency. Early money can be tempting when bills are piling up.

- They attack wage-loss claims. This is especially common for self-employed workers, gig workers, and anyone with variable income.

The right response depends on the reason for the dispute. If the disagreement is really about missing proof, fix the proof. If the carrier has the proof and still won't value the case fairly, stronger action may be necessary.

When a lawsuit becomes the right tool

A lawsuit is not the first move in most uninsured motorist settlement disputes. It becomes appropriate when negotiation has stopped being productive.

Consider escalation when:

- The insurer denies a claim despite solid liability evidence

- The offer ignores significant documented damages

- The carrier relies on strained causation arguments unsupported by the record

- Repeated requests for review produce delay without meaningful movement

If your carrier has denied or sharply undervalued the claim, this guide on appealing an insurance claim denial may help you understand the next practical steps.

Litigation alters strategic advantage. It allows formal discovery, sworn testimony, and judicial oversight. It also requires time, discipline, and a clear file. The strongest lawsuits are usually built long before the complaint is filed.

Frequently Asked Questions About UM Settlements

Does UM coverage apply in a hit-and-run case

It often can, because hit-and-run crashes may function like uninsured driver cases when the at-fault driver cannot be identified. The details matter. Prompt reporting, scene evidence, witness information, and consistency in the account become especially important.

Can I use UM coverage for damage to my car

That depends on the policy language and the type of coverage involved. In many cases, vehicle damage is addressed under collision coverage rather than bodily injury UM benefits. The declarations page and the specific policy terms control that answer.

Do I need a lawyer if the other driver was clearly uninsured

Not always, but legal help becomes much more important when injuries are significant, treatment is ongoing, wage loss is disputed, or the insurer is pushing a procedural issue. Clear fault does not guarantee a fair payout.

What deadline applies to a UM claim in Colorado

Deadlines can depend on the policy, the nature of the claim, and whether litigation becomes necessary. Because timing rules can be claim-ending, the safest move is to review the policy and get case-specific advice as early as possible.

Should I talk to the adjuster myself

You can, but be careful. Even ordinary statements about pain levels, prior injuries, work restrictions, or treatment plans can later be used to narrow value. If the claim is more than minor, it helps to approach those communications strategically.

If you were hurt by an uninsured or underinsured driver in Colorado, Nares Law Group LLC helps injured people evaluate coverage, avoid procedural mistakes, document damages, and pursue compensation through settlement or litigation. A good UM claim is built with evidence, timing, and careful attention to the policy terms. Getting clear guidance early can prevent mistakes that are hard to undo later.