A subrogation claim is what happens after your insurer pays a covered loss and then steps into your shoes to get that money back from the person or company that caused the harm. In real life, that process matters because subrogation recoveries in healthcare typically range between 0.2% and 0.3% of total health insurance costs, yet for the 5% to 6% of claims that are accident-related, recovery efforts can still hit an injured person's settlement hard.

Consider this scenario: Your insurer pays a bill that should never have existed if another driver had been careful. Then your insurer turns around and says, “We want reimbursement from the one who caused this.” That sounds reasonable until you realize the money they want back may come out of the same settlement you were counting on to pay your own bills, replace lost income, and stabilize your life.

If you're reading this because you got a letter with the word “subrogation” in it, you're not behind. You're in the same position a lot of injured people find themselves in. They've done the hard part. They reported the crash, treated with doctors, missed work, answered adjuster calls, and then an official-looking notice arrives from a health plan, auto carrier, or benefits administrator demanding information or repayment.

That letter can feel invasive, confusing, and a little threatening. It often uses technical language on purpose. But the issue underneath it is simple. Someone paid part of your loss, and now they want to recover that money. The question is whether they legally can, how much they can claim, and what that means for your wallet.

Your Accident and the Letter You Did Not Expect

A common version goes like this. You were rear-ended in Denver. Your car went to a body shop. Your MedPay or health insurance covered treatment while you tried to get better. Weeks later, maybe months later, you receive a letter from a company you've never heard of, or from your own insurer, asking about the crash, the other driver, and whether you expect a settlement.

Your first reaction is usually one of these:

- Confusion: Why is my own insurance company asking for money?

- Panic: Am I being accused of doing something wrong?

- Frustration: I'm injured. Why am I dealing with another claim?

All three reactions make sense.

The word subrogation sounds like something designed to keep regular people out of the conversation. But most of the time, the letter is not saying you committed fraud or that your case is in trouble. It's saying the insurer believes it has a right to be repaid if you recover money from the at-fault party.

Why this catches people off guard

Most accident victims assume the only real fight is with the driver who caused the crash and that driver's insurance company. That's only part of it. Once your own coverage or your health plan starts paying bills, another financial player enters the picture.

That's why post-accident insurance communication needs to be handled carefully. If you're already sorting through adjuster calls, repair estimates, and medical billing, it helps to understand how to deal with insurance after car accident issues before you answer every letter on autopilot.

Most subrogation problems get worse when injured people assume the notice is routine paperwork and sign or respond too quickly.

What the letter is really telling you

Strip away the formal language and the message is usually this:

| What the letter says | What it means in plain English |

|---|---|

| We paid benefits related to your accident | We spent money on your claim |

| We may have subrogation rights | We may demand reimbursement |

| Please provide settlement details | We want to track any money you recover |

| Do not impair our rights | Don't sign away claims without understanding the consequences |

That last point matters more than is often realized. A subrogation issue isn't just paperwork in the background. It can affect the amount you keep when your case ends.

What a Subrogation Claim Really Means for You

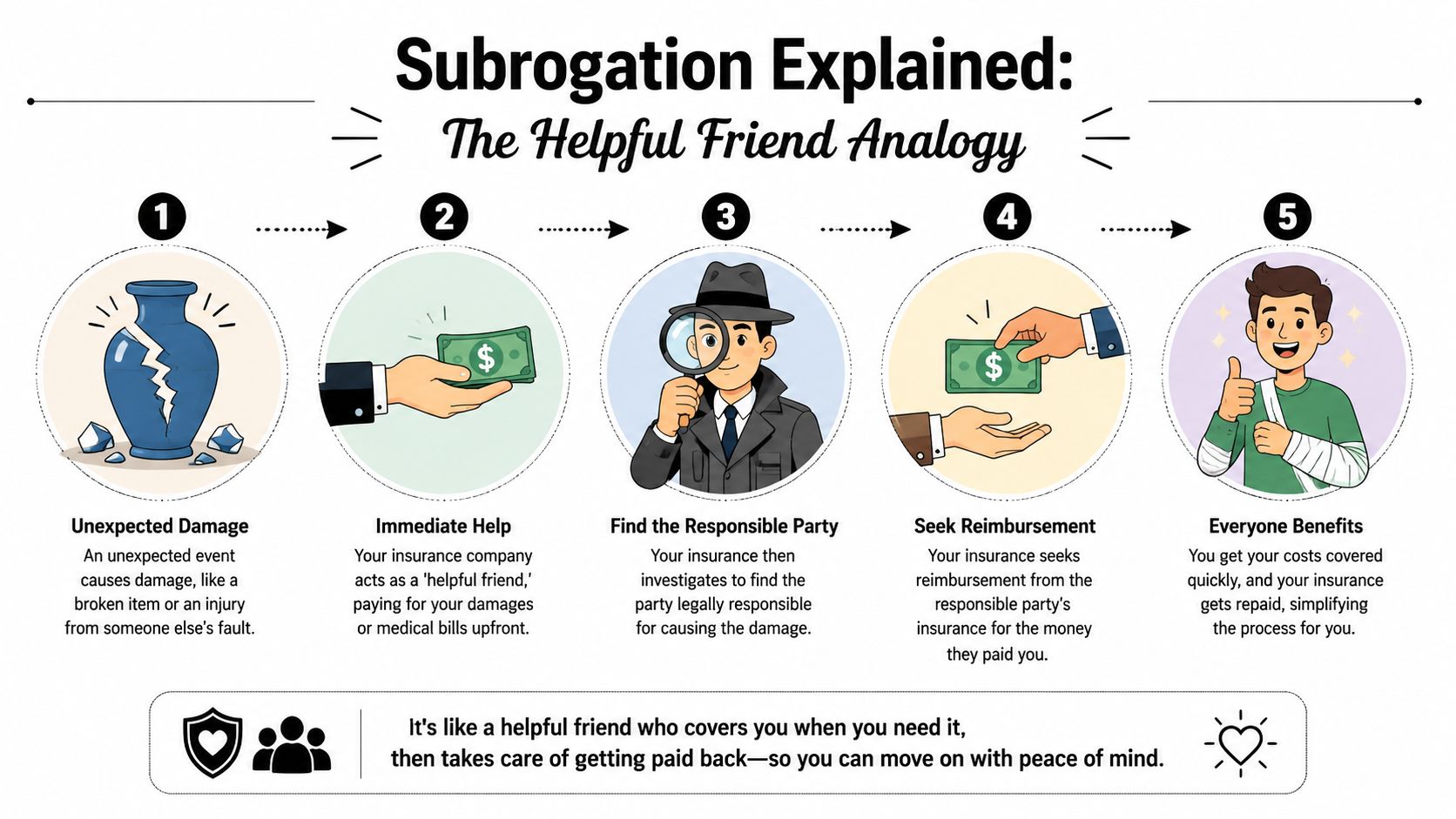

The simplest answer to “what is subrogation claim” is this: your insurer pays first, then tries to collect later from the party that caused the loss.

A good analogy is a friend covering your dinner after someone else steals your wallet. Your friend helps you immediately. Later, your friend goes after the person who caused the problem and asks to be repaid. In insurance, that “friend” is your carrier or health plan. The legal phrase is that the insurer steps into your shoes after payment and pursues the at-fault third party for reimbursement, as explained in this overview of subrogation rights.

The three people or entities in almost every subrogation dispute

To understand subrogation, keep these roles separate:

You, the injured person

You suffered the loss. Your car was damaged, your body was hurt, or both.Your insurer or benefit plan

This company paid something on your behalf. It might be your auto insurer, health insurer, workers' compensation carrier, or another plan.The at-fault third party

This is the driver, business, property owner, or insurer believed to be responsible for the loss.

Once your insurer pays, it may gain the right to pursue the responsible party for the amount it paid. That is the core mechanism.

Why insurers use subrogation

Subrogation is a post-payment recovery mechanism. That means payment comes first, recovery efforts come later. From your perspective, that can be helpful because you don't have to wait for the liability claim to finish before some bills are paid.

But convenience upfront can create pressure later. If your insurer paid money that overlaps with your injury claim, the insurer may try to recover from the same pool of settlement funds you expected to receive.

Plain rule: Subrogation is not about whether you were hurt. It's about who ultimately bears the cost of what was paid.

The sequence in plain language

Here's the usual flow:

- An accident happens. Another person or company may be legally responsible.

- Your insurer pays covered losses. That may include medical bills, repair costs, or related benefits.

- Your insurer investigates fault. It tries to connect its payments to someone else's negligence.

- A reimbursement claim follows. The insurer seeks repayment from the at-fault side.

That's the clean version. Real cases are messier because fault can be disputed, bills may include unrelated treatment, and multiple insurance companies may all claim a right to recover.

Subrogation in Action for Auto and Health Insurance

You get through the first part of an injury claim, and it feels like the bills are finally being handled. Your car is in the shop. Your doctor visits are covered. Then another question shows up: who wants to be paid back later?

For injured people, subrogation usually shows up first in two places: auto insurance and health insurance. The rule sounds simple, but the effect on your money can be very different depending on which policy paid and what it paid for.

Auto insurance subrogation

Auto subrogation often feels less personal at first because it usually starts with property damage and transportation costs. Your insurer may pay for repairs, arrange a rental car, or cover medical payments under MedPay. Later, it may seek repayment from the at-fault driver's insurer for those same amounts, as explained in Progressive's plain-language description of subrogation.

That matters to you for a practical reason. Auto claims are rarely one single bucket of money. They are more like separate envelopes tied to the same crash.

Here are common examples:

- Vehicle repairs: Your carrier pays the body shop, then tries to recover that amount.

- Medical payments coverage: If MedPay covered treatment, your carrier may review whether it can recover those payments.

- Rental car costs: Temporary transportation can be included in the recovery demand.

- Deductible reimbursement: If your insurer recovers money, that can affect whether your deductible is returned.

A rear-end crash shows how this works in real life. Your insurer pays to fix the bumper, covers a few early medical bills, and pays for a rental car for a week. Later, your insurer turns to the at-fault driver's carrier and asks for repayment. If you are also settling your injury case, you need to know which parts have already been paid and which claims may still attach to the final payout.

If you are reviewing the terms of a settlement, it helps to understand how a settlement agreement works before you sign anything.

Health insurance subrogation

Health insurance subrogation tends to hit harder because it involves treatment you needed to recover. Emergency room care, imaging, surgery, follow-up visits, physical therapy, and specialist appointments may all be paid by your health plan first. After that, the plan may ask to be reimbursed from your injury settlement if someone else caused the harm.

This is the part that catches many injured people off guard. You use your health insurance the way you are supposed to use it. Months later, the plan may still claim a right to part of the money meant to compensate you.

The timing also makes it harder to spot. Health treatment can continue for months while the liability claim develops in the background. By the time settlement talks get serious, the reimbursement demand may already be large.

A short explainer can help if this still feels abstract:

Why multiple claims can stack up

One accident can create several repayment demands at the same time. That is where people lose track of what they may ultimately keep.

| Type of payer | What it may want back |

|---|---|

| Auto insurer | Repair costs, MedPay, rental expenses |

| Health insurer | Accident-related medical treatment costs |

| Workers' compensation carrier | Benefits paid if the injury happened on the job |

A helpful way to view this is to picture your settlement as one table with several hands reaching toward it. One hand may belong to your health plan. Another may belong to your auto carrier. If the injury happened at work, a workers' compensation carrier may also be involved.

That overlap is why a case can look settled on paper but still leave serious questions about your net recovery.

How Subrogation Directly Affects Your Settlement

You settle your injury case and feel a wave of relief. Then the question hits. How much of that money will make it into your hands?

That question matters because a settlement amount and a take-home amount are not the same thing. Your settlement may need to cover future medical care, lost income, rent, transportation, and the ordinary bills that kept coming while you were hurt. A subrogation claim can reduce what is left for all of that.

Why your net recovery can shrink

Subrogation affects your settlement at the payout stage. Before money is disbursed, an insurer or health plan may claim a right to be repaid for accident-related benefits it covered.

A lien works like a hold on part of the settlement funds. The money is there, but you may not be free to keep all of it until that claim is reviewed.

The process usually looks like this:

- Your injury claim settles

- Repayment claims are identified and gathered

- The claimed amounts are checked for accuracy and legal support

- Any valid claims are negotiated or paid

- You receive the remaining balance

That final number is your real recovery. It is the amount that affects your daily life, not the larger settlement figure in the headline.

A case can look strong on paper and still leave you disappointed if no one dealt carefully with the repayment demands attached to it.

Why the number on the settlement check can be misleading

Many injured people focus on case value and do not learn until late in the process that settlement math has several layers. The gross settlement is only the starting point. After that come attorney fees, case costs, and any valid subrogation or lien claims.

That is why it helps to understand what a settlement agreement does. The documents that close your case can affect how and when reimbursement issues are resolved.

A clear review separates three different questions:

| Question | Why it matters |

|---|---|

| What was the full value of your injury claim? | This measures the harm caused by the accident |

| What repayment claims are being asserted? | These can reduce what you receive |

| Are those claims legally valid and correctly calculated? | Some claims are too high, unsupported, or limited by law |

A simple example shows the risk

Say you settle for an amount that sounds fair after months of treatment and missed work. Then a health plan claims reimbursement for accident-related care, and your auto insurer also seeks repayment for certain benefits it paid early on. If those demands are accepted without review, your share can drop much more than you expected.

That is why subrogation is not a side issue. It is part of the settlement itself.

The practical problem is simple. You are trying to rebuild your life with a limited pool of money. Every dollar paid back on a valid claim is one less dollar available for your recovery.

Do not assume the demand is correct

A reimbursement notice is not automatically accurate just because it arrived on official letterhead. The claimed amount may include treatment that had nothing to do with the accident. It may count charges instead of actual payments. It may ignore policy language, state law limits, or the fact that your settlement did not fully cover your losses.

Insurers often press these claims before settlement funds are released because that is the moment when money is available and easiest to reach. From your side of the case, that means timing matters. If the claim is not reviewed early, you can lose bargaining room and part of your recovery.

The bottom line is straightforward. Subrogation directly affects your wallet. If you want to know what your settlement is really worth, you have to examine what others say they are entitled to take from it.

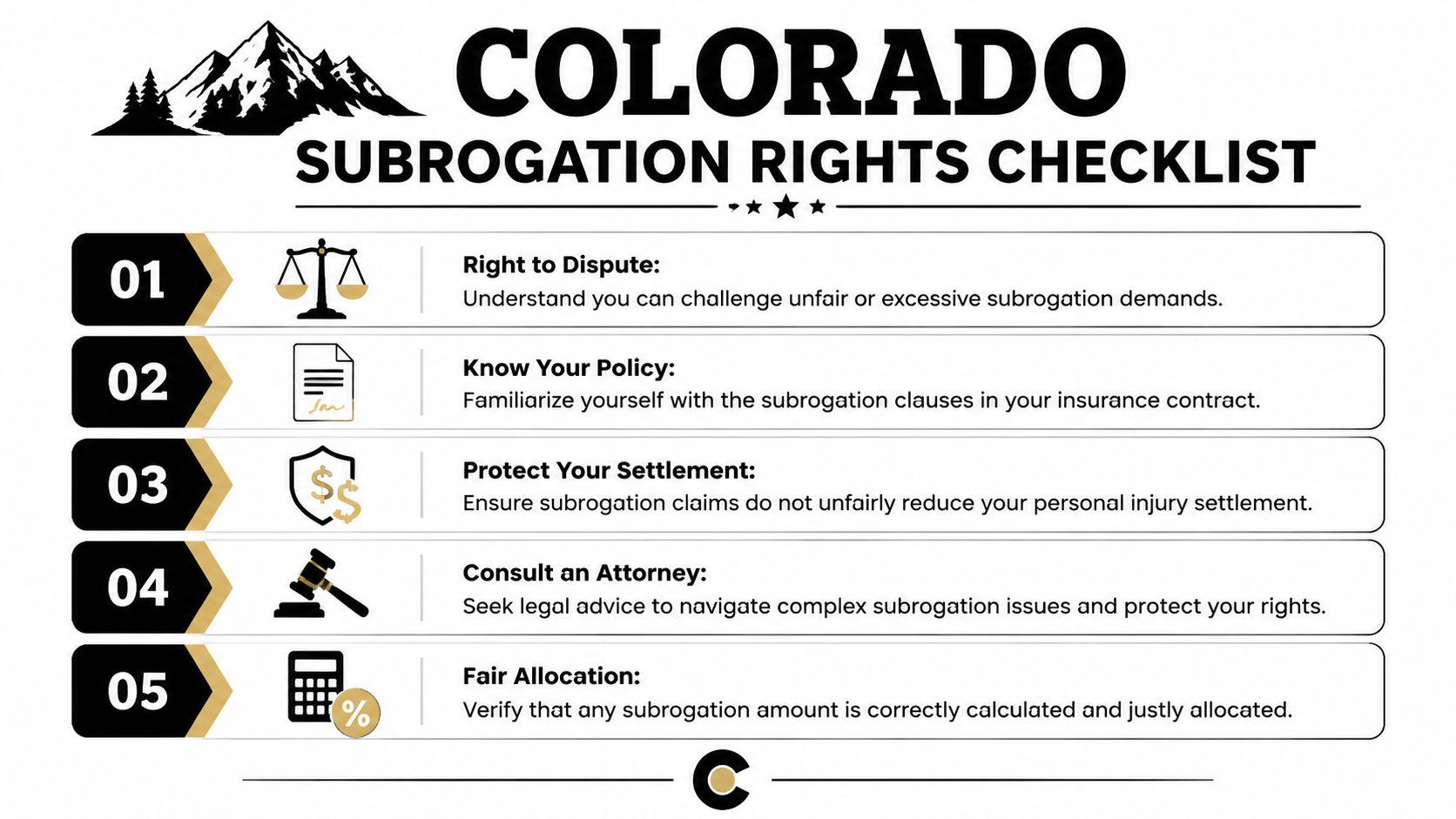

Your Rights Under Colorado Subrogation Laws

Colorado injury victims do have protections, but those protections only help if someone raises them. Insurance companies rarely volunteer the limits of their own recovery rights.

One reason this matters is scale. As noted earlier, an estimated $15 billion in subrogation judgments are obtained annually but remain uncollected. That reality pushes insurers to be assertive before settlement funds are disbursed. In Colorado, that makes state-specific defenses and allocation arguments especially important.

Colorado protections can change the outcome

Two ideas matter a lot in practice.

The first is the Made Whole Doctrine. In plain English, that doctrine can limit an insurer's ability to recover until the injured person has been fully compensated for their losses. If you settled for less than your total damages because of policy limits, disputed liability, or serious long-term harm, that issue may matter.

The second is Colorado's handling of certain MedPay recovery questions. In many injury cases, MedPay creates confusion because people assume any medical payment made by an auto insurer automatically comes back out of the settlement. Colorado law can be more protective than that assumption.

What you should verify in every Colorado case

If a subrogation or lien claim appears in your file, check these issues carefully:

- Whether the payer has a valid legal basis: A demand letter is not proof.

- Whether the bills are accident-related: Charges unrelated to the crash should not be included.

- Whether the amount reflects actual payments: Billed charges and paid amounts are not always the same.

- Whether Colorado defenses apply: State law can affect timing, priority, and fairness.

- Whether another lien is already competing: Workers' compensation and other claims can overlap.

If your injury happened while working, there may be an entirely separate reimbursement issue to untangle. Colorado workers' compensation claims can interact with injury settlements in ways many people don't expect. This overview of a workers compensation lien on personal injury settlement gives a useful snapshot of how those claims can affect the final distribution.

Colorado-specific mindset: Never assume the insurer's first number is the legally correct number.

Rights are only useful if someone enforces them

Colorado law may give you arguments. It doesn't automatically apply them for you.

That means someone has to demand backup, compare the claimed amount to actual records, analyze whether you were made whole, and challenge any overreach. When that work isn't done, people often give up money they didn't owe.

Protecting Your Settlement from a Subrogation Claim

A lot of people assume subrogation claims are automatic and untouchable. They aren't. Some are valid. Some are overstated. Some collapse when you ask for proof and apply the law carefully.

That's why the right response is not panic. It's scrutiny.

Five practical defenses injured people should think about

- Question the medical tie-in: If the insurer included treatment unrelated to the crash, that portion may be challengeable.

- Check what was paid: Some demands are built from charges or summaries that don't match real payment records.

- Review your policy language: Contract wording matters. Not every policy grants the same rights.

- Look for settlement allocation problems: If a case resolves under difficult liability or policy-limit conditions, full repayment may be unfair or unsupported.

- Watch for waiver language: A signed release or contract can accidentally damage recovery rights.

The waiver of subrogation trap

One of the least understood problems is a waiver of subrogation. Policyholder Pulse explains that a waiver of subrogation clause appears in over 40% of commercial contracts and can legally bar an insurer from pursuing a claim. That matters because if an injured person signs away rights without understanding the clause, they can block their own insurer from recovering certain amounts, including a deductible.

This comes up more often than people think in commercial leases, construction settings, fleet situations, and settlement paperwork tied to business relationships. The danger is a double loss. You give up a claim, and your insurer loses its route to recover money that might otherwise have benefited you.

Don't sign any release, reimbursement agreement, or settlement addendum involving insurance rights until someone has reviewed how it affects subrogation.

Why billing records matter more than people think

Subrogation fights often turn on paperwork. Not dramatic courtroom moments. Billing ledgers, payment histories, accident coding, treatment dates, and provider records can make or break a reimbursement demand.

If you're trying to understand how providers and medical receivables get documented on the backend, this overview of the healthcare practice lien process is a useful reference point. It helps explain why careful lien and payment tracking matters when multiple entities claim an interest in the same recovery.

The broader rule is simple. Never assume the claimed amount is clean just because it arrived on formal letterhead.

Why an Attorney Is Your Strongest Defense

Subrogation sits at the intersection of insurance contracts, settlement strategy, medical billing, and state law. That mix is why people lose money when they try to handle it casually.

A good attorney doesn't just argue about fault in the accident case. They audit the repayment claims attached to the case. They compare demand letters to payment records. They challenge unrelated charges, inflated totals, unsupported liens, and waiver language that could damage your recovery. They also negotiate reductions when the law and the facts support it.

That work matters because subrogation problems are often buried in dense documents, plan language, and settlement releases. If a case involves multilingual records, out-of-state paperwork, or translated agreements, precision becomes even more important. Errors in legal wording can change rights in ways people don't notice until the money is gone. This discussion of expert insights on legal translation risks shows why technical accuracy matters so much in legal and claims-related documents.

The bottom line is straightforward. If you're asking what is subrogation claim, you're really asking a more urgent question: Will someone else take part of my settlement, and can I stop that from happening unfairly? In many Colorado injury cases, that answer depends on whether someone with experience is protecting the settlement before the funds are distributed.

If you're dealing with a subrogation letter after a car crash, truck wreck, or serious injury in Colorado, Nares Law Group LLC can help you understand what the insurer is claiming, whether that claim is valid, and how to protect the largest possible share of your settlement for you and your family.