A serious crash changes more than a medical chart. It changes how a family thinks about bills, future care, work, and what happens if the worst occurs. If you or someone you love is recovering from a life-altering injury, or if your family is handling a wrongful death claim, small financial details suddenly feel enormous.

One of those details is the beneficiary form attached to an insurance policy, retirement account, bank account, or settlement-related planning tool. People often assume their will controls everything. In real life, that assumption can leave the wrong person with the asset and the right person with a court fight.

That's why it helps to understand what a beneficiary designation is, how it works, and why updating it can be one of the most protective steps a family takes after a major accident.

What Is a Beneficiary Designation

A family is already under strain after a serious accident. Bills are arriving, treatment decisions are ongoing, and hard conversations about the future can no longer wait. In that moment, a beneficiary designation can determine whether money reaches the right person quickly or gets tied up in confusion.

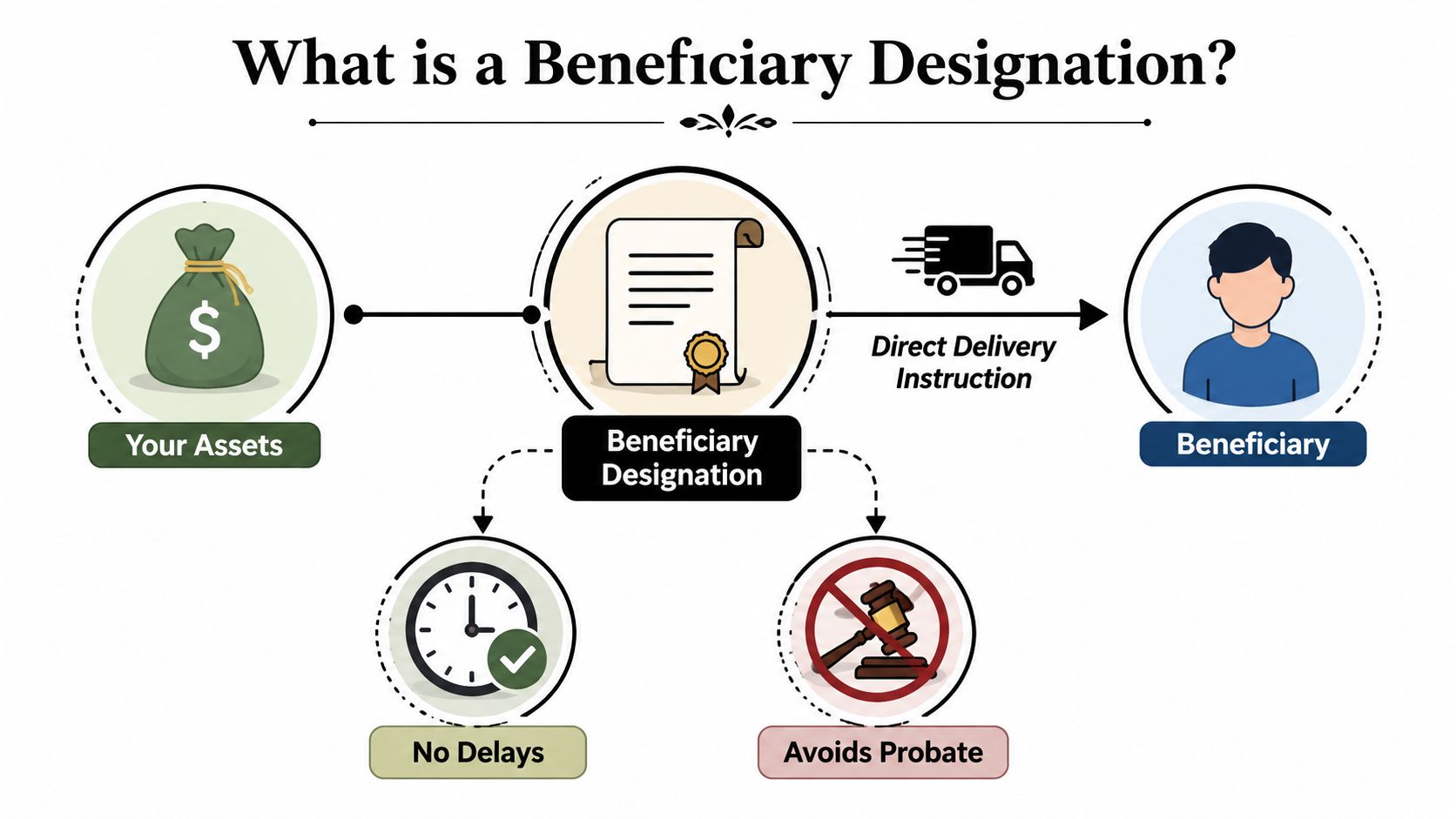

A beneficiary designation is a legal instruction attached to certain accounts and insurance policies. It tells the company holding the asset who should receive it when the owner dies. It works like a delivery label on a specific package. The institution reads the label on that account and sends the asset to the person, trust, charity, or estate named on the form.

That instruction carries legal force. It is not a side note or a casual preference. It is part of the account paperwork, and the bank, insurer, or plan administrator usually relies on that form when the time comes to pay benefits.

This matters for injury victims and their families. After a life-altering crash, people often receive settlement funds, open new financial accounts, update insurance, or revisit job benefits they set up years earlier. If an old form still names an ex-spouse, leaves out a child, or fails to coordinate with a special needs trust, the money may go somewhere the family never intended.

Why this step is easy to overlook

Families often assume a will covers everything. The confusion is understandable. A will feels like the master plan.

But beneficiary designations are attached to individual assets. A will may say one thing while the form on the account says another. In many cases, the institution follows the beneficiary form for that asset.

A short way to remember it is this: the beneficiary form is often the instruction sheet the account company follows first.

That can have real consequences after a catastrophic injury or wrongful death. Money meant to support a spouse, children, or a trust for long-term care can end up delayed or paid to the wrong person if the designation is outdated.

A simple example

Suppose a parent has a workplace life insurance policy and an IRA. Years pass. There is a remarriage, a divorce, a new child, or a growing need to protect settlement money for someone living with a disability. If the beneficiary form never changes, the company holding the account will usually start with the name already on file.

That is one reason families reviewing coverage after a fatal accident should also understand how different policies pay benefits. This guide to accidental death insurance vs. life insurance explains where beneficiary designations often become part of the bigger financial picture.

What the form usually does

Most beneficiary forms ask you to name the person or entity that should receive the asset and to assign shares that add up to the full amount. That may sound administrative. It is not. A few lines on a form can shape who has financial stability after a loss.

If you remember one point from this section, keep this one: a beneficiary designation is one of the clearest ways to protect your family from delay, confusion, and unintended transfers.

The Different Types of Beneficiary Choices

Once people understand the basic idea, the next question is usually, “Who exactly should I list, and how?” Then, the form's language can feel colder than the family decisions behind it.

Institutions commonly ask for the beneficiary's full legal name, relationship, address, and date of birth, and they distinguish between people who are first in line and those who serve as backups. Securian explains this in its guide to naming a life insurance beneficiary.

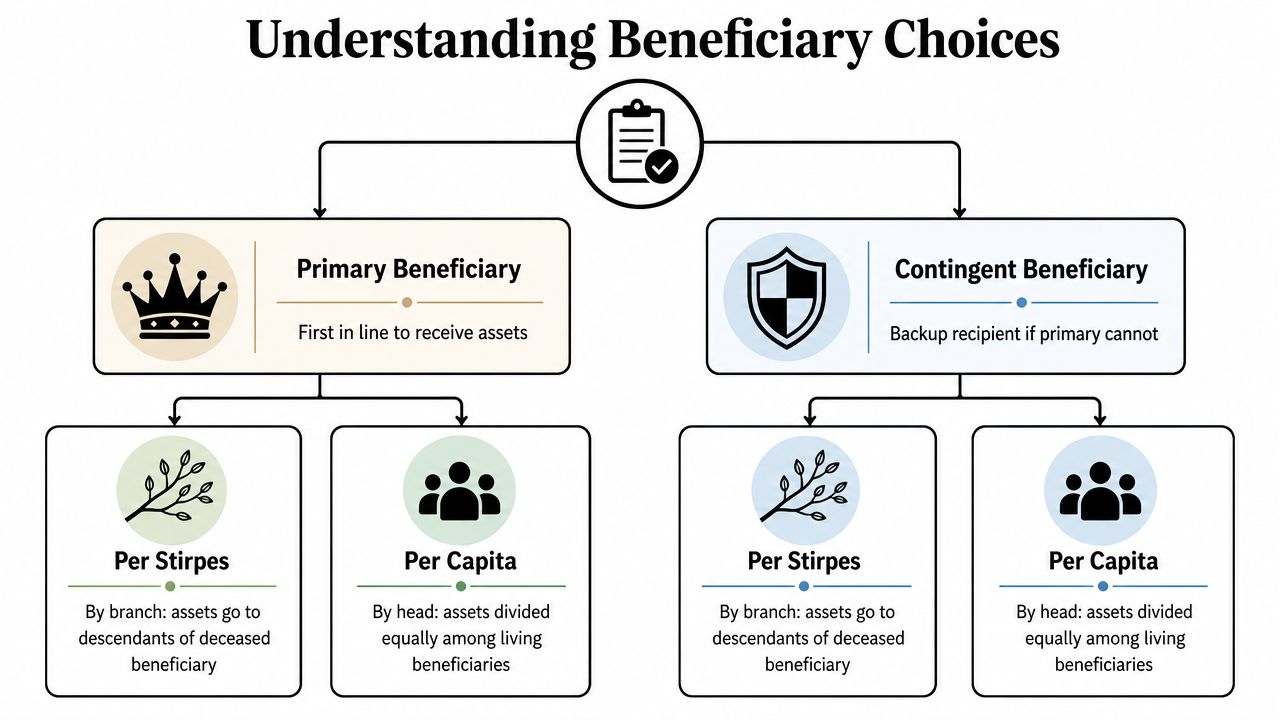

Primary and contingent beneficiaries

A primary beneficiary is first in line to receive the asset.

A contingent beneficiary receives it only if the primary beneficiary is unavailable at the time of death. That could happen if the primary beneficiary died earlier, can't be located, or refuses the inheritance.

Here's the easiest way to understand it:

- Primary means first choice. If the primary beneficiary can receive the asset, the institution usually pays that person.

- Contingent means backup plan. If the first choice can't take it, the institution looks to the contingent beneficiary.

- No backup can create avoidable problems. If the primary beneficiary is gone and no contingent is listed, the asset may be harder to distribute.

Practical rule: Every beneficiary form works better when it includes both a first choice and a backup.

How percentages work

Many forms let you name more than one primary beneficiary. If you do that, you usually assign percentages. Those shares must total 100% for that category.

A common example looks like this:

| Choice | Role | Share |

|---|---|---|

| Spouse | Primary beneficiary | 50% |

| Child A | Primary beneficiary | 25% |

| Child B | Primary beneficiary | 25% |

If all three are primary beneficiaries, the institution follows those percentages on the form.

Per stirpes and per capita

These terms confuse people because they sound technical, but the family impact is simple.

Per stirpes

Per stirpes usually means a deceased beneficiary's share passes down that person's branch of the family tree.

Example: You name your two adult children as beneficiaries. One dies before you, leaving children of their own. Under a per stirpes approach, that deceased child's share would generally pass to that child's descendants.

Per capita

Per capita usually means the asset is divided among the living beneficiaries in the named group.

Using the same family, if one child dies before you, the surviving named beneficiary may receive the whole amount rather than the deceased child's descendants receiving that share.

These options matter in blended families, families with grandchildren, and families trying to protect children after a severe accident or a parent's death.

What about minors or trusts

Naming a minor directly can create practical complications because financial institutions often need an adult or legally recognized arrangement to manage funds. In some families, a trust is the cleaner choice, especially when a child has special needs, the funds should be used gradually, or a settlement needs careful management.

A short checklist helps when you're filling out a form:

- Use legal names. Nicknames and vague descriptions create confusion.

- Include complete identifying details. Institutions ask for them for a reason.

- Think beyond today. Ask what happens if your first choice dies before you.

- Match the choice to the family situation. A trust may fit better than naming a child outright.

The form may look administrative. The decision behind it is personal.

Accounts That Use Beneficiary Designations

A family often finds beneficiary designations in the middle of a hard moment, not during calm planning. After a serious accident, a spouse may be reviewing insurance, retirement savings, and new settlement accounts while also handling medical decisions, missed work, and fear about the future. That is when this question becomes practical: which assets already have instructions telling the institution who gets the money?

Many do.

Beneficiary designations commonly appear on life insurance, retirement accounts, and certain bank or investment accounts. Some states also let people transfer real estate outside probate with a transfer-on-death deed. If your family is dealing with the financial aftermath of an injury or trying to understand what happens after a death claim, rules about probate and direct transfers often overlap with state-specific issues like the Colorado wrongful death statute.

Where families usually find them

A beneficiary form works like a set of delivery instructions attached to a specific asset. The bank, insurer, or plan administrator checks that instruction first when the owner dies.

Start by looking for these accounts:

- Life insurance policies. This includes individual policies and coverage through an employer.

- Workplace retirement plans. Examples include 401(k) plans, 403(b) plans, and some pension survivor benefits.

- IRAs and similar retirement accounts. These often have their own beneficiary forms on file.

- Bank accounts with POD instructions. “POD” means payable on death.

- Brokerage accounts with TOD instructions. “TOD” means transfer on death.

- Annuities. These usually name one or more beneficiaries in the contract paperwork.

- Real estate in states that allow TOD deeds. A recorded deed can direct who receives the property at death.

This catches families off guard because the form may have been signed years earlier, during hiring paperwork, open enrollment, or a quick account opening meeting.

Why this matters after a personal injury settlement

A settlement can change a family's financial structure almost overnight. Money may go into a new investment account. A parent may buy more life insurance. A family may create a trust because a child needs long-term care, government benefits protection, or help managing funds after a disabling injury.

If the old forms stay in place while new planning happens somewhere else, the result can be a patchwork. One account follows updated wishes. Another follows a form signed long before the accident.

That is one reason families ask probate questions at the same time. For added context on how transfer-on-death planning fits into the broader estate process, see how BDJ Express Law helps with probate.

A simple account audit

Gather the documents you already have. Check the employee benefits portal, retirement statements, insurance records, bank paperwork, and brokerage account profiles.

Then ask one question for each asset: Does this asset pass by beneficiary designation, joint ownership, trust terms, or probate?

That single review often reveals instructions the family forgot existed, or never knew were there at all.

The Critical Rule Beneficiary Designations Override Wills

This is the rule families need to know before a crisis turns into a dispute.

Because the asset is contractually directed to the named beneficiary, it typically bypasses probate court. The designation on file generally controls that asset's disposition even if a will says otherwise, and mismatches can create unintended transfers and litigation risk, as explained in this article on what beneficiary designation means in probate and estate disputes.

Core rule: For assets with a valid beneficiary designation, the form on file usually controls before the will does.

Why the law treats it this way

A will is a testamentary document. A beneficiary designation is part of the contract governing a specific account or policy. The institution holding that asset looks to its contract records first.

That difference sounds abstract until a family lives through it.

Suppose a person divorces, updates the will, and leaves everything to their children. But they never update the old retirement plan beneficiary form. When that person dies, the retirement account may still go to the ex-spouse named on the plan documents. The family may feel certain that the will should win. Often, it doesn't for that asset.

Why this hits injury and wrongful death cases so hard

When a family is focused on surgeries, rehabilitation, permanent disability, or grief, paperwork drops to the bottom of the list. But these forms can control who receives life insurance proceeds, retirement funds, or accounts that become central to supporting surviving family members.

If your family is already navigating loss after negligence, understanding the legal framework for these claims can also help. This overview of the Colorado wrongful death statute explains part of the bigger legal environment families may be facing.

A second layer of confusion comes after death, when the family tries to settle accounts, collect records, and understand what belongs to the estate versus what passes outside it. For a plain-language overview of that process, this practical guide to estate settlement is a helpful companion resource.

Before you move on, this short video may help reinforce how beneficiary instructions and estate documents can collide in real life.

The safest takeaway

Don't assume your will “covers” accounts with named beneficiaries. It may not.

If you've had a major life event, compare the actual beneficiary forms against your current wishes. Read the names on file. Read the percentages. Read the backup choices. Those details decide far more than many anticipate.

Common Beneficiary Mistakes and How to Prevent Them

Most beneficiary mistakes aren't dramatic when they happen. They often unfold without much notice. A form gets signed once and never revisited. An address changes. A child is born. A divorce decree is entered. An old employer plan sits untouched for years.

Then a death occurs, and the family discovers the form tells a different story.

Bank and wealth-planning guidance warns that outdated records, missing beneficiaries, or extra identity verification can still delay payment. Administrative review, conflicting records, and outdated forms can slow distribution even when probate is avoided, according to U.S. Bank's discussion of common beneficiary designation mistakes to avoid.

The mistakes families make most often

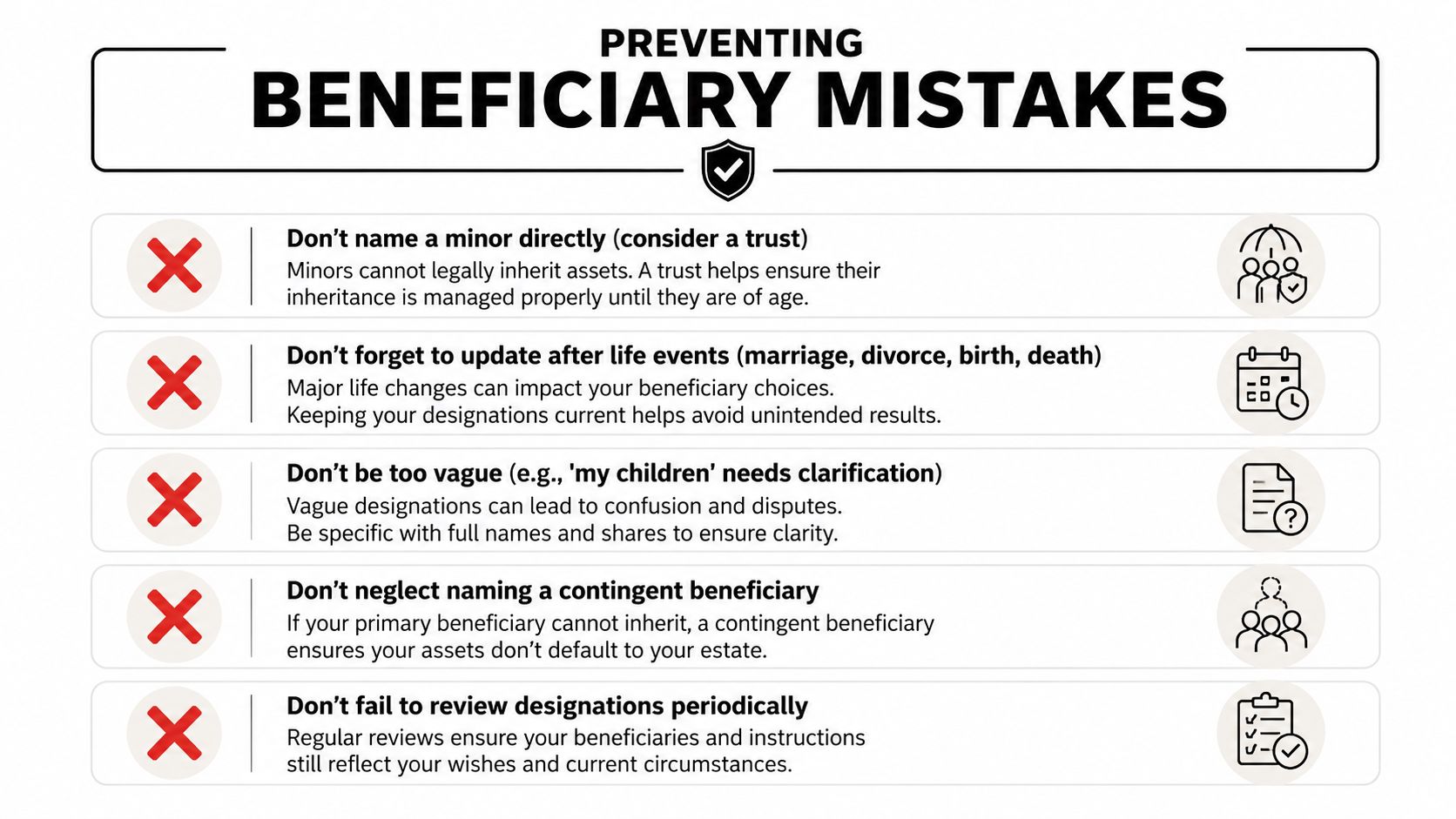

Forgetting to update after life changes

This is the big one. Marriage, divorce, remarriage, birth, death, estrangement, disability, and a new settlement plan can all change who should receive an asset.

A form that once made perfect sense can become dangerous through inaction alone.

Leaving out a contingent beneficiary

A parent names a spouse as sole beneficiary and stops there. Years later, both die close in time, or the spouse dies first. Without a backup, the institution may need more process, more documentation, and more delay.

Naming a minor directly

Parents often do this out of love. The issue isn't the intention. The issue is administration. If a child is young, the institution may not be able to hand over the asset as straightforwardly as the parent expected.

Using vague descriptions

“My children” may sound clear inside a family. It may be less clear on paper in a blended family, after adoption, after estrangement, or where a child has died leaving descendants.

Clear names beat shorthand every time.

The mistake people don't expect

Even a basically correct designation can still lead to hold-ups if the institution needs to confirm identity, reconcile inconsistent records, or locate beneficiaries. Families hear “avoids probate” and assume “immediate payment.” Those are not the same thing.

That's why it helps to think about probate avoidance as one part of a larger plan, not a magic shortcut. If you want a broader overview, this article on how to protect your assets from probate offers useful background on non-probate transfers and related planning tools.

A prevention checklist that works

Use this review list once a year and after any major family change:

- Pull every account statement. Don't rely on memory.

- Confirm the exact beneficiary names on file. Old employer plans are easy to overlook.

- Check contact details. Wrong addresses and outdated personal information can create problems.

- Make sure backup beneficiaries exist. One name is often not enough.

- Ask whether a trust should be listed instead of an individual. This matters in families with minors or special care concerns.

- Store confirmation copies. Keep the submitted form and any acknowledgment from the institution.

For families carrying the stress of injury care, these steps may feel administrative. They are. But they're also protective.

Next Steps for You and Your Family

When a family is dealing with a spinal injury, traumatic brain injury, permanent disability, or the death of a loved one, estate planning terms can feel far removed from immediate survival. But beneficiary designations sit right at the intersection of grief, money, and long-term security.

If you've been asking what is beneficiary designation, the practical answer is this: it's one of the few places where a short form can determine whether money reaches the intended person directly, or whether confusion follows. That matters even more when a family is reorganizing life after a settlement, setting up support for children, or trying to protect a surviving spouse from unnecessary obstacles.

A calm way to move forward

Start with a folder, not a grand plan. Gather insurance policies, retirement account statements, bank and brokerage records, and any trust documents. Then compare each account's beneficiary instruction to your current wishes.

If you or your loved one recently received settlement funds, pause before assuming everything should flow through a will. Some assets may need updated designations. Some may be better coordinated with a trust. Some may need professional review because the family situation is more complex than a simple named beneficiary can solve.

When to ask for help

You don't need to handle every legal and financial issue at once. But you should get advice if any of these are true:

- A child or dependent adult needs protection

- A trust already exists or should be considered

- There was a divorce, remarriage, or blended family situation

- A beneficiary has died or can't be located

- A major settlement changed the family's financial structure

For families coping with a fatal injury claim, it can also help to understand the broader legal process around accountability and compensation. This guide to wrongful death claims in Colorado provides context many surviving relatives need while organizing the financial side of loss.

The most caring version of estate planning is often simple maintenance. Read the forms. Update the names. Keep copies where your family can find them.

You can't undo the accident that brought your family here. But you can reduce uncertainty. Reviewing beneficiary designations is one of the clearest, most immediate ways to do that.

If your family is dealing with a catastrophic injury or wrongful death and you need clear guidance during an overwhelming time, Nares Law Group LLC offers compassionate support for injured people and surviving families. A strong legal team can help you pursue accountability while you focus on recovery, care, and protecting your family's future.