A crash scrambles your attention. One moment you're driving to work, picking up your kids, or heading home on I-25. The next, you're looking at a damaged car, a pounding heart, and a phone full of missed calls while an insurance adjuster starts asking questions you're not ready to answer.

That confusion is normal. Individuals often don't learn Colorado car accident laws until they need them, and by then they're already dealing with pain, repair bills, and lost time from work. The hard part is that Colorado's rules don't operate one at a time. Fault rules affect insurance. Insurance limits affect whether your losses will be paid. Reporting deadlines affect both your license and your claim.

Navigating the Aftermath of a Colorado Crash

A lot of clients describe the same first day. They're sore but unsure whether it's serious. The other driver says, “Let's keep insurance out of it.” A police officer may or may not come to the scene. Then, by evening, the injured person starts wondering whether they made a mistake by going home, delaying care, or failing to take enough photos.

That's why understanding colorado car accident laws matters in practical terms, not just legal terms. Colorado sees a large number of crashes, and the stakes are real. According to a Colorado Department of Transportation summary, fatalities rose from 691 in 2021 to 764 in 2022, an 11% increase. The same source also references more recent reporting showing 97,398 total crashes and 698 fatalities in 2025. Those aren't abstract figures. They represent thousands of people dealing with medical care, insurance disputes, missed work, and grief.

If you're reading this while injured or caring for someone who is, start with two goals. Protect your health. Protect the record of what happened. Those two tracks usually move together. Medical records help your recovery, and they also document that the crash caused harm.

Why people get tripped up

Colorado's system can feel unfair at first because being hurt doesn't automatically mean you'll be paid. You still have to show who was at fault, what losses you suffered, and where compensation will come from. A seemingly simple wreck can turn complicated if the other driver denies fault, carries low coverage, or leaves the scene.

Practical rule: The first version of events often becomes the foundation of the whole claim. What gets documented early tends to matter later.

Physical recovery can also be slower than expected. If you're dealing with stiffness, headaches, or back pain, this resource on healing faster after a motor vehicle accident explains why symptoms can build over time and why consistent treatment matters.

What helps most right now

Three habits protect people after a crash:

- Write down what you remember: Even a short note on your phone about the lane positions, traffic light, weather, and what the other driver said can help later.

- Keep everything in one place: Save photos, discharge papers, prescriptions, repair estimates, and insurer emails in a single folder.

- Don't assume the system will sort itself out: Colorado law gives you rights, but you still have to preserve them.

Your First Steps What to Do Immediately After an Accident

The first hour after a crash matters. Not because you need to become a lawyer at the roadside, but because simple actions can protect your safety and your claim.

Start with safety

If your vehicle can be moved safely, get out of active traffic. Turn on hazard lights. Check yourself first, then passengers, then others involved. Adrenaline can hide pain, so don't assume everyone is fine just because they're standing.

If anyone may be hurt, call 911. Even if injuries seem minor, you want medical help available and a dispatch record showing the crash happened when and where you say it did.

Stay and report what happened

Colorado drivers generally must stop at or near the scene after a crash. A Colorado legal summary also notes reporting duties when there's injury, fatality, or property damage over $1,000, and explains that evidence should be preserved early because delay creates problems with memory, vehicle inspection, and reconstruction in this overview of Colorado car accident laws.

That means “I was in a hurry” or “the cars still drove away” usually isn't a safe assumption. If the crash qualifies, report it.

Gather the right evidence

You don't need perfect evidence. You need enough to make the truth harder to dispute.

Take photos of:

- Vehicle positions: Before cars are moved, if it's safe to do so

- Damage points: Close-up and wide shots of every vehicle

- The roadway: Lane markings, skid marks, debris, traffic signs, and signals

- Conditions: Snow, rain, glare, construction, or blocked views

- Visible injuries: Bruising, cuts, airbags, and broken glass

Collect these details too:

- Driver information: Name, phone number, address, plate number, insurer, and policy details

- Witness contacts: Neutral witnesses often matter when drivers disagree

- Officer information: Agency name, report number, and how to request the report

If you can't think clearly, use your phone camera like a second memory. Walk slowly around the scene and record everything.

Get medical care even if you hope you're okay

A lot of people skip care because they don't want to overreact. Then neck pain, dizziness, numbness, or headaches appear later. Delayed symptoms are common after car wrecks. If you're evaluated early, your records show a cleaner timeline between the crash and the injury.

Say less at the scene

Be polite. Be cooperative. But don't guess.

A few phrases help:

- To police: “I'll give the facts I know.”

- To the other driver: “Let's exchange information.”

- To insurers: “I'm still being evaluated.”

Avoid apologizing or speculating. People often say “I'm sorry” out of shock, not fault. Insurance companies may still try to use it.

Understanding Fault in Colorado Crashes

Colorado follows an at-fault system. That means the legally responsible driver, or another negligent party, pays compensatory damages after a crash. The key issue isn't whose insurance card is bigger. The key issue is who caused the collision and how strongly the evidence proves it.

If you've wondered whether Colorado is a no-fault state, the short answer is no. This explanation of whether Colorado is a no-fault state gives helpful background on that distinction.

Think of fault like a pie

Colorado uses modified comparative negligence. Under this rule, a claimant can recover damages only if they are less than 50% at fault, and any recovery is reduced by their share of fault, as explained in this summary of Colorado car accident liability laws.

Here's the simplest way to picture it. Imagine a pie that represents all blame for the crash.

- If the other driver gets most of the pie and you get a smaller slice, you may still recover.

- If your slice grows, your compensation shrinks.

- If your slice reaches 50%, recovery is barred.

A plain example

Say a driver runs a red light, but you were also speeding. The insurer may argue both actions contributed. If you're found to share some fault, your claim doesn't automatically disappear. But the amount you receive can be reduced.

That's why fault fights matter so much. Small details can move the pie. A witness who saw the light change, a photo showing point of impact, or vehicle data showing speed can all affect where blame lands.

Why this matters: The difference between being seen as mostly careful and equally to blame can determine whether you recover anything at all.

Where people get confused

Many injured drivers think, “I wasn't perfect, so I probably don't have a case.” That's not how Colorado law works. You can make a mistake and still have a valid claim if the other party bears the larger share of fault.

Insurers know this. Adjusters often look for statements they can use to increase your percentage of blame. Common examples include:

- Casual admissions: “I never even saw him.”

- Unnecessary guesses: “Maybe I was going a little fast.”

- Minimizing the other driver's conduct: “It just happened so fast.”

Fault can involve more than two drivers

Some crashes involve a chain reaction, a company vehicle, a rideshare trip, a poorly secured load, or a dangerous road condition. In those cases, fault may be spread among several parties. The legal question becomes less about one villain and more about how responsibility is divided.

That's one reason evidence matters more than intuition. What feels obvious right after a crash isn't always what the paper trail shows later.

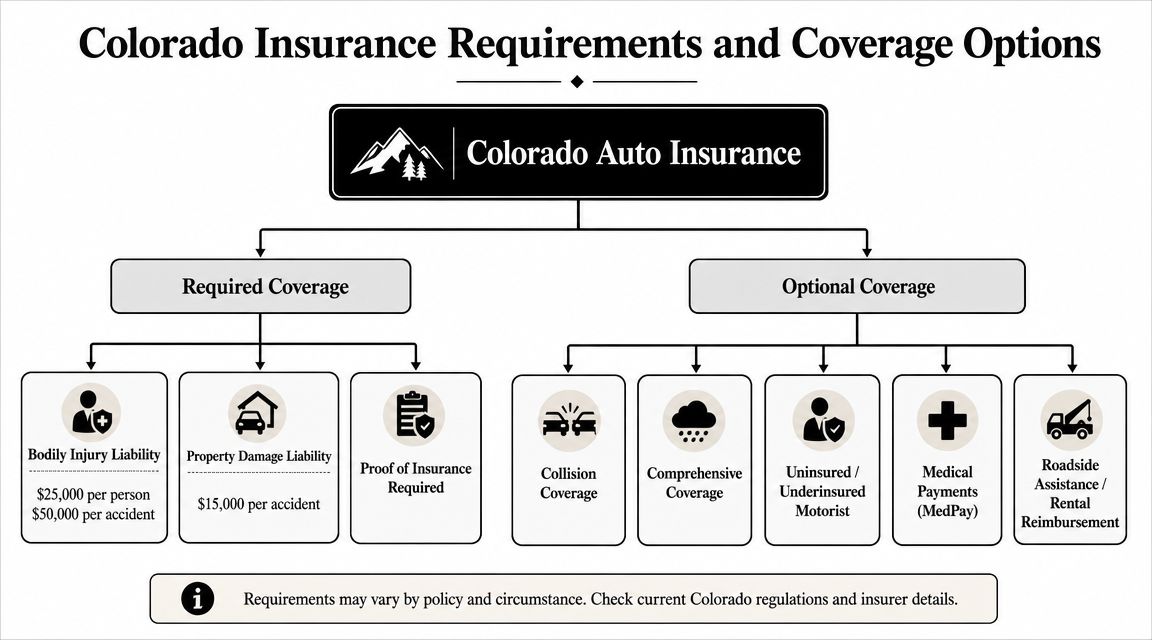

Colorado Insurance Requirements and Coverage Options

After fault comes the next hard question. Where does the money come from? In many cases, the answer is not “enough.”

Colorado's minimum liability limits are $25,000 per person and $50,000 per accident for bodily injury, and those limits can be exhausted quickly in serious crashes, which is why Colorado liability insurance requirements and policy review matter so much. When injuries are significant or multiple people are hurt, those numbers may not stretch very far.

Liability coverage

Liability insurance is the coverage that pays when an insured driver causes harm to someone else. In a fault-based state like Colorado, this is usually the first pool of money examined after a crash.

But minimum coverage is just that. Minimum. A short ambulance ride, imaging, follow-up care, and time off work can put pressure on a small policy quickly. If multiple injured people are making claims under one policy, the available funds may have to be divided.

UM and UIM coverage

Uninsured/Underinsured Motorist coverage, often shortened to UM/UIM, becomes important. According to this overview of Colorado car accident coverage issues, Colorado's low minimum limits are often not enough in serious accidents, making UM/UIM critical.

UM/UIM acts like a backup source of protection under your own policy in certain situations, including when:

- The other driver has no insurance

- The other driver has insurance, but not enough

- A hit-and-run driver isn't identified

People often assume their own insurer will automatically be on their side in a UM/UIM claim. Sometimes the process is smoother than expected. Sometimes it becomes its own dispute about fault, medical necessity, or value.

Other useful coverage to check

Pull out your declarations page and look for these items:

- Medical Payments coverage: Often called MedPay. It may help with medical bills regardless of fault, depending on your policy terms.

- Collision coverage: Helps pay for repairs to your own vehicle, subject to the policy.

- Rental reimbursement: Can help while your car is in the shop.

How the pieces work together

Think of insurance like layers of rain gear in a storm. The at-fault driver's liability coverage is the outer layer. If that layer is thin or torn, your own UM/UIM, MedPay, or collision coverage may become the practical protection that keeps the financial damage from spreading.

For people dealing with severe injuries or a disputed claim, some choose to get legal help early. A firm such as Nares Law Group LLC handles investigation, insurance negotiations, and case development in Colorado crash matters. The point isn't to escalate every claim. It's to avoid missing coverage or undervaluing losses when the facts are serious.

What Compensation Can You Recover After a Crash

Many people think a claim is just about hospital bills and car repairs. In reality, the law looks at the broader effect the collision had on your life. A strong claim accounts for both the bills you can count and the losses that are harder to measure but still very real.

Economic damages

These are the financial losses with paper trails. They're often easier to identify because they show up in invoices, payroll records, pharmacy receipts, or repair estimates.

Common examples include:

- Medical expenses: Emergency care, follow-up visits, imaging, medication, physical therapy, and future treatment tied to the crash

- Lost wages: Income you missed while recovering or attending treatment

- Reduced earning ability: When injuries affect the kind of work you can do going forward

- Property damage: Vehicle repair or replacement and related out-of-pocket costs

If your doctor recommends ongoing care, don't assume only the first round of bills matters. A claim should reflect the full course of treatment supported by the evidence.

Non-economic damages

These losses don't come with a simple receipt, but they still matter. The law recognizes that an injury can change how your body feels, how your mind handles stress, and how your daily life functions.

Examples include:

- Pain and suffering

- Emotional distress

- Loss of enjoyment of life

- Physical impairment or limitations

A useful way to think about non-economic damages is this: if a crash changes how you sleep, drive, work, parent, exercise, or participate in normal routines, those effects belong in the case.

Keep a short recovery journal. Notes about pain levels, missed events, sleep problems, and daily limitations can help show what your injury actually cost you beyond the bill stack.

Don't value the case too early

People often want a quick number right away. That urge is understandable, especially when bills start arriving. But valuing a claim too soon can be risky if you haven't finished medical evaluation or don't yet understand the long-term impact.

A fair case assessment usually depends on several moving parts:

| Claim factor | Why it matters |

|---|---|

| Medical records | They connect the crash to your symptoms and treatment |

| Work impact | They show lost income and disruption to your routine |

| Fault evidence | It affects whether compensation is reduced |

| Available coverage | It may limit what can realistically be collected |

A settlement should reflect the full picture, not just the first week after the wreck.

Special Rules for DUI and Hit-and-Run Accidents

Not every crash is treated the same way. When the at-fault driver was impaired or fled the scene, the case often becomes more serious both factually and legally.

A recent Colorado crash summary reported 52,532 crashes involved DUI charges and 64,686 were suspected to involve alcohol, underscoring why impairment is a major issue in claims and why these cases can involve punitive damages, as discussed in this review of Colorado motor vehicle accident statistics.

When alcohol or drugs are involved

An impairment case changes the tone of the claim. Evidence about intoxication can strengthen the argument that the other driver acted recklessly, not merely carelessly. That can affect settlement negotiations and litigation strategy.

In practical terms, these cases often require fast evidence preservation. Blood or breath evidence, criminal charges, bodycam footage, bar receipts, and witness observations may all become relevant. The civil case and the criminal case are different, but information from one can affect the other.

If your family is also trying to understand what happens on the criminal side after an arrest, this guide to the Colorado DUI bail process gives a basic overview of that separate process.

Hit-and-run claims

A hit-and-run creates a different problem. Fault may be obvious, but the driver is gone. That means the claim often turns on what you can prove and what coverage exists under your own policy.

Focus on these steps quickly:

- Call police immediately: A prompt report supports that the crash occurred and may help locate the driver.

- Look for witnesses and cameras: Nearby businesses, homes, and dashcams can matter.

- Document vehicle debris: Parts left behind can help identify the fleeing vehicle.

- Review your UM/UIM coverage: This may become the central path to recovery.

In a hit-and-run, your own policy may become the main source of compensation. Don't assume that means the claim will be simple.

These cases reward speed. Surveillance footage disappears, witness memories fade, and vehicle fragments can get lost.

Critical Deadlines The Colorado Statute of Limitations

After a crash, people usually focus on healing and car repairs first. The legal clock still runs in the background. Missing a deadline can damage a claim even when liability is strong.

Colorado motor vehicle crash cases generally must be filed within three years when they involve bodily injury or property damage arising from the use or operation of a motor vehicle. Separately, a written crash report called DR 3447 may be required within 60 days for crashes involving injury, death, or significant property damage, as explained in this guide to Colorado filing deadlines after a car accident.

Two clocks, different purposes

People often confuse these deadlines because both relate to the same wreck, but they do different jobs.

The three-year deadline is the lawsuit filing window. If you miss it, a court may refuse to hear the case.

The 60-day report is an administrative requirement tied to qualifying crashes. Calling police at the scene and filing the written report are not always the same thing.

Key Colorado Car Accident Deadlines

| Action Required | Deadline | Governing Law/Rule |

|---|---|---|

| File a lawsuit for bodily injury or property damage from a motor vehicle crash | Generally within three years | Colorado statute for tort actions arising from motor vehicle use |

| Submit written crash report DR 3447 when required | Within 60 days | Colorado administrative crash reporting requirement for qualifying crashes |

Why waiting causes problems

Even when you're still within the filing period, delay can hurt the proof. Cars get repaired. Photos get deleted. Witnesses move. Medical providers change systems. Reconstruction becomes harder.

A short checklist helps:

- Request the crash report early

- Preserve vehicle photos before repairs

- Keep treatment records together

- Track all insurer communications in writing

If you're unsure whether the written reporting rule applies in your situation, find out early. It's much easier to correct course in week one than month six.

Frequently Asked Questions About Colorado Accident Claims

Should you talk to the other driver's insurance company

You can usually provide basic identifying information. Be careful about giving a recorded statement before you understand your injuries and the facts. Early conversations often sound informal, but they can shape how the insurer argues fault and damages later.

If you do speak with an adjuster, keep it simple. Confirm the date, location, vehicles involved, and that treatment is ongoing. Don't guess about speed, distance, or how you'll feel next week.

What if you were partly at fault

Partial fault does not automatically end a claim in Colorado. What matters is whether your share of blame stays below the bar discussed earlier. In real life, this means evidence becomes even more important because fault allocation drives value.

Useful proof can include:

- Scene photographs

- Witness statements

- Medical records

- Vehicle damage patterns

- Traffic camera or dashcam footage

What if the at-fault driver had little or no insurance

This is one of the most frustrating situations for injured people. You may have a strong case on liability and still run into a collection problem. That's when your own UM/UIM coverage can become central.

Also check whether there may be another responsible party. In some crashes, liability extends beyond the individual driver, depending on the facts.

How much is a lawyer paid in a car accident case

Most personal injury lawyers handling crash claims work on a contingency fee. That usually means the fee comes from the recovery rather than an upfront hourly charge. The exact percentage and expense terms depend on the fee agreement, so read that agreement carefully and ask questions until it's clear.

Do you need a lawyer for every crash

No. Some property-damage-only cases are manageable without one. But legal help becomes more useful when injuries are significant, fault is disputed, multiple vehicles are involved, the insurer is delaying, or available coverage may be limited.

What should you bring to a consultation

Bring whatever you have. You do not need a perfect file.

A helpful starter set includes:

- Crash report or report number

- Photos and video from the scene

- Insurance information for all drivers

- Medical records and bills you've received

- Repair estimates or total-loss documents

- Any letters, emails, or texts from insurers

The best time to get clarity is before you give detailed statements, sign releases, or accept money that closes the claim.

Should you post about the crash on social media

That's usually a bad idea. Even harmless-looking posts can be misunderstood. A smiling photo at a family event doesn't prove you aren't in pain, but an insurer may still try to use it that way.

What if you already accepted part of the insurance payment

It depends on what you signed. Payment for vehicle damage is often separate from a bodily injury release, but you should verify that before assuming your injury claim remains open.

If you're dealing with injuries, insurance pressure, or questions about fault after a crash, Nares Law Group LLC offers Colorado accident guidance and case evaluation for people who need help understanding their rights and next steps.