You paid your premiums. You reported the crash. You sent the medical records, repair estimates, photos, and every form the insurance company asked for. Then the waiting started.

A week turned into more. Calls went unanswered. The adjuster changed. The explanation shifted. Maybe the insurer denied the claim outright. Maybe it offered a number that didn't come close to covering what happened to you. Or maybe it finally paid something, after dragging you through months of stress, and left you wondering whether that unfair process was just “how insurance works.”

It isn't.

Colorado law gives injured people real protection when an insurer mishandles a claim. That matters most after a car wreck or truck collision, when bills are stacking up and your energy is already going toward healing. The hard part is that insurance bad faith can feel vague until you know what to look for.

This guide is built for that moment. It explains Colorado insurance bad faith in plain language, including two points many people miss: an insurer can face bad faith liability even if it eventually pays, and you generally sue the insurance company, not the individual adjuster.

When Your Insurance Company Breaks Its Promise

Insurance is a promise on paper. You keep your side by paying premiums and reporting claims accurately. The company keeps its side by investigating fairly and paying covered claims without games.

When that promise breaks, people usually feel two things at once. First, anger. Second, self-doubt. Many injured people start asking whether they're overreacting, whether the delay is normal, or whether they should just accept less and move on.

A common example looks like this. A driver gets hit by a commercial truck on I-25. Her injuries keep her out of work. She opens a claim, cooperates fully, and expects the insurer to evaluate it on the facts. Instead, the company asks for the same records more than once, ignores the treating doctor's explanation, and focuses on scraps of information that make the injury sound less serious. Months later, the insurer sends a partial payment and acts as if that should end the matter.

It often doesn't.

Bad faith isn't just about a final “no.” It can be about the road the insurer forced you to travel to get to any answer at all.

That distinction matters in Colorado. A claim can become a bad faith problem because of how the insurer handled it, not only because of the final result. If the company used delay, selective investigation, unfair pressure, or unreasonable denial tactics, the law may give you a remedy.

People also get tripped up by blame. They focus all their frustration on the adjuster whose name appears on the emails. That reaction is understandable. But legal responsibility usually points you toward the insurer itself.

If you're in the middle of a claim and nothing feels straightforward anymore, trust that instinct enough to look closer. Confusion is often part of the pressure. Clarity is how you take some control back.

What Is Insurance Bad Faith in Colorado

An insurance policy is a promise on paper. Colorado law treats that promise as more than a stack of forms and premiums. It includes an implied duty of good faith and fair dealing, which means the insurer must investigate, evaluate, and respond to your claim in a fair and reasonable way.

The point that many injured people miss is this: bad faith can exist because of the insurer's process, not only because of the final answer. A company does not erase months of unfair delay, selective review, or pressure tactics by sending a check later. If the claim was handled unreasonably, the problem may still be bad faith even when some benefits are eventually paid.

First-party claims and third-party claims

Start with the relationship.

A first-party claim is a claim under your own policy. Examples include medical payments coverage, uninsured motorist coverage, or underinsured motorist coverage. In that setting, your insurer owes duties to you because it sold you the policy and accepted your premiums.

A third-party claim is different. That usually means you are dealing with the at-fault driver's insurance company. That insurer did not make a contract with you, so the legal duties are not the same.

For Colorado bad faith cases, the main focus is usually the first-party insurer. If you are unsure whether the company is genuinely reviewing your claim or dragging its feet, it helps to understand how an insurance company investigation is supposed to work. That gives you a useful baseline for spotting conduct that falls short of fair claim handling.

The two legal tracks

Colorado recognizes two main ways to bring a bad faith claim against a first-party insurer: common-law bad faith and statutory bad faith.

The difference often confuses people, so it helps to sort them by what must be proven.

Statutory bad faith focuses on whether the insurer unreasonably delayed or denied benefits. The core question is practical. Did the company have a reasonable basis for what it did?

Common-law bad faith asks for more. The policyholder must show the insurer acted unreasonably and did so with knowledge, or reckless disregard, that its position lacked a reasonable basis.

A simple comparison helps. Statutory bad faith looks at the fairness of the company's conduct. Common-law bad faith looks at the same conduct but also examines the insurer's state of mind.

| Claim type | Basic focus | What the injured person must show |

|---|---|---|

| Statutory bad faith | Unreasonable delay or denial | The insurer lacked a reasonable basis |

| Common-law bad faith | Unreasonable conduct plus culpable mental state | The insurer acted unreasonably with knowledge or reckless disregard |

You usually do not sue the adjuster personally

This point matters because many people aim their frustration at the person whose name appears on the emails.

An adjuster may be the one requesting the same records again, minimizing your doctor's opinion, or sending the denial letter. Even so, Colorado law generally directs a bad faith claim against the insurance company, not the individual adjuster. The company controls the claim process, sets the standards, and owes the duty tied to the policy.

That does not excuse rude or unfair conduct by an adjuster. It means the legal target is usually the insurer itself.

Practical rule: If you believe your claim was handled in bad faith, your lawyer will usually focus on the insurance company, not the individual employee assigned to your file.

What “unreasonable” means in real life

Courts use the word “unreasonable,” but claimants usually experience it in ordinary, concrete ways.

It can mean the insurer ignored important medical records while highlighting minor facts that help its position. It can mean the company delayed a decision without a valid explanation, misread its own policy, demanded cumulative paperwork, or evaluated the claim with a result-first mindset instead of an honest review.

That last point is important. Fair claim handling is supposed to work like a balanced scale. The insurer should put all relevant facts on the scale, not press down on one side with only the evidence that saves money.

If your claim process feels slanted, inconsistent, or built to wear you down, that concern is not trivial. In Colorado, bad faith is often found by examining how the insurer handled the road to a decision, not just the letter it sent at the end.

Recognizing Bad Faith Tactics by Insurers

Bad faith becomes easier to understand when you stop thinking in labels and start looking at behavior.

A typical claim file doesn't announce, “we are acting unfairly.” Instead, the insurer's tactics often look procedural. That's why people second-guess themselves. They think the company is just being slow, careful, or bureaucratic. Sometimes that's true. Sometimes it isn't.

What these tactics look like after a crash

Consider a person injured in a rear-end collision. The liability facts are straightforward. The medical treatment is documented. Yet the insurer stalls by saying it still needs “one more review,” then another, then another. Weeks pass. Bills become collections problems. The claimant feels pressure to take less just to end the uncertainty.

That can be a warning sign.

Another example is the lowball offer. The company doesn't deny the claim outright. It offers some money, but only after downplaying the injury, overlooking treatment needs, or pretending the recovery should have been quicker. The tactic is simple. Pay enough to sound reasonable, but not enough to be fair.

You should also watch for process-based problems like these:

- Repeated document requests after you already provided the materials

- Silence after major submissions, especially after records or bills arrive

- Shifting explanations for why the claim hasn't been resolved

- Policy misstatements, where the company describes coverage more narrowly than the policy permits

- Denials without a clear written explanation

For a closer look at how insurers build and defend claim evaluations, this overview of an insurance company investigation process can help you see what may be happening behind the scenes.

Paid claims can still involve bad faith

This is one of the most misunderstood parts of Colorado insurance bad faith law.

Many people assume that once the insurer pays anything, the bad faith issue disappears. That isn't the rule. A Colorado Supreme Court opinion in 2022 confirmed that liability can still exist even if the claim was eventually paid, because the fundamental question is whether the insurer acted unreasonably during the process, as explained in this discussion from McCormick & Murphy.

So if the company spent months dragging its feet, leaning on cherry-picked evidence, or forcing you through an unfair claims process before making payment, that conduct may still matter.

The video below gives a helpful general overview of bad faith concerns people often face in insurance disputes.

A short gut-check table

| Insurer behavior | Why it may matter |

|---|---|

| Delays with no solid explanation | Delay itself can be part of the wrong |

| Partial payment after unfair handling | Payment doesn't automatically erase prior misconduct |

| Denial letter with vague reasoning | You may not be getting the real basis for the decision |

| Offer far below documented losses | The insurer may be undervaluing the claim rather than evaluating it fairly |

If the company's process feels designed to exhaust you into surrender, pay attention. That's often where the real bad faith story lives.

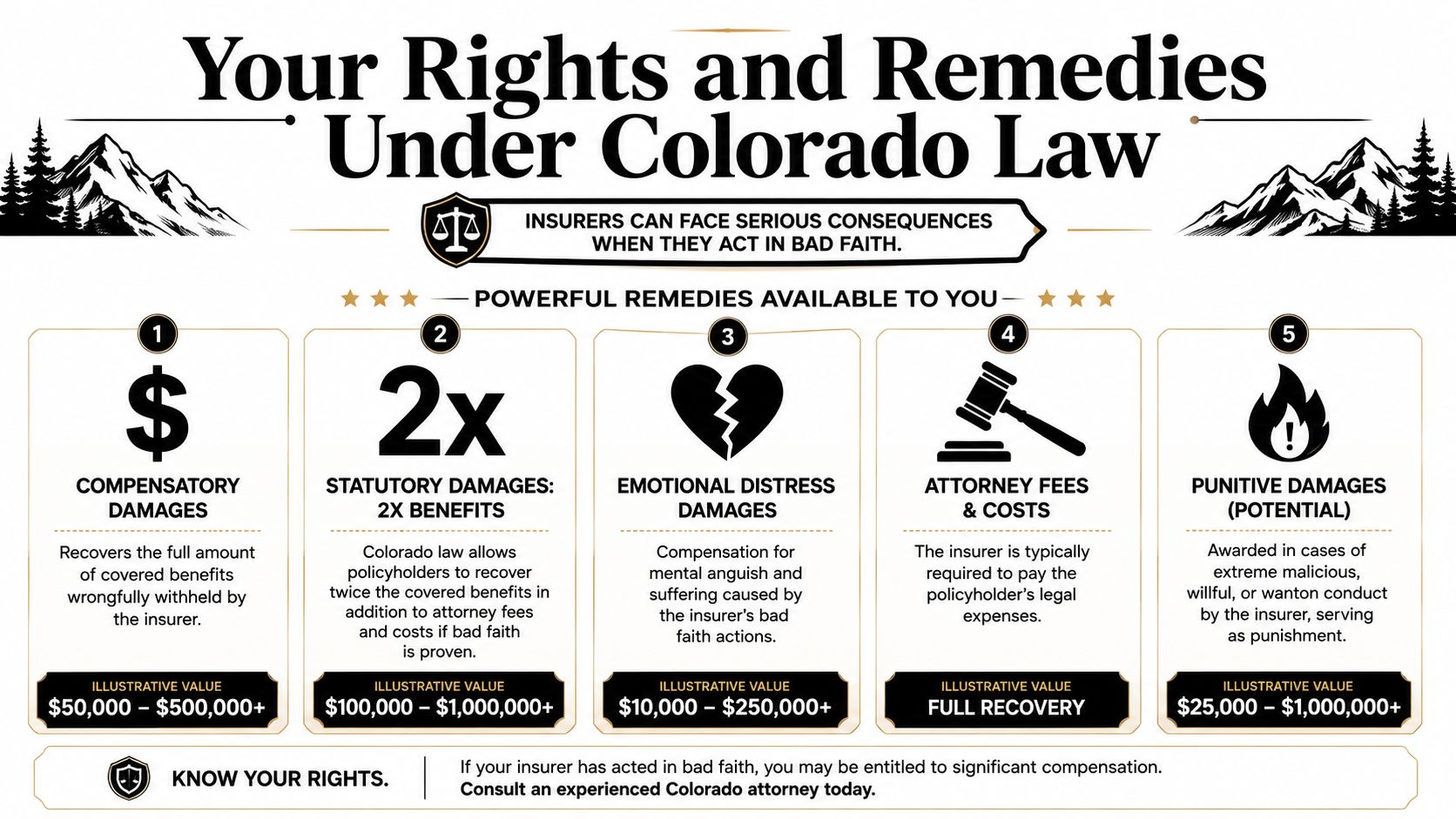

Your Rights and Remedies Under Colorado Law

A lot of injured people hear the same reassurance from an insurance company: if benefits are eventually paid, there is nothing left to fight about. Colorado law does not treat it that easily. The focus is often the insurer's conduct during the claim, not just the final check.

The statutory remedy

Colorado gives policyholders a strong statutory claim when an insurer unreasonably delays or denies payment of covered benefits. Under C.R.S. § 10-3-1116(1), a successful claimant can recover two times the covered benefit plus the covered benefit itself.

A simple example helps. A discussion from Robinson & Henry explains that if an insurer unreasonably denies an $80,000 covered medical claim, the policyholder may seek $160,000 in statutory damages plus the original $80,000 benefit, for a total of $240,000.

That remedy matters because it changes the insurer's risk. Delay is no longer cost-free.

Colorado's statute also allows recovery of reasonable attorney fees and court costs in a proper bad faith case. For many families, that point is practical, not academic. It can make it possible to bring a claim that would otherwise be too expensive to pursue.

The common-law remedy

Colorado also recognizes common-law bad faith. That claim addresses the insurer's unreasonable handling of the claim and can allow recovery for harm beyond unpaid policy benefits.

Depending on the facts, those damages may include compensation for emotional distress and other losses caused by the insurer's misconduct. In cases involving willful and wanton conduct, punitive damages may also be available under Colorado law. If the same conduct also violates the Colorado Consumer Protection Act, other remedies may come into play as well.

The label matters less than the idea behind it. Statutory bad faith is one tool. Common-law bad faith is another. A lawyer often evaluates both.

Two points many Colorado claimants miss

First, a later payment does not automatically erase earlier misconduct. If the insurer used an unfair process, stalled without a reasonable basis, or forced you through needless obstacles before paying, the bad faith issue may still exist.

Second, the claim is usually against the insurance company, not the individual adjuster. That surprises many people, especially when one adjuster was the face of the mistreatment. In Colorado, the adjuster generally is not someone you sue personally for bad faith. The legal focus is on the insurer and how the company handled the claim.

That distinction can save time and confusion early in the case.

What these remedies do in the real world

An insurance claim works a lot like a contract with a referee built into the system. The company promises to evaluate and pay covered claims fairly. Colorado law steps in when the referee starts favoring one side and breaking the rules.

Here is what that can mean for you:

- More than the unpaid claim amount may be recoverable

- Attorney fees and costs may be available under the statute

- Emotional distress damages may be available in a common-law claim

- Punitive damages may be possible in cases involving especially serious misconduct

That does not mean every denial becomes a bad faith case. A genuine dispute over value is different from an unreasonable claim process. The details matter, especially the timeline, the explanations the insurer gave, and whether those explanations held up when the evidence was reviewed.

Denial, appeal, and bad faith are different tracks

People often blend these together because they happen around the same claim. The law treats them as separate questions.

An appeal asks, “Was the company wrong to deny or underpay my claim?” A bad faith claim asks, “Did the company handle my claim unreasonably?”

Sometimes you pursue both. If you are trying to sort out the first path, this guide on how to appeal an insurance claim denial explains that process in plain English.

A contract claim focuses on benefits owed. A bad faith claim focuses on the insurer's unfair conduct while deciding whether to pay those benefits.

For many Colorado victims, that is the turning point in understanding their rights. The case may be about the money owed under the policy, but it may also be about the way the insurer treated you while you were trying to get back on your feet.

Protecting Your Claim from Insurance Company Tactics

A common claim pattern looks like this. The insurer stays polite, asks for one more form, one more statement, one more exam, and then months later says it still needs more time. If that has happened to you, the safest response is not to argue louder. It is to build a record that shows, step by step, what the company asked for, when you gave it, and how the process unfolded.

Build a record that shows the whole process

Bad faith cases often turn on process. The question is not only whether the insurer eventually paid something. The question is whether it handled the claim fairly while making its decision. A clean paper trail helps answer that.

Treat your claim file like a timeline you may need to hand to a judge later. Save every email, letter, portal message, voicemail summary, bill, and explanation from the insurer. After any phone call, write down the date, time, who spoke, and what was said. Then send a short follow-up email confirming your understanding.

That habit serves two purposes. It reduces later disputes about what was said, and it makes it harder for the insurer to blur the sequence of events.

Keep your materials organized in separate folders:

- Claim correspondence, including emails, letters, text messages, portal uploads, and denial notices

- Medical records and bills related to your injuries and treatment

- Repair estimates and photos for vehicle or property damage

- Lost wage documents such as pay stubs, employer letters, and missed-time records

- A communication log with dates, names, and short summaries

A jury usually sees a claim through documents first. Clear records make unfair conduct easier to spot.

Be careful with routine-looking requests

Some insurer requests are ordinary. Some can change the direction of your claim in a serious way.

Read medical authorizations closely. Review recorded statement requests before agreeing to them. Do not sign a release just because a check is attached. A release can close out rights you did not mean to give up, including future parts of the claim that are still developing.

Insurer-requested medical exams deserve special attention. The company may call it an evaluation, but the exam can become a tool for minimizing injuries or disputing treatment. If you have been told to attend one, this guide to an independent medical examination explains how that process works and what to watch for.

Ask the insurer to commit to a specific explanation

Vague claim handling creates room for delay. Specific written explanations create accountability.

If the insurer says your claim is under review, ask what information is still needed. If it denies or underpays the claim, ask it to identify the policy language, the facts it relied on, and the reason for its decision in writing. If the explanation changes later, save both versions.

That matters because unfair conduct often shows up in the gaps. One month the insurer says it needs medical records. The next month it says liability is unclear. Then it makes a partial payment and acts as if the earlier delay no longer matters. In Colorado, a bad faith issue can still exist even if the insurer eventually pays. Payment does not erase an unreasonable process.

It also helps to keep your focus on the company itself. Adjusters make many of the day-to-day decisions, but Colorado law generally does not allow you to sue the individual adjuster personally for bad faith. The claim is usually against the insurer. That makes your documentation of the company's actions especially important.

Practical steps that protect your position

Use one master timeline for the life of the claim. Start with the date of loss, then add each document request, each submission, each phone call, each payment, and each explanation the insurer gives.

Keep treatment records current. Gaps in care and missing notes often become talking points for underpayment.

Confirm oral conversations in writing the same day if possible.

Save every version of letters and emails. Small wording changes can reveal a shift in the insurer's position.

Get legal advice before signing any release or broad authorization.

For a broader consumer-side view of how injury claims are built and presented, SkipCalls' personal injury playbook gives useful context on how documentation and intake shape the strength of a case.

Watch the clock while you document the file

Deadlines do not pause because the insurer says it is still investigating. Colorado bad faith claims are subject to limitation periods, and waiting too long can damage an otherwise valid case.

That is why record-building and deadline awareness need to happen at the same time. If the insurer has been delaying, shifting reasons, requesting the same materials again, or paying part of the claim while handling the rest unfairly, protect yourself early. Time can weaken a claim in two ways at once. It can erase evidence, and it can run down the period you have to act.

When to Hire a Bad Faith Insurance Lawyer

Some claim problems are manageable. Others stop being paperwork disputes and start becoming legal fights. That's usually the point where handling the claim alone becomes risky.

You should strongly consider a lawyer when the insurer denies a serious injury claim without a clear explanation, makes an offer that doesn't line up with the medical reality, stops communicating, or keeps shifting the reason for delay. Those aren't just frustrating events. They can be clues that the company is positioning the file to save itself money.

Bad faith cases are also document-heavy and strategy-heavy. The insurer has its own records, internal notes, supervisors, lawyers, and claim protocols. Trying to uncover and present that story by yourself is like trying to rebuild a truck engine with a kitchen spoon. Effort alone won't solve the tool problem.

A lawyer can identify whether the issue is a contract dispute, a valuation fight, a statutory bad faith claim, a common-law claim, or some combination. Just as important, counsel can preserve evidence, frame the demand properly, and keep the insurer from defining the narrative.

If you want a broader consumer-side look at how injury cases are evaluated and why case presentation matters, SkipCalls' personal injury playbook offers useful context on how claims move from intake to action.

The right time to get help is usually earlier than people think. Not because every rough claim becomes a lawsuit, but because early mistakes can close doors that were open at the start.

Frequently Asked Questions About Insurance Bad Faith

Can my own insurer act in bad faith on a UM or UIM claim

Yes. A first-party claim against your own insurer can lead to a bad faith issue if the company handles the claim unfairly. That's one reason uninsured and underinsured motorist claims deserve close attention. Your insurer may wear the friendly label of “your company,” but it still has financial incentives during claim evaluation.

What's the difference between breach of contract and bad faith

A breach of contract claim focuses on whether the insurer owed benefits under the policy and failed to pay them. A bad faith claim focuses on whether the insurer handled the claim unreasonably. Those are related, but they are not identical. An insurer can create bad faith exposure through unfair claim handling, not just through a final refusal to pay.

If the insurer paid part of my claim, is that the end of it

Not necessarily. Partial payment does not automatically wipe out concerns about the insurer's conduct. If the claim process involved unreasonable delay, selective investigation, or other unfair handling, there may still be a legal issue worth reviewing.

Can I sue the adjuster who handled my claim

In Colorado, bad faith claims are generally brought against the insurance company, not the individual adjuster. That's frustrating for many people because the adjuster is the face of the problem. But legal responsibility usually runs to the insurer.

What should I save if I think bad faith is happening

Keep the policy, claim letters, emails, claim portal messages, denial explanations, medical records, bills, repair documents, and notes of every call. Save anything that helps show what the insurer knew, when it knew it, and how it responded.

If an insurance company has delayed, underpaid, or unfairly denied your claim after a Colorado crash, Nares Law Group LLC can help you understand your options. The firm represents injured people and families facing serious motor vehicle and truck accident claims, and it brings compassionate guidance to a process that often feels stacked against you. A consultation can help you figure out whether you're dealing with a simple claim dispute or something more serious under Colorado bad faith law.