The days after a serious crash often feel less like recovery and more like triage. Bills start arriving before you've even figured out your treatment plan. Work calls stop. Insurance letters keep coming. If you're a parent, spouse, or the person who usually keeps the household running, the question gets very practical very fast: how is this going to affect our family financially?

That's where economic damages calculation matters. This isn't just a lawyer's phrase. It's the process of putting a reliable value on the financial harm an accident caused, so you can seek money for the losses you can measure. In plain terms, it asks what the injury has cost you already, what it will cost you later, and what support you'll need to rebuild a stable future.

After an Accident What Does Full Compensation Mean

A lot of people hear “full compensation” and think it means one big settlement that somehow covers everything. But when you're living through the aftermath of a crash in Colorado, the issue feels much more personal. You may be staring at an emergency room bill, wondering how long your paycheck will be interrupted, and worrying whether your injuries will change the kind of work you can do next year.

That's why it helps to separate two ideas that often get blended together.

Economic damages are the losses you can calculate. Medical bills. lost pay. future treatment. the cost of replacing help you used to provide at home. Non-economic damages are different. They address human harm that doesn't come with a receipt, such as pain, emotional suffering, and loss of enjoyment of life. If you want a clearer explanation of that second category, Nares Law Group has a helpful guide on how pain and suffering is proven.

What clients usually mean by full compensation

When clients sit down in my office, they rarely start by saying, “I need an economic damages model.” They say things like:

- I can't miss more work: The mortgage is due whether your shoulder heals or not.

- I don't know what future treatment will cost: You've been told you may need ongoing therapy, injections, or surgery.

- My life at home has changed: You used to do the driving, lifting, cleaning, childcare, or yard work, and now someone else has to do it.

- I'm afraid of settling too soon: Once a case resolves, you usually don't get a second chance to ask for more because a later expense showed up.

Full compensation, in real life, means enough financial support to cover what the injury took from your household and what it will continue to take in the future.

That's why this process matters. A careful economic damages calculation isn't about inflating a claim. It's about making sure the numbers reflect the life you were living before the crash, and the life you now have to finance after it.

The Building Blocks of Your Economic Claim

Economic losses usually come in layers. Some are obvious the first week. Others don't become clear until your doctor talks about restrictions, surgery, retraining, or long-term care.

Medical costs are more than the first round of bills

Past medical expenses are the easiest place to start because they leave a paper trail. Ambulance charges, emergency care, imaging, surgery, medications, follow-up visits, and physical therapy all belong in the picture if they relate to the accident.

Future medical costs can be harder because they haven't happened yet. But that doesn't make them less real. If your providers say you'll likely need continuing treatment, those projected costs may become part of the claim.

Useful records include:

- Billing statements: Hospital, specialist, rehab, pharmacy, and therapy statements

- Treatment records: Progress notes, referrals, discharge plans, and physician recommendations

- Out-of-pocket proof: Receipts for co-pays, medical equipment, parking, and travel connected to care

Lost income is not the same as lost earning capacity

If you missed work after the crash, that's usually lost income. If the injury changes what you can earn going forward, that may be lost earning capacity.

For personal injury cases, expert models often begin with historical earnings and then project expected earnings using work-life expectancy, labor-force participation, and career progression. Those models may also include fringe benefits, because employer retirement contributions, group insurance, and payroll taxes can significantly increase the loss base, as explained in the Knowles Group's discussion of economic damage calculation inputs.

A simple way to think about it is this:

| Damage Component | Required Documentation Examples |

|---|---|

| Medical expenses | Hospital bills, provider invoices, prescriptions, treatment notes, future care recommendations |

| Lost wages | Pay stubs, W-2s, tax returns, employer wage verification, attendance records |

| Lost earning capacity | Work restrictions, vocational records, employment history, tax returns, expert analysis |

| Household services | Invoices for cleaning, childcare, home help, repair help, statements describing tasks you can no longer do |

| Property damage | Repair estimates, repair invoices, replacement receipts, photographs, valuation documents |

Household services count because your time had value

This category gets overlooked all the time. If you used to mow the lawn, cook, drive kids to school, shovel snow, care for a family member, or handle home maintenance, your injury may force the family to pay someone else to do those jobs.

That loss is economic because it has a replacement cost. It may not come through payroll. It still affects the family budget.

Property damage is part of the picture, but not the whole picture

Vehicle repair or replacement often gets attention first because it's immediate. But in a serious injury case, property damage is often the smallest part of the overall financial harm. Don't let a quick conversation about the car distract from the much larger issue of your body, your work, and your future.

Practical rule: Save every document, even if it seems minor. A single parking receipt won't decide a case, but a complete pattern of records makes your claim far more credible.

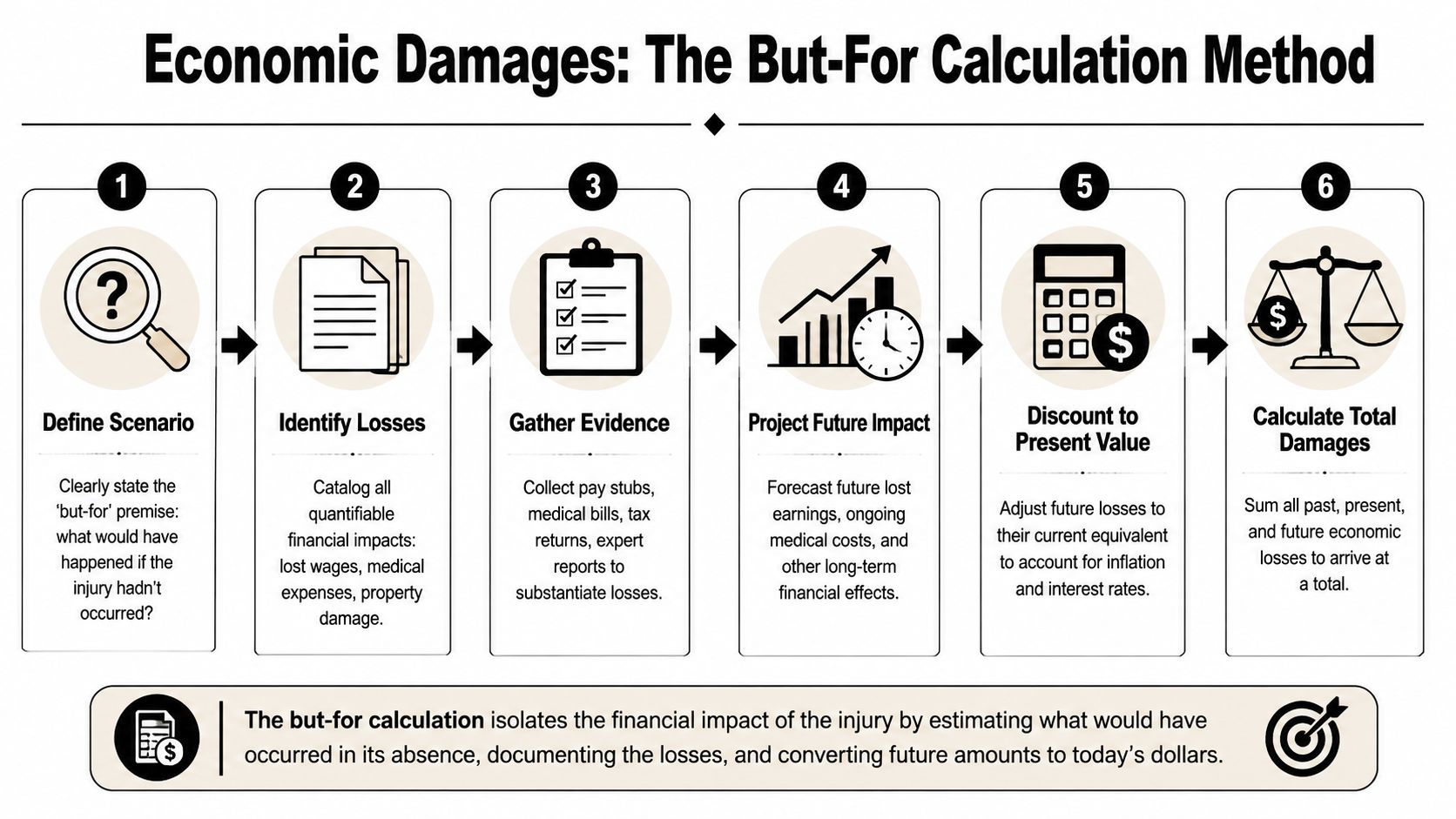

The Math Behind The Numbers A Step-by-Step Method

At the center of economic damages calculation is one core question: what would your financial life have looked like if the injury had never happened?

That's known as a but-for analysis. The Federal Judicial Center explains the basic method this way: the expert compares the plaintiff's actual economic position with the position the plaintiff would have been in had the harmful event not occurred. Damages equal the difference between the but-for value and the actual value, and they are measured net of avoided costs, as described in the Federal Judicial Center's reference guide on estimation of economic losses.

The but-for question in plain English

If a Denver driver is hurt in a truck crash, the model asks two parallel questions.

First, what would that person likely have earned, spent, and retained if the crash never occurred?

Second, what happened instead?

The gap between those two paths is where damages live.

The basic sequence lawyers and experts use

Most serious cases follow a method something like this:

- Define the starting point: Income history, work pattern, benefits, medical status, and household role before the crash.

- Measure past losses: Bills already incurred, wages already missed, and property loss already documented.

- Project future losses: Ongoing care, reduced work ability, or needed support over time.

- Account for offsets: Some expenses may have been avoided because of the injury, and the method aims to capture net loss rather than gross numbers.

- Discount future losses to present value: Future dollars are converted into a current lump sum.

- Test assumptions: Reliable models are transparent about what changes if a key assumption changes.

For readers who want another perspective on the mechanics, Lighthouse Consultants offers expert insights on quantifying financial losses that are useful for understanding how professionals approach return-of-earnings and loss questions.

Why present value confuses people

This is the part many clients dislike at first. They hear that future losses are being reduced to a present number and think someone is cutting down their claim.

A better analogy is a garden hose and a water tank. If you know you'll need water over time, you don't need every future gallon delivered today in separate trucks. You need one tank today that, if managed properly, supplies the flow when needed. Present value works the same way. A lump sum paid now is intended to fund future losses as they arise.

That's also why details matter. If the discount approach is unfair, the current lump sum may be too small to cover the actual future need. If it's done carefully, it's designed to match future losses in today's dollars.

The number on a demand or verdict form may look smaller than the raw total of all future bills added together. That doesn't automatically mean it's wrong. It means someone has translated a stream of future losses into a present-day amount.

One related issue comes up in vehicle claims too. If your car was unusable after a collision, there may be a separate conversation about loss of use damages in an auto insurance claim, which is distinct from injury-based financial loss but often part of the overall recovery picture.

A Calculated Example From Accident to Award

Consider a Colorado construction foreman injured in a truck collision on I-25. Before the crash, he supervised crews, climbed ladders, inspected active sites, and worked long days that depended on mobility and stamina. After the collision, he can still think clearly and manage people, but he can't safely perform the physical parts of the job that made him valuable in that role.

Start with the life he actually had

His file might include medical bills, payroll records, tax returns, employer benefit information, and treatment recommendations. Those documents create the baseline. They show what his work life looked like before the wreck and what changed afterward.

The story behind the numbers matters here. A lower back injury on paper may really mean he can't return to the trade he built over years. A shoulder injury may mean he now needs retraining for a less physical role. Lost earning capacity, in human terms, may be the money needed to support a career pivot the injury forced on him.

Then compare two futures

One future is the but-for path. He stays in construction supervision, continues earning along his expected path, and keeps receiving the benefits tied to that work.

The other future is the post-crash path. He misses work during treatment. He returns with restrictions. He may move to a less demanding position, work fewer hours, or leave the field entirely.

A credible model would compare those paths and ask:

- What income did he already lose while out of work

- What benefits were tied to that employment

- What future care is medically supported

- What household tasks now require paid help

- What earnings gap is likely to continue because of permanent restrictions

That process is easier to grasp when you hear it explained visually, especially if you're trying to understand how lawyers package these losses in a serious injury claim.

Why the award is about future stability

A good damages presentation doesn't treat him like a spreadsheet. It connects every category to a real need. Future treatment means keeping pain manageable enough to function. Reduced earning capacity means replacing income he would have used to support his family. Household help means his spouse doesn't have to absorb every burden alone.

That's the point of the exercise. Not a bigger pile of numbers for its own sake. A more accurate picture of what it will take to keep a family financially secure after a life-changing injury.

Common Pitfalls and Insurance Company Defenses

Insurance companies rarely challenge the idea that a crash costs money. They challenge the amount, the cause, and the certainty of the loss. Their job is to narrow the number. Your job is to make the number defensible.

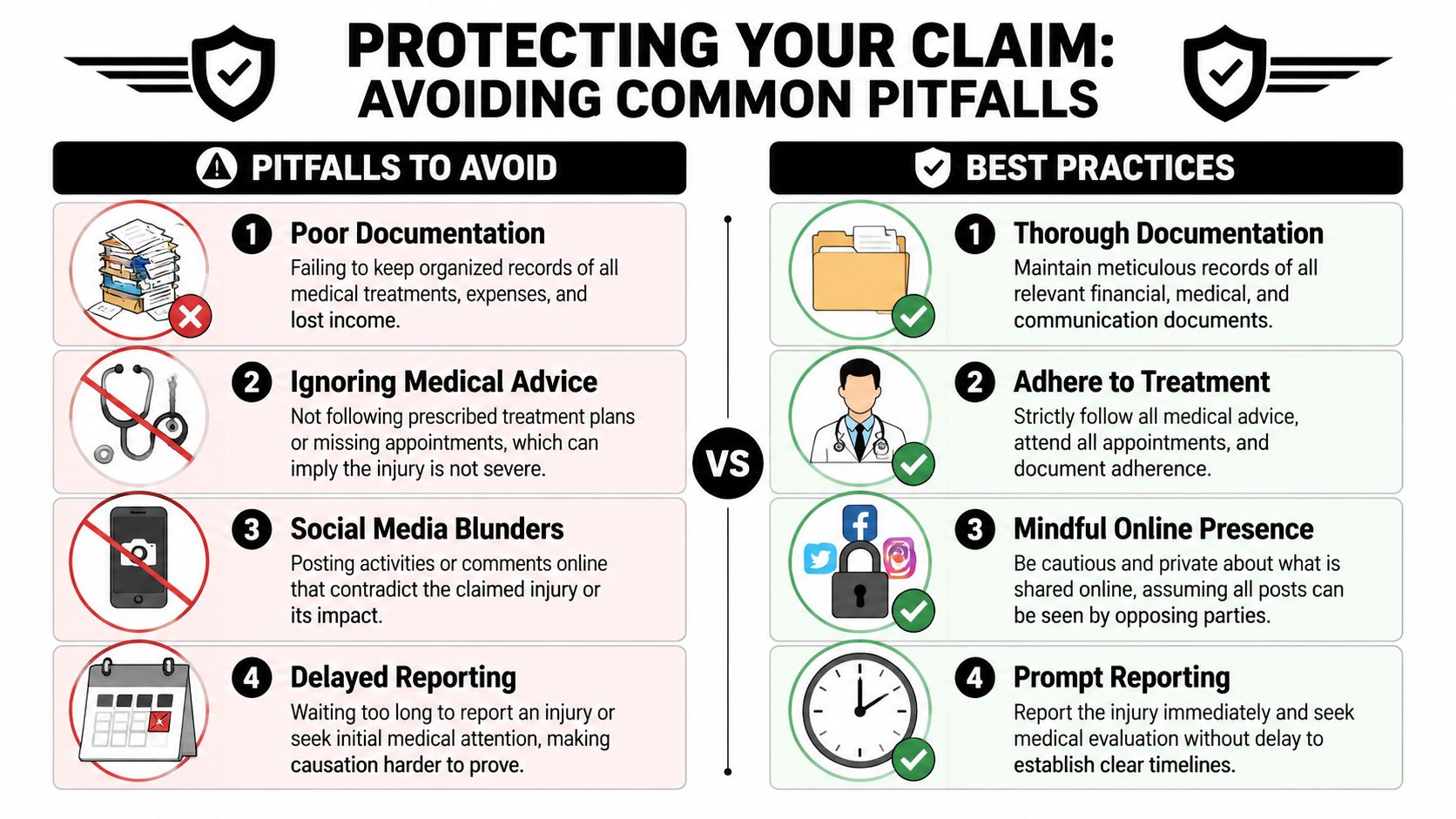

Where claims often weaken

Some problems start innocently. People are hurt, overwhelmed, and trying to get through the week. But small gaps can become major arguments later.

Common trouble spots include:

- Incomplete records: Missing bills, missing wage documents, or no organized proof of out-of-pocket spending

- Treatment gaps: Long breaks in care that let the insurer argue the injury improved or wasn't serious

- Unsupported future claims: Asking for future losses without medical or vocational support

- Online contradictions: Social media posts that don't reflect the restrictions being claimed

- Early settlement pressure: Accepting money before the long-term picture is clear

How insurers attack the math

In complex cases, the defense often aims at the assumptions underneath the model.

They may say future wage loss is speculative. They may argue your medical care won't last as long as your doctor expects. They may push for assumptions that shrink the present value of future loss. They may also claim some part of your financial downturn came from something other than the crash.

One especially important issue is double recovery. A credible model has to avoid counting the same loss twice. Anthem Forensics highlights the need for mutual exclusivity so future medical needs, lost earnings, retirement benefits, and household services are documented and discounted separately without overlap in its discussion of economic damages and duplication safeguards.

A strong claim doesn't just ask for more. It shows why each category is separate, supported, and not duplicative.

What you can do right now

If you're still in the early phase of a Colorado case, these habits help protect your claim:

- Follow medical advice: Keep appointments, complete treatment, and tell providers about ongoing symptoms

- Create one file system: Save bills, receipts, wage records, insurer letters, and mileage logs in one place

- Be careful online: Assume the defense will try to use posts, photos, and comments against you

- Report losses as they happen: Don't wait months to tell your lawyer or insurer about missed work or paid household help

If you're dealing with adjusters directly, this guide on handling insurance after a car accident can help you avoid common mistakes that make economic losses harder to prove later.

The Role of Experts and Colorado-Specific Rules

A serious injury case often turns on a hard question. How do you prove losses that have not fully happened yet, but are already reshaping your life?

If a back injury keeps a warehouse worker from lifting, the issue is not only next week's missed paycheck. It may also be the cost of retraining for lighter work, the difference between old wages and new wages, and the long-term effect on retirement benefits. In a wrongful death case, the numbers may reflect income, household services, and financial support a family expected to receive for years. Experts help translate those life changes into evidence a court or insurer can test.

Why expert help matters in bigger cases

Each expert covers a different part of the story.

A treating physician explains the injury, the limits it causes, and whether those limits are likely to last. A vocational expert examines what work a person can still perform, whether retraining is realistic, and how the injury affects earning capacity within the labor market. A life care planner maps out future medical needs, from therapy and medications to equipment or home assistance. A forensic economist then uses those findings to calculate the financial value of those losses over time.

That process works like building a house from separate trades. The doctor identifies the physical restrictions. The vocational expert shows what those restrictions do to work options. The life care planner identifies future support needs. The economist ties those pieces together so the final number rests on facts instead of guesswork.

The defense often attacks future losses as too speculative. Expert analysis answers that attack by showing the chain of cause and effect. As DMA Economics explains in its discussion of causation and valuation in damages modeling, a sound damages model must separate losses caused by the defendant from losses caused by unrelated economic forces.

Colorado law affects the outcome

Colorado adds another layer. The financial model may be accurate and still not be the final number.

Under Colorado's modified comparative negligence rule, C.R.S. § 13-21-111, an injured person's recovery can be reduced by that person's share of fault. For a client, that means two things at once. Your losses need careful proof, and liability facts need equally careful proof. A strong damages presentation matters, but so does showing why the defendant caused the harm in the first place.

Colorado cases also bring local practical issues into play. Judges apply Colorado rules on expert testimony and evidence. Juries in different parts of the state may respond differently to future-loss testimony, especially in cases involving traumatic brain injury, permanent disability, or wrongful death. For that reason, the work is not just math on a spreadsheet. It is a clear explanation of how an injury changed a person's ability to earn, care for a family, and plan for the future.

That human piece matters.

"Lost earning capacity" can sound abstract until you connect it to real life in Colorado. It may mean funding community college courses for a new line of work after construction is no longer possible. It may mean replacing the value of childcare, home maintenance, or transportation help a parent used to provide. The rules of proof exist to test those claims, but the purpose of the claim is much more personal. It is to protect stability after a life has been forced off course.

Securing Your Future with Nares Law Group

When people hear “economic damages calculation,” they often expect something cold and technical. In real cases, it's personal. It's the cost of future surgery. It's the paychecks that stop while healing drags on. It's the money needed to replace a career path an injury interrupted. It's the support that keeps a household functioning when one family member can no longer do what they used to do.

The law tries to translate those losses into numbers because numbers are how courts and insurers make financial responsibility real. But the reason for the calculation is human. A sound claim helps protect housing, treatment access, family stability, and long-term independence.

For Colorado injury victims, especially those dealing with truck wrecks, traumatic brain injuries, or wrongful death, the stakes are usually too high for rough estimates and incomplete paperwork. Serious cases need organized proof, careful modeling, and a strategy built for the defenses that insurers and corporate defendants are likely to raise.

If you're trying to understand what your case may be worth, clarity matters early. So does restraint. The goal isn't to throw out the biggest number possible. The goal is to build a claim that can stand up under scrutiny and fund the future your family now has to manage.

If you need help understanding how economic losses apply to your Colorado injury or wrongful death case, contact Nares Law Group LLC for a free consultation. The firm helps injured people and families evaluate medical costs, lost income, long-term care needs, and other financial harms so they can make informed decisions about settlement, litigation, and the road ahead.