When you’re standing on the side of the road, dazed and confused after a crash, it’s almost impossible to think clearly. The same goes for a sudden slip and fall that leaves you stunned on the floor of a store. Your only focus is the immediate shock and pain.

What you do in these first few minutes and hours, however, can make or break your ability to get fair compensation later. It’s about protecting your health and, at the same time, laying the groundwork for your personal injury claim.

Your First Steps After an Injury in Colorado

The moments after an accident are a blur. Whether you were caught in a multi-car pileup on I-70 or injured on poorly maintained property, your first instinct might be to brush it off or just get out of there. Resist that urge.

Taking a deep breath and methodically working through a few key steps will protect both your physical well-being and your legal rights. It's all about creating a clear, undeniable record of what happened and how it affected you right from the start.

Prioritize Your Health Above All Else

Before anything else, get medical help. This is not the time to be tough or downplay your pain. Adrenaline is a powerful chemical that can easily mask serious injuries like concussions, internal bleeding, or the kind of soft tissue damage that only shows up hours or days later.

It’s a classic mistake. The police or paramedics ask if you’re hurt, and you say, “I think I’m okay.” That one phrase can come back to haunt you. An insurance company will use it to argue your injuries weren’t a result of the accident at all.

Seeing a doctor right away creates an official, time-stamped record connecting your injuries to the incident. This documentation is the single most important piece of evidence you will have. With over 6,500 people injured in car accidents every day and 39.5 million Americans needing medical care for injuries annually, you are far from alone. You can see more on these trends in Clio's latest personal injury statistics report.

Document the Scene Like a Detective

While you wait for help, pull out your smartphone. You have a powerful evidence-gathering tool in your pocket, and the photos you take will tell an unbiased story.

Turn into a crime scene investigator for a few minutes. Capture everything you can:

- Vehicle Damage: Get wide shots showing where the cars ended up, then move in for close-ups of the impact points and any damage.

- The Surroundings: Photograph traffic lights, stop signs, slick spots on the road, skid marks, or anything else that helps explain what happened.

- Your Injuries: Take clear pictures of any cuts, bruises, or swelling. These visible injuries can heal fast, so documenting them immediately is key.

Think of it as creating a visual narrative. You’re building a file that will allow an insurance adjuster—or even a jury—to see the scene exactly as it was.

Interact Carefully with Police and Witnesses

When law enforcement arrives, give them the facts. Stick to what you know for sure and avoid guessing, apologizing, or admitting any fault. Just calmly state what you saw and felt. Before they leave, make sure you get the officer’s name, badge number, and information on how to get a copy of the official police report.

If anyone saw what happened, ask for their contact information. A simple, polite request is usually all it takes. Try something like, “I saw you witnessed the accident. Would you be willing to give me your name and number in case the insurance companies need to talk to someone who was here?”

These three things—getting medical care, documenting the scene, and gathering information—form the bedrock of a strong personal injury claim.

Building Your Case: The Power of Meticulous Documentation

Once your immediate medical needs are handled, your focus has to shift. A strong personal injury claim isn’t built on what you remember; it’s built on what you can prove. Every single photo, receipt, and doctor's note becomes a piece of the puzzle, forming a clear picture of what this injury has cost you.

From this moment on, you are the chief historian of your own story. Insurance adjusters live and breathe paperwork. A disorganized claim is an easy target. A well-documented file is your strongest shield against their attempts to downplay or deny what happened.

More Than Medical Bills: Capturing the Human Cost

A huge part of your claim’s value comes from something the law calls "pain and suffering." This isn't about bills; it's about the very real, human impact of your injury. This is where a simple personal injury journal becomes one of the most powerful tools you have. It can be a basic notebook or even a note-taking app on your phone.

The goal is to capture the details that medical charts will always miss.

- Your Daily Pain: Use a simple 1-10 scale to log your pain levels. Be specific. Instead of "my back hurts," write "sharp, stabbing pain in my lower right back, an 8/10 when I try to get out of bed."

- The Emotional Toll: Note your feelings. Are you anxious about driving? Frustrated that you can't do simple things? Depressed because you missed a family wedding? Write it down.

- Life's Interruptions: Record every single time your injury got in the way. Maybe you needed help tying your shoes. Perhaps you couldn't pick up your toddler or walk your dog. These details matter.

A journal entry that says, "Couldn't sleep again because of the throbbing in my shoulder. Had to cancel plans to take my daughter to the park and felt a wave of guilt all day," tells a much more powerful story than just saying you have shoulder pain. It puts a face on the injury.

These entries create a running narrative of your recovery. They provide concrete, undeniable proof of how this accident has fundamentally changed your quality of life. This is the evidence we use to calculate the true value of your damages.

Getting Your Paperwork in Order

As the bills and records start to pour in, it’s easy to feel buried. The key is to start organizing from day one. A simple binder with dividers or a set of digital folders on your computer will do the trick.

Start collecting every piece of paper related to the accident. This isn't just about the major hospital bills; it's about every small expense that adds up over time.

To get you started, here is a checklist of the essential documents you’ll need to build a strong foundation for your claim. This isn't just about collecting papers; it's about gathering the specific evidence needed to prove every aspect of your case to an insurance company.

Essential Documentation Checklist for Your Claim

Use this checklist to collect and organize the critical documents needed to support your personal injury claim in Colorado.

| Document Category | Specific Items to Collect | Why It's Important |

|---|---|---|

| Accident Scene Evidence | Police/accident reports, photos/videos of the scene, witness contact information, photos of your injuries. | Establishes how the accident happened, who was at fault, and the immediate aftermath. |

| Medical Records & Bills | ER reports, ambulance bills, hospital records, surgeon's notes, physical therapy reports, X-ray/MRI results. | Proves the extent of your injuries and documents the full cost of your medical treatment. |

| Proof of Lost Income | Pay stubs from before and after the injury, a letter from your employer confirming missed time, tax returns. | Shows the exact amount of wages you lost because you were unable to work. |

| Out-of-Pocket Expenses | Receipts for prescriptions, medical devices (crutches, braces), mileage/parking for appointments, co-pays. | Recovers all the "smaller" costs that add up quickly and would not have existed without the injury. |

| Personal Injury Journal | Daily notes on pain levels, emotional state, sleep disruptions, and missed activities. | Provides a human narrative of your suffering and demonstrates the non-economic impact on your life. |

This collection of documents does more than just list your expenses. It tells a complete story. It transforms your claim from a simple request for money into a well-supported, fact-based demand that an insurance adjuster is forced to take seriously.

Navigating Insurance Companies and Demand Letters

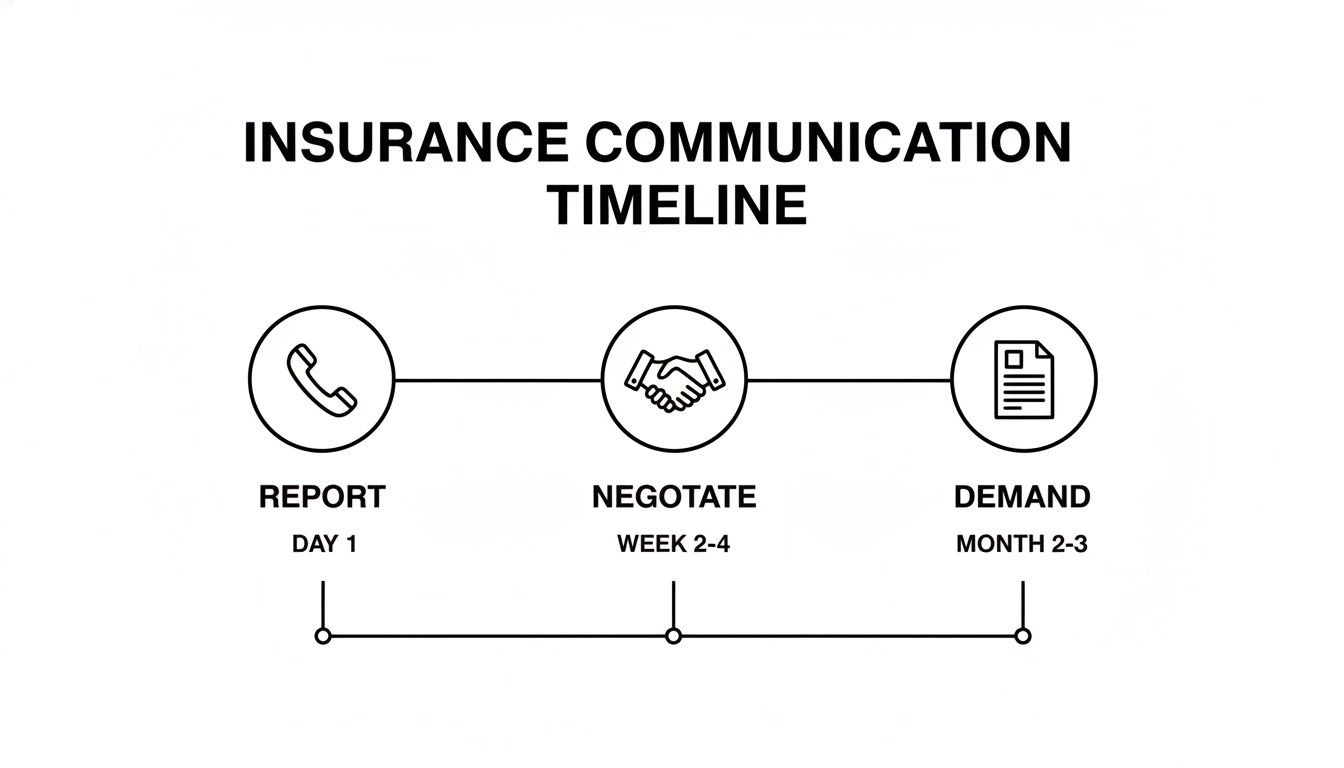

Once you've started documenting your injuries, you'll enter what feels like a chess match with the insurance companies. This is where things can get tricky. Insurance adjusters are trained professionals whose only job is to protect their company’s bottom line by minimizing what they pay out. Your job is to be just as prepared to protect your own interests.

Your first encounter will almost certainly be a phone call from an adjuster. It's important to remember, no matter how friendly or compassionate they sound, they are not on your side. Their goal is to gather information that could limit their company's liability.

The Initial Phone Call with an Adjuster

Sooner or later, the phone will ring. It’ll be an insurance adjuster. Your approach here should be polite but very firm. You do need to report the accident to your own insurer and the other party’s, but you control what you share.

Keep these things in mind during that first call:

- Stick to the bare facts. Just confirm your name, address, and the date and location of the accident. Don't go into detail about your injuries—you likely don't know the full extent of them yet, anyway.

- Politely decline to give a recorded statement. They will almost always ask for one. You are not required to give it, and doing so without a lawyer is a major risk. Your words can be twisted and used against you later on.

- Never, ever admit fault. Steer clear of any language that sounds like an apology, like "I should have seen them" or even a simple "I'm so sorry." These phrases can be interpreted as an admission of guilt.

A classic adjuster tactic is to offer a quick, lowball settlement just days after the accident. They might say something like, "Let's just get this taken care of right now with a check for $1,000." This is a test. They're seeing if you're desperate or don't know your rights. If you take that check, your claim is closed for good—even if you find out later your injuries are far more serious.

Understanding the Insurer's Perspective

It’s helpful to know what you’re walking into. Insurance is a massive industry, and for them, handling claims is a numbers game. You should notify the insurers promptly, but never sign away your rights without getting legal advice.

Consider this: insurers are known to deny or underpay claims for 62 million injury-related medical visits every single year. As the personal injury legal market grows toward $61.3 billion and average auto bodily injury claims are projected to hit $27,373 by 2026, the pressure on adjusters to control costs is intense. You can explore the latest personal injury statistics to see the trends that shape how they'll handle your case.

Crafting a Powerful Demand Letter

After you have a firm grasp of your injuries and have collected all your medical records and bills, it's time to formally ask for compensation. This is done with a demand letter.

This isn't just any letter. It's a structured legal document that lays out your entire case from start to finish. It’s your opening argument, presented in a clear and compelling narrative.

A strong demand letter needs to accomplish a few key things. It must:

- Explain the facts of the accident and why the other party is responsible.

- Provide a detailed summary of your injuries, backed up by your medical records.

- Include a full accounting of all your economic damages, like medical bills and lost wages.

- Make a clear and reasoned case for your non-economic damages, like pain and suffering.

- State a specific, total dollar amount you are demanding to settle the claim.

The heart of the letter is how you calculate your damages. You’ll add up all your medical expenses and lost income to find your "special," or economic, damages. For "general," or non-economic, damages, a common approach is to apply a multiplier (usually between 1.5 and 5) to your economic damages. The more severe and permanent your injuries, the higher that multiplier should be. You can learn more about the demand preparation stage of a personal injury case to get a better handle on this crucial step.

Sending a well-organized and persuasive demand letter sets a serious, professional tone. It shows the insurance company that you've done your homework, built a solid case, and are ready to fight for a fair result.

The Unforgiving Clock: Understanding Colorado's Statute of Limitations

After an injury, time feels strange. Some days drag on, filled with pain and appointments, while weeks disappear in a blur. But in the legal world, time moves with unforgiving precision. From the moment you are hurt, a clock starts ticking.

If that clock runs out before you file a lawsuit, your right to compensation is gone. Forever. It doesn’t matter how clear the fault was or how severe your injuries are. This legal deadline is called the statute of limitations, and in Colorado, it’s a rule with very few exceptions.

Missing this deadline isn't a simple mistake—it's a fatal blow to your claim. The court will have no choice but to dismiss your case, leaving you with no way to recover your losses.

With nearly 400,000 personal injury cases filed in U.S. state courts each year, the system is busy. You can't afford to wait. Even while you're negotiating with an insurance company, that legal deadline is quietly approaching. If talks stall, you must file a suit to keep your claim alive. You can see more data on these filing trends and their impact by checking the 2026 Injury Impact Report.

Colorado's Main Personal Injury Deadlines

The specific deadline for your case depends on what happened and who was responsible. While there’s a general rule, some crucial exceptions can drastically shorten your window to act.

Here are the timelines you need to know in Colorado:

- Motor Vehicle Accidents: For injuries from a car, truck, or motorcycle crash, you have three years from the date of the accident to file a lawsuit.

- Most Other Personal Injury Claims: For incidents like a slip and fall or dog bite, the deadline is shorter. You generally have two years from the date you were injured.

- Claims Against the Government: This is where the timeline gets incredibly tight. If you were injured by a government employee or on public property—like a city bus or a poorly maintained park—you have only 182 days to give formal written notice of your claim.

The initial back-and-forth with an insurer has its own rhythm, but it’s completely separate from these hard legal deadlines.

These early insurance steps are just the beginning. They must happen long before the final legal clock runs out.

Lawsuit Deadlines vs. Insurance Deadlines

This is a point of confusion I see all the time. People mix up the deadline to report the claim with the deadline to file a lawsuit. They are not the same thing.

Your own insurance policy will say you need to report an accident "promptly." This is a contractual duty you have with your insurer, and it usually means within a few days or weeks.

The statute of limitations, on the other hand, is a state law that sets the absolute final date for taking your case to court. You can spend months negotiating with an adjuster, but if you pass the statute of limitations without filing a lawsuit, all your leverage vanishes. The insurance company no longer has any legal reason to pay you a dime.

Think of it this way: reporting the crash to the insurance company opens the door for conversation. The statute of limitations is the date the door slams shut for good. Understanding the specific statute of limitation for a car accident is one of the most important things you can do to protect your rights.

Because these deadlines are so strict, getting legal advice early is critical. An attorney can make sure every timeline is identified and met, preserving your ability to pursue the full and fair compensation you deserve.

Knowing When to Hire a Personal Injury Lawyer

Trying to figure out the claims process can be completely overwhelming. It’s natural to wonder if you really need to hire someone or if you can just handle it yourself. For a tiny fender bender with zero injuries, you might be fine. But when the stakes get higher, that's when things change.

An attorney levels the playing field. You have to remember, insurance companies employ teams of professionals whose entire job is to minimize what they pay you. A skilled lawyer pushes back, fighting only for your best interests so you aren’t taken advantage of when you’re most vulnerable.

Clear Signals It's Time to Call an Attorney

Some situations are immediate red flags. They’re clear signs that you need legal guidance right away. Trying to navigate these scenarios on your own can seriously risk your ability to get fair compensation for everything you’ve lost.

You should seriously think about hiring a lawyer if:

- The Injuries Are Serious: Anything beyond minor soreness warrants a conversation. This includes broken bones, concussions, traumatic brain injuries (TBIs), spinal cord damage, or any injury that needs surgery or long-term medical care.

- Fault Is Being Disputed: If the other driver’s insurance company is trying to blame you for the accident, even a little, you need an advocate. Colorado’s modified comparative fault rule means your compensation gets reduced by your percentage of fault. Fighting a false accusation is absolutely critical.

- The Insurer Is Uncooperative: Delay tactics, flat-out denying a valid claim, or making a shockingly low settlement offer are classic signs the insurance company is not negotiating in good faith.

An adjuster's job is to close your file for as little money as possible. If they offer a quick check just days after the accident, it's not because they're being generous—it's because they hope you'll accept it before you realize the true, long-term cost of your injuries.

Spotting these red flags early is vital. You can find more detail on these tricky situations and learn more about when to hire a personal injury attorney to protect your rights.

The Role of a Personal Injury Lawyer

A good personal injury lawyer does so much more than just send a letter. They become your case manager, your strategist, and your advocate, taking the legal weight off your shoulders so you can focus on one thing: getting better.

From the minute you hire them, they take charge. Your attorney will launch a full investigation, gathering police reports, tracking down and interviewing witnesses, and sometimes bringing in accident reconstruction experts to prove exactly what happened. They handle all communication with the insurance companies, shielding you from the constant calls and pressure from adjusters.

As your case moves forward, they meticulously collect every medical record and bill. They work with your doctors to understand your prognosis and then calculate the full scope of your damages—not just what you've already lost, but what you’ll need in the future.

Demystifying the Contingency Fee

One of the first questions people ask is, "How can I afford a lawyer?" The answer is actually one of the best parts of personal injury law: nearly every attorney works on a contingency fee basis.

Here’s what that really means for you:

- You pay zero upfront costs to get your case started.

- The lawyer's fee is simply a percentage of the settlement or verdict they win for you.

- If for some reason they don't secure any money for your claim, you owe them nothing.

This system was designed to give everyone access to top-tier legal help, no matter their bank account balance. It also means your lawyer is directly invested in getting you the best possible outcome. They put their own time and resources on the line because they're confident they can win.

Of course. Here is the rewritten section, adopting the specified human-like, expert tone and style.

Common Questions About Colorado Injury Claims

After an injury, your mind is probably racing with questions. The uncertainty can be overwhelming. As you try to figure out what comes next, you're not just dealing with legal concepts—you're facing real-world problems that affect your family and your finances.

Getting clear, honest answers is the first step toward regaining control. Below, we’ve answered some of the most pressing questions we hear from people in your exact situation.

How Much Is My Personal Injury Claim Worth?

This is almost always the first question we’re asked, and the only honest answer is: it’s complicated. There’s no magic formula or online calculator that can give you a real number. The value of your claim is deeply personal and is tied directly to the specific details of your life.

We figure out what a claim is truly worth by digging into the facts, looking at things like:

- The Severity of Your Injuries: A case involving a traumatic brain injury is worlds apart from one with minor whiplash. The nature of the injury is the foundation of the claim's value.

- Your Total Medical Bills: This isn’t just the ER visit. It’s every single cost, from the ambulance ride to future surgeries, ongoing physical therapy, and prescriptions.

- Lost Wages and Earning Capacity: We calculate the income you've already lost from being out of work, but we also look ahead. We project how your injuries might impact your ability to earn a living in the future.

- The Impact on Your Quality of Life: This is often called "pain and suffering," but it's more than that. It’s the missed family events, the hobbies you can no longer enjoy, and the daily struggles. This is a critical part of your compensation.

You might see reports that the average auto bodily injury claim was around $27,373 in 2026, but that number is practically meaningless for an individual. It’s just an average. Catastrophic injury cases can be worth millions. Be extremely wary of any lawyer who throws out a specific dollar amount before they’ve done a full investigation.

What if I Have to Go to Court?

The thought of a courtroom showdown is enough to make anyone anxious. The good news? It’s incredibly rare. The vast majority of personal injury cases never see the inside of a courtroom.

Statistically, over 90% of personal injury cases settle out of court. This happens through direct, tough negotiation between your attorney and the insurance company.

Trials are expensive, time-consuming, and unpredictable for everyone involved. Because of this, insurance companies would much rather settle.

But a settlement is only a victory if the number is fair. If an insurer refuses to make a reasonable offer that truly covers your losses, filing a lawsuit is the only way to hold them accountable. We prepare every single case as if it’s going to trial. This intense preparation shows the insurance company we mean business, which is often the very thing that convinces them to offer a better settlement.

How Long Does It Take to Settle a Claim?

This process is a marathon, not a sprint. While everyone wants a fast resolution, the timeline can stretch from a few months to well over a year. Sometimes longer.

Several things control the clock:

- Case Complexity: A straightforward rear-end collision where fault is obvious might settle quickly. A multi-vehicle truck accident with disputed liability is going to take much more time to unravel.

- Injury Severity: We can’t even think about settling until you’ve reached Maximum Medical Improvement (MMI). This is the point where your doctor says your condition is stable and they have a clear picture of your long-term medical needs.

- Insurer Cooperation: If the insurance company is negotiating in good faith, things move along. If they start using delay tactics and dragging their feet, the process stalls.

Settling your case before you reach MMI is almost always a huge mistake. You only get one shot to resolve your claim. If you settle too early, you could be left paying for future medical treatments out of your own pocket. A patient, strategic approach ensures you don’t leave money on the table.

What if the Other Driver Was Uninsured?

It’s a nightmare scenario, and unfortunately, it’s all too common here in Colorado. If the driver who hit you has no insurance—or not enough to cover your damages—you’re not out of options. You can turn to your own insurance policy.

This is exactly why Uninsured/Underinsured Motorist (UM/UIM) coverage is so critical. It’s an optional part of your auto policy, but we tell every driver we know to carry as much of it as they can afford.

When you file a UM/UIM claim, you’re making a claim against your own insurance company. They are supposed to "step into the shoes" of the at-fault driver's missing insurance. This can feel strange, even like a conflict of interest. That’s another reason why having an experienced lawyer on your side is so important—to make sure your own insurer treats you fairly and pays the full benefits you’re entitled to.

Navigating the complexities of a personal injury claim can be daunting, but you don't have to do it alone. The team at Nares Law Group LLC is here to provide the clarity, guidance, and aggressive advocacy you need. If you've been injured and have questions, contact us today for a free, no-obligation consultation to protect your rights and secure the future you deserve.