The crash is over, but panic often starts afterward.

You may be sitting in a damaged car on a Colorado road, answering calls from family, trying to calm your breathing, and wondering how you are supposed to pay for an ambulance, a rental car, time off work, and medical care that has only just begun. If the other driver caused the wreck, one question rises above the rest. Who pays for this?

That is where colorado liability insurance becomes more than a policy term. It becomes the financial system that decides whether there is money available for your hospital bills, lost income, vehicle damage, and, in serious cases, the life changes that follow a brain injury, spinal injury, or fatal crash.

Many injured people assume the answer is simple. The at-fault driver has insurance, so the insurance company should cover the harm. In practice, it is rarely that clean. Some drivers carry only the legal minimum. Some carry no insurance at all. Some crashes involve a company vehicle, a trucking policy, or a separate premises liability policy. And Colorado has a few important rules that can either help your recovery or limit it if you do not know they exist.

Your Guide to Colorado Liability Insurance After an Accident

A common scene after a wreck looks like this. Your neck hurts. Your phone battery is low. The other driver says, “Don’t worry, I have insurance.” Later, an adjuster calls and asks for a statement before you even know the full extent of your injuries.

That moment is where many individuals get lost. They hear words like liability, limits, bodily injury, property damage, uninsured motorist, and underinsured motorist, but no one slows down to explain what those terms mean in practice.

Liability insurance is the money pool that may pay when a person or business causes harm. In a car crash, it usually starts with the at-fault driver’s policy. In a truck case, it may involve a commercial vehicle policy. If the injury happened on business property, another kind of liability policy may matter.

The hardest part is that insurance rules sound technical, while your problem is painfully personal. You are not trying to learn insurance for fun. You are trying to find out whether treatment will be covered, whether your lost wages can be replaced, and whether a quick settlement would leave you paying the rest yourself.

Key takeaway: Liability insurance is not just about whether coverage exists. It is about whether the available coverage is enough to match the damage done.

Colorado law gives injured people some useful tools. It also leaves dangerous gaps. Both matter. A driver can follow the law and still carry coverage that falls far short of a serious injury claim. At the same time, Colorado law gives injured people important rights involving policy disclosure and underinsured motorist recovery that many individuals do not fully understand.

If you are dealing with pain, paperwork, and pressure from insurers, clarity matters. The rules below are the ones most likely to affect your financial recovery.

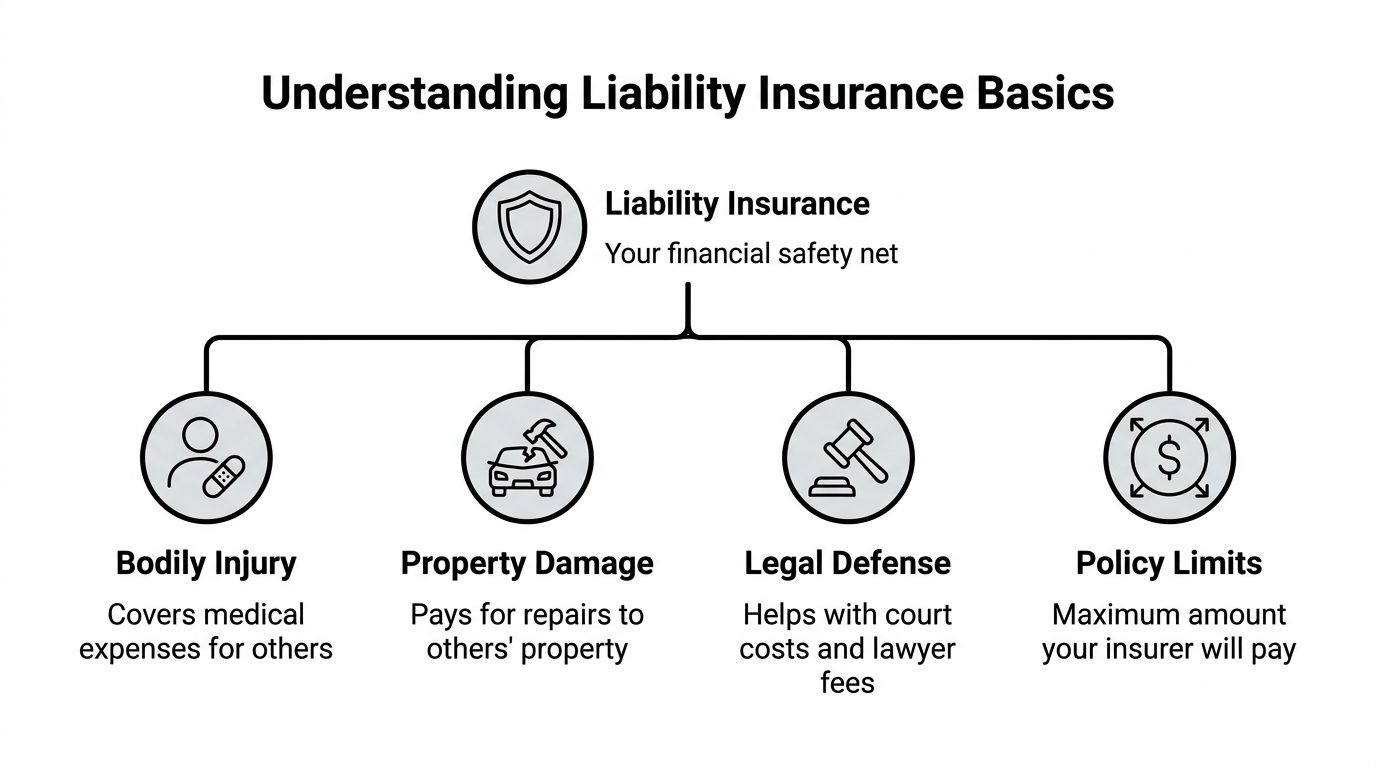

Understanding Liability Insurance Basics

Liability insurance works like a financial shield. It protects the at-fault driver or business from paying every loss out of pocket, and it creates a source of money for the injured person to pursue.

That shield has limits. It is not unlimited. It only pays up to the policy amount, and it only applies when the policy covers the event.

The two parts individuals deal with first

In a Colorado auto case, liability insurance usually has two basic pieces.

- Bodily injury liability pays for harm to people. That can include medical bills, lost wages, and other injury-related losses claimed by the person who was hurt.

- Property damage liability pays for damage to someone else’s property. In a crash, that usually means vehicle repairs or replacement, though other damaged property may also be involved.

People often confuse liability coverage with their own medical coverage or collision coverage. They are different. Liability coverage is primarily about what the at-fault party owes others.

What Colorado requires

Colorado requires drivers to carry minimum liability coverage of $25,000 per person for bodily injury, $50,000 per accident for bodily injury, and $15,000 per accident for property damage, according to the Colorado auto insurance fact sheet.

Those numbers are often written as 25/50/15.

If you were hurt and the other driver was at fault, those numbers matter because they can cap the amount available from that driver’s policy. If several people were injured in the same crash, the total bodily injury pool for everyone combined may be limited by the per-accident amount.

Where people get confused

A lot of people hear “Colorado is a no-fault state” from a friend or from old information online. It is not. If you need a quick explanation, this page on whether Colorado is a no-fault state helps clear that up.

Here is the practical version. In Colorado, fault still matters. The person or company that caused the crash is financially responsible, and liability insurance is the first place injured people usually look for recovery.

The problem with relying on the system alone

Even when coverage is legally required, not every driver follows the law. The same Colorado fact sheet reports that 16.2% of Colorado drivers were operating without insurance, ranking the state 9th highest nationally in that data set, which means uninsured drivers remain a significant threat to injured people seeking payment for their losses through the usual liability process.

So the basic rule is simple. Liability insurance is supposed to pay when someone else causes harm. The harder question is whether there is enough of it, or any of it, when you need it.

The Dangerous Gap Between State Minimums and Actual Costs

The legal minimum can sound reasonable until you compare it to the cost of a serious injury claim.

A serious collision does not produce one bill. It produces a chain of bills. Emergency transport. Emergency room care. Imaging. Follow-up visits. Specialist referrals. Physical therapy. Medication. Missed work. Sometimes surgery. Sometimes long-term cognitive or physical limitations that keep affecting income long after the vehicle is repaired.

Colorado’s minimum liability requirement creates a narrow bridge over a very wide canyon. If your injuries are minor, that bridge may be enough. If your injuries are substantial, it often is not.

Why minimum coverage runs out fast

Take a common post-crash path. A person goes to the hospital, gets diagnostic testing, follows up with doctors, misses work, and needs rehabilitation. Even before anyone starts talking about pain, suffering, permanent impairment, or future treatment, the financial loss can become serious.

That is why an injured person can be hit by someone who was “insured” and still face a major shortfall. The issue is not only uninsured drivers. It is underinsured drivers, meaning drivers whose policy exists but does not come close to covering the damage they caused.

Colorado’s underinsured risk is unusually important

Colorado drivers face a major coverage gap. The state has a 13.5% uninsured driver rate and a 40.9% underinsured rate, creating over a 50% combined risk that the at-fault driver will not have enough insurance to cover a victim’s serious injuries, according to this discussion of Colorado car insurance requirements.

That number changes how injured people should think about colorado liability insurance. The primary danger is not only that the other driver broke the law and carried nothing. It is that the other driver carried too little.

A plain-language example

A rear-end crash at highway speed can leave one person with lingering headaches, dizziness, concentration problems, neck pain, and an inability to return to work on the same timeline expected before the wreck. On paper, the at-fault driver may be fully compliant with Colorado law. In reality, the available policy money may cover only a fraction of what the injury costs.

That disconnect shocks people. They assume “insured” means “covered.” It often does not.

Signs your case may involve an underinsured driver

You may be dealing with an underinsured situation if:

- Your medical care is still ongoing and the other driver’s insurer starts talking about limits early.

- More than one person was hurt in the same crash, which can force multiple claims into one policy pool.

- Your injury affects your job and creates lost wage issues beyond immediate treatment bills.

- You have a brain injury or other long-term condition that may require future care, monitoring, or work restrictions.

Practical tip: When an insurer moves quickly to discuss settlement before your treatment picture is clear, that can signal a low policy limit rather than generosity.

What this means for your recovery

The gap between minimum limits and actual losses is the reason many injury claims become more complicated than expected. It is also why identifying every available insurance policy matters. In some cases, your claim may involve more than one layer of recovery. In others, your own policy becomes the lifeline.

The key point is simple. A valid liability policy is not the same thing as adequate compensation. Colorado law sets a floor, not a guarantee that your losses will be fully covered.

Navigating Auto Commercial and Premises Liability

Not all liability insurance is the same. The type of policy involved depends on who caused the harm, what vehicle or property was involved, and where the incident happened.

That matters because the available coverage, the investigation, and even the legal arguments can change depending on the policy type.

Three policy types people commonly encounter

| Policy type | Who usually buys it | Common example | Why it matters |

|---|---|---|---|

| Personal auto liability | An individual driver | A crash caused by a private car | Usually the starting point in a standard car wreck claim |

| Commercial auto liability | A business using vehicles for work | A delivery van or semi-truck collision | May involve company responsibility and larger policy questions |

| Commercial general liability | A business or property operator | A slip on unsafe property | Applies to bodily injury or property damage claims tied to premises or operations rather than ordinary driving |

Personal auto liability

This is the policy people picture first. A driver buys it for a personal vehicle. If that driver causes a crash, the injured person usually makes a bodily injury claim against that policy.

A standard two-car collision often starts and ends here, unless the losses exceed the available limits or another defendant is involved.

Commercial auto liability

This policy comes into play when the vehicle is tied to business activity. That could involve a company car, delivery vehicle, work truck, or commercial carrier.

Truck and business vehicle claims often raise extra questions:

- Was the driver working at the time?

- Does the employer share responsibility?

- Are there separate corporate policies?

- Did multiple businesses play a role in the trip, load, or dispatch?

A crash with a commercial vehicle is not just a bigger version of a private car claim. It often requires a broader search for policies and responsible parties.

Commercial general liability and premises claims

Some injuries do not come from a road collision at all. A person may fall on icy steps outside a business, trip over unsafe conditions at a loading area, or get hurt on commercial property connected to transportation or retail activity.

In Colorado, Commercial General Liability coverage provides occurrence-based coverage for bodily injury or property damage and is distinct from motor vehicle policies, according to the Colorado Bar article on Colorado CGL Coverage A. That source also states that average premiums for small businesses are $1,755 annually, or 19% above national averages.

The important practical point is that CGL is not the same as auto insurance. If you are hurt because of unsafe property conditions, the claim may fall under a premises or operations policy instead of a vehicle policy.

Key takeaway: The same business can have more than one liability policy. A trucking company may have a commercial auto policy for road crashes and a separate CGL policy for unsafe conditions at a yard, depot, or office.

A simple way to tell them apart

Ask what caused the injury.

- A negligent driver caused it. Start with auto liability.

- A company vehicle caused it during work activity. Look for commercial auto coverage and possible business liability.

- Unsafe property caused it. Think premises liability and CGL.

Why policy type changes the claim

Policy type affects what evidence matters. In a car crash, investigators focus on speed, lane position, signals, and impact. In a premises case, they look at maintenance, notice of a hazard, inspection practices, and the condition of the property.

It also affects who gets pulled into the case. A personal auto claim may involve one driver. A commercial matter may involve an employer, fleet owner, or business operator. A premises claim may involve a store, landlord, management company, or contractor.

For injured people, the takeaway is practical. If you are not sure what kind of liability insurance applies, do not assume it is only one policy or one defendant. The answer can shape the entire recovery path.

Your Financial Lifeline Uninsured and Underinsured Motorist Coverage

When the at-fault driver has no insurance or too little insurance, many individuals think the case is over. It is not always over. Your own policy may contain the coverage that keeps the claim alive.

That coverage is Uninsured Motorist and Underinsured Motorist coverage, often shortened to UM/UIM.

UM/UIM is different from liability insurance. Liability coverage protects others from what you may cause. UM/UIM protects you when another driver cannot fully pay for the harm they caused.

Why this coverage matters so much in Colorado

Because of the underinsured problem discussed earlier, UM/UIM is not a technical add-on. It can be the main source of recovery in a serious injury case.

Many drivers buy it without really understanding it. Some only learn what it does after a wreck, when the at-fault driver’s policy turns out to be too small.

If you want a practical overview focused on claims, this page about uninsured motorist coverage in Colorado is a useful starting point.

The anti-offsetting rule many overlook

Colorado has an especially important protection for injured people. Under Colorado Revised Statute 10-4-609, insurers cannot offset what the at-fault driver’s liability insurer paid against the injured person’s own UIM recovery, according to this explanation of why Colorado drivers need UM coverage.

In plain English, your insurer does not get to say, “You already got money from the at-fault driver, so we subtract that from your UIM coverage.”

That rule changes the math in a meaningful way.

A step-by-step example

The verified example works like this:

- The at-fault driver carries minimum bodily injury liability coverage of $25,000.

- Your total damages are $100,000.

- The at-fault driver’s insurer pays its available liability amount.

- Your own UIM coverage can apply on top of that payment rather than being reduced by it.

Before Colorado changed the law, an insurer could argue that the payment from the at-fault driver reduced what was available under your UIM coverage. Under the current rule, that reduction is not allowed in the way it once was.

The practical effect is often described as the ability to stack the coverages.

Why this matters in real cases

In a serious injury case, people often focus only on the other driver’s policy. That is a mistake. If your own UIM coverage is available, it may significantly increase the recovery pool.

This is especially important when:

- The other driver carried only minimum limits

- Your injury creates ongoing treatment needs

- You cannot return to work normally

- The crash involved long-term symptoms such as cognitive issues, chronic pain, or permanent limitations

Questions people usually ask

Is UM/UIM only for hit-and-run drivers

No. It can help in hit-and-run situations, but it also matters when the driver is identified and insured, just not insured enough.

Does my own insurer become my ally

Not automatically. Your insurer may owe coverage, but it still evaluates the claim and may dispute value, causation, or medical necessity.

If I have UM/UIM, am I guaranteed full compensation

Not necessarily. It depends on your policy terms, the amount of your losses, and the available coverage. But it can close a gap that would otherwise leave you carrying the loss yourself.

Practical tip: Ask for a full copy of your own auto policy, not just the declarations page. UM/UIM disputes often turn on language buried in the policy itself.

The planning lesson people wish they knew earlier

A lot of drivers match their UM/UIM limits to their liability limits without thinking much about it. That may feel tidy on paper, but it can leave a family exposed after a serious crash caused by someone with too little coverage.

The larger lesson is that colorado liability insurance does not tell the whole story. Recovery often depends on the interaction between the at-fault driver’s liability policy and your own UM/UIM protection. Colorado’s anti-offsetting rule makes that interaction much more favorable to injured people than many assume.

Protecting Your Rights After a Colorado Crash

The first days after a crash can shape the insurance claim more than people realize. Good medical care matters for your health, but it also creates the record that proves what the crash did to you.

Insurers build cases from documents, statements, timelines, and gaps. You should too.

What to do first

- Get medical attention promptly. If you feel dizzy, confused, numb, or increasingly sore, get evaluated. Some injuries look minor at first and become more obvious later.

- Report the crash properly. A law enforcement report can help establish basic facts, involved parties, and scene information.

- Preserve evidence early. Save photos of vehicles, visible injuries, the roadway, weather, debris, and anything else that may later disappear.

- Track your symptoms. A simple daily note about pain, sleep problems, headaches, work limitations, or missed activities can help show how the injury affects real life.

What not to do

- Do not give a recorded statement lightly. The other side’s insurer may ask questions in a way that locks you into an incomplete account before diagnosis is clear.

- Do not rush into a settlement. Early offers often come before the full medical picture develops.

- Do not assume the insurer will gather everything for you. Missing records and missing context often hurt the injured person, not the carrier.

- Do not minimize your symptoms. People often say “I’m okay” at the scene out of shock or politeness. That sentence can resurface later.

Ask for the insurance information that matters

Colorado law gives claimants an important tool. House Bill 19-1283, effective January 1, 2020, requires insurers to disclose liability policy information within 30 days of a written request from the claimant or the claimant’s attorney, including policy limits and certain other coverage details, according to this explanation of Colorado House Bill 19-1283 and insurance disclosure.

That same source says the law can accelerate settlement timelines by 20% to 30% in underinsured scenarios because the parties can evaluate the coverage picture earlier.

Delay is expensive for injured people. You may be trying to plan treatment, evaluate UIM issues, or decide whether the available liability limits are enough to justify broader litigation.

A practical checklist for the next week

- Create a claim folder: Keep crash photos, the police report, medical visit summaries, work notes, and insurer letters together.

- List every insurer involved: That can include the at-fault driver’s carrier, your own carrier, a commercial carrier, or a business insurer.

- Request policy information in writing: Written requests create a paper trail.

- Watch your deadlines: Insurance and legal deadlines are not always the same.

Key takeaway: The faster you identify the available coverage, the faster you can decide whether the case is a simple liability claim or a more complex underinsured claim.

When legal help becomes especially important

Some claims are manageable. Others stop being simple quickly. If the crash involved a commercial vehicle, severe injury, disputed fault, multiple injured people, or possible UM/UIM exposure, the insurance questions usually get more complicated.

At that point, the issue is not just whether someone has insurance. It is whether the right requests were made, the right policies were identified, and the claim was valued with the long-term picture in mind.

Why You Need an Advocate Against Insurance Companies

Insurance companies do not approach your claim the way you approach your recovery.

You are focused on healing, paying bills, protecting your job, and figuring out what your life looks like after the crash. The insurer is focused on evaluating exposure, controlling payout, and closing the file.

That difference matters.

Why self-representation gets harder over time

At first, a claim can look straightforward. Then the complications start. The adjuster questions treatment. A prior injury is raised. The crash is blamed for less than all of your symptoms. A low offer arrives before you know whether you will need future care.

Those are not random developments. They are part of a system built to test, narrow, and reduce claims.

If you want a plain-language explanation of that dynamic, this article on why insurance companies deny liability is helpful.

What an advocate does

A lawyer in this space is not only filing lawsuits. The primary work often starts much earlier:

- identifying all available insurance

- requesting policy disclosures

- preserving evidence

- coordinating records

- presenting damages in a way that reflects long-term impact

- handling communications so the injured person does not get boxed into harmful statements

Nares Law Group LLC, for example, contacts insurance carriers, sends representation letters, opens bodily injury claims, and obtains policy declarations and related policy documents to confirm coverage limits. Those tasks are administrative on the surface, but they often determine whether the claim starts on solid ground.

Why this can affect compensation

A rushed claim often values only the obvious losses. A well-developed claim looks at the whole picture, including ongoing treatment, future limitations, lost earning impact, and the interaction between liability coverage and UM/UIM coverage.

That is the primary reason many injured people need an advocate. It is not about making the case louder. It is about making the case complete.

If you were hurt in a Colorado car or truck crash and need help understanding insurance coverage, policy limits, or whether your own UM/UIM coverage may apply, Nares Law Group LLC offers guidance for injured people and families facing medical bills, lost wages, and pressure from insurers. A consultation can help you identify what coverage exists, what rights Colorado law gives you, and what steps may protect your recovery.