A crash changes the tone of an ordinary day in seconds. First there is noise, confusion, and that shaky feeling in your hands. Then comes the practical question every injured person asks. Who is going to pay for this?

Sometimes the answer gets worse before it gets better. The other driver says they do not have insurance. Or they hand you a card that turns out to be expired. Or they speed away, leaving you with a damaged car, a pounding headache, and no clear path forward.

That is where uninsured motorist coverage colorado becomes more than fine print on a declarations page. It becomes the difference between having a financial backstop and being left to fight through medical bills, missed work, and an insurance process that suddenly feels far more complicated than it should.

The Moment Your Crash Gets Complicated

You are standing on the shoulder after a collision. Your neck hurts. Your car door will not close correctly. The other driver looks panicked and says something like, “I’m sorry, I don’t have coverage right now.”

That moment lands hard because many assume the other driver’s insurance will handle the damage. In a fault-based system, that usually is the plan. But when the at-fault driver has no insurance, or disappears, the claim shifts toward your own policy and your own protections.

Colorado drivers face that risk more often than understood. In 2023, Colorado ranked ninth worst in the nation for uninsured motorists, with an estimated 17.5% of drivers operating without insurance, which means drivers here have about a 1-in-6 chance of being hit by someone without coverage, according to Colorado Public Radio’s report on uninsured drivers in Colorado.

Why this feels so overwhelming

The confusion comes from one basic misunderstanding. People think, “If I was not at fault, why would my own insurance matter at all?”

Because insurance has separate jobs.

One part of your policy protects other people if you cause a crash. Another part can protect you if someone else causes a crash and cannot pay. That second part is what many injured people only discover after they need it.

Key takeaway: If the person who hit you has no valid insurance, your recovery may depend heavily on what your own policy says about UM and UIM coverage.

A common real-world version

A driver runs a red light and slams into your vehicle. You go to urgent care that day, then start missing work because the pain gets worse. You expect the claim to be straightforward. A week later, you learn the driver was uninsured.

Now the questions start coming fast:

- Who pays medical bills

- Can I recover lost wages

- What if the driver fled

- What if my insurer says there is not enough proof

- What if I rejected coverage years ago and do not remember

Those are not small questions. They affect treatment decisions, family finances, and peace of mind.

The issue is not new

Colorado has dealt with uninsured driving for a long time. That matters because this is not some rare fluke claim category. It is a recurring problem on Colorado roads, and families need to know how the law responds when the ordinary claim path breaks down.

When a crash gets complicated, the right next step is not guessing. It is understanding the safety net you may already have.

Your Financial Safety Net UM and UIM Coverage Explained

Think of UM/UIM coverage as the backup insurance you buy for yourself. You hope you never need it. But if the driver who hurts you cannot pay, this coverage can step into the gap.

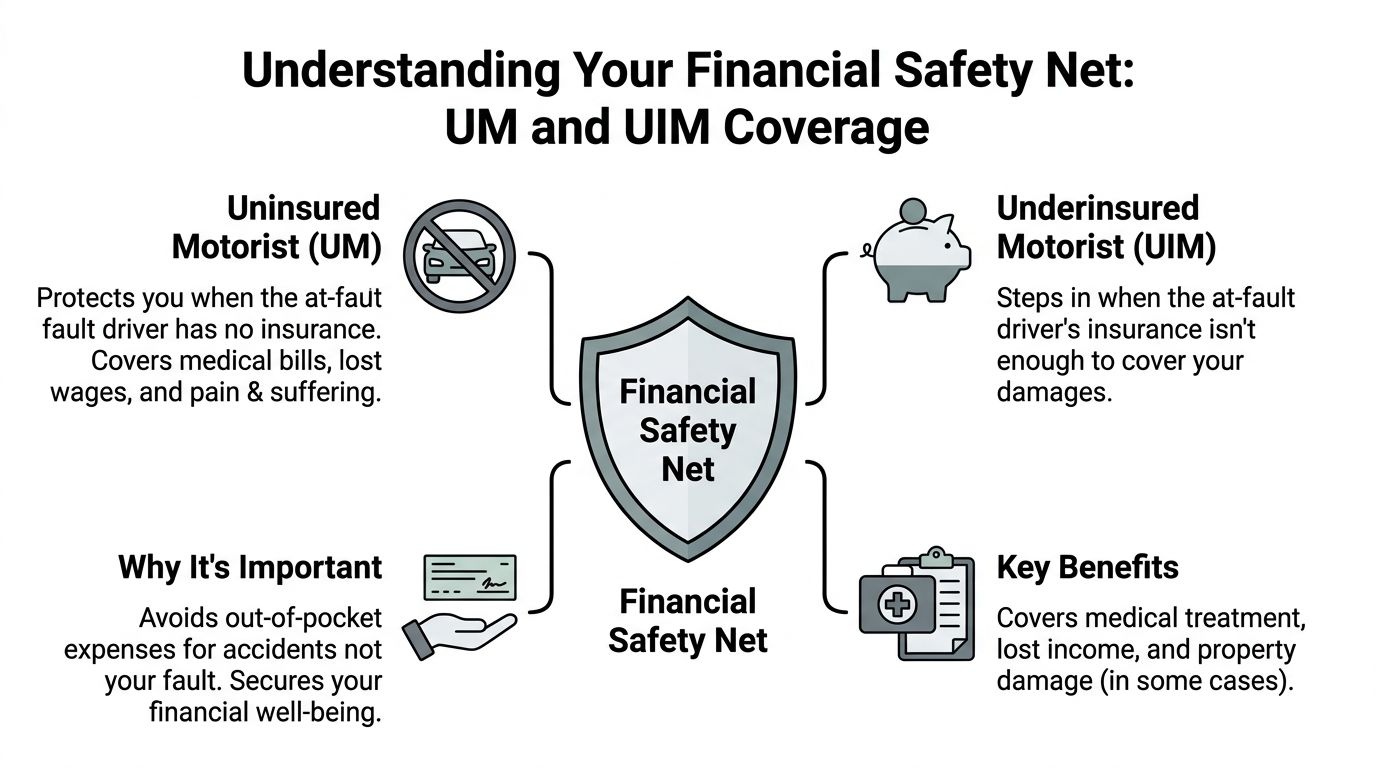

What UM coverage does

Uninsured motorist coverage, usually shortened to UM, applies when the at-fault driver has no insurance at all. It can also matter in some hit-and-run situations, which become especially important later in this article.

If another driver causes the crash and has no valid policy, UM coverage may help compensate you for bodily injury losses. In plain language, this is the part of your policy that can stand in for the missing insurance the other driver should have had.

What UIM coverage does

Underinsured motorist coverage, or UIM, applies when the at-fault driver does have insurance, but not enough to cover the full harm done.

That distinction matters. A driver can be insured and still be unable to cover a serious injury claim. If your losses are bigger than the other driver’s available liability coverage, UIM may provide another layer of protection through your own policy.

For a deeper explanation of how that second layer works, Nares Law Group has a plain-language overview of underinsured motorist insurance coverage in Colorado.

Why people mix them up

The terms sound similar, and insurers often group them together on the declarations page. That can make it seem like they are the same thing. They are related, but they solve different problems.

| Coverage type | When it usually applies | Core issue |

|—|—|

| UM | The at-fault driver has no insurance | There is no liability policy to claim against |

| UIM | The at-fault driver has insurance, but not enough | The available liability coverage runs out before your losses do |

Colorado law starts from protection, not rejection

Colorado law does something many drivers do not realize. It requires insurers to offer UM/UIM coverage to policyholders.

Under Colorado Revised Statutes § 10-4-609, insurers must offer UM/UIM coverage with limits equal to your bodily injury liability limits. If the insurer cannot prove you rejected it in writing, the coverage may be legally imposed on the policy, as explained in Cannon Law’s discussion of Colorado uninsured motorist coverage.

That rule matters because people often do not remember what they signed years ago. Sometimes they switched carriers. Sometimes they changed vehicles and renewed online. Sometimes the paperwork is incomplete. In those situations, the question becomes not just “Did you reject it?” but “Can the insurer prove that you rejected it in writing?”

What this means in practical terms

When clients hear “your own insurance may cover this,” they sometimes worry that using it feels like doing something wrong. It is not. This is coverage you purchased, or coverage the law may treat as included if the rejection was not properly documented.

Here is the practical effect:

- UM protects against a driver with no insurance

- UIM protects against a driver whose insurance is too small for the harm caused

- Colorado requires insurers to offer this protection

- A missing written rejection can become a major issue in your favor

Practical tip: Pull your declarations page before a crash ever happens. If your UM/UIM limits match your bodily injury limits, you are usually in a stronger position than someone who waived or reduced that protection.

People often think of auto insurance as protection for the other person. UM and UIM flip that idea around. They are protection for you, your passengers, and your future when another driver fails to carry enough coverage.

How Colorado Law Protects Your UM Claim

Colorado’s UM/UIM rules are more consumer-protective than many people expect. That does not mean claims are easy. It does mean the law includes tools that can make a major difference when injuries are serious and the at-fault driver’s insurance falls short.

The anti-offset rule matters more than understood

A point of confusion comes up when the at-fault driver has some insurance, just not enough. People assume their own insurer can subtract what they already recovered from the other driver and pay only the difference. In Colorado, that older approach changed.

Post-2008 revisions to Colorado law eliminated offsetting in UIM claims. That means your insurer cannot reduce your UIM payment by the amount you recover from the at-fault driver’s insurance, allowing you to access the full value of the coverage you paid for, as described in Mintz Law Firm’s explanation of Colorado UIM law.

That is a big deal in serious injury cases. If the at-fault driver’s liability coverage is exhausted early, your UIM coverage is not supposed to shrink just because you recovered that initial amount first.

Why this changes the value of your policy

Think of the at-fault driver’s policy and your UIM policy as separate buckets. Under the anti-offset rule, payment from the first bucket does not automatically empty the second.

For injured people, that can affect:

- Medical treatment decisions, especially when care continues after the first insurance payment is gone

- Lost income claims, if time away from work becomes longer than expected

- Pain and suffering recovery, when the human impact of the crash far exceeds a minimal liability policy

The written rejection issue can become its own legal battle

Another important protection sits at the policy formation stage. Colorado requires insurers to offer UM/UIM coverage in a particular way. If the carrier cannot show a valid written rejection, coverage may still be treated as part of the policy.

That changes the conversation from “You do not have this coverage” to “Show me the signed rejection.”

In practice, that can matter when:

- a policy has been renewed many times

- records are incomplete

- the insured never understood the option presented

- the carrier cannot produce the necessary paperwork

Attorney view: Some UM/UIM disputes are not really about fault in the crash. They are about whether the insurer properly offered coverage and can prove that the customer turned it down.

A brief visual explanation

This short video gives a helpful overview of how uninsured and underinsured motorist issues can affect a claim:

Where people get tripped up

The law can be protective, but the process is still adversarial once money is on the table. Your own insurer may investigate your injuries, question causation, dispute the value of treatment, or argue over policy language.

That surprises people. They think, “This is my carrier. Why are they pushing back?”

Because a UM or UIM claim turns your own insurer into the party paying the loss. Once that happens, the relationship can become more like a contested injury claim than a customer service interaction.

What to keep in mind

Colorado law helps in at least three ways:

| Legal protection | What it does for you |

|---|---|

| Mandatory offer of UM/UIM | Makes the insurer’s paperwork and proof important |

| Potential deemed coverage | May help when there was no valid written rejection |

| No offset in UIM claims | Preserves the value of coverage you purchased |

If you are badly hurt, those protections are not technical details. They can shape the entire financial outcome of the case.

Navigating a Claim After a Crash With an Uninsured Driver

The first days after a crash matter. They matter medically, because some injuries are delayed. They matter legally, because evidence disappears fast. And they matter for a UM claim because your insurer will look closely at what was documented early and what was not.

The first steps after the collision

At the scene, start with safety and medical care. Call law enforcement. Get evaluation if you feel pain, dizziness, confusion, or any symptom that could point to a head, neck, or back injury.

Then start preserving information.

A useful checklist includes:

- Photographs of everything. Vehicle damage, debris, skid marks, the roadway, nearby signs, and visible injuries.

- Driver information if available. Name, plate, contact details, and whatever insurance information the person provides.

- Witness names and numbers. Independent witnesses often become critical when fault is disputed.

- A prompt report to your insurer. Give notice that a crash occurred and that an uninsured or possibly uninsured driver may be involved.

The hit-and-run problem

Hit-and-run claims are where many people get blindsided. If the driver flees, you may assume your uninsured motorist coverage automatically applies. Sometimes it does. Sometimes the insurer challenges whether there was enough proof that another vehicle caused the crash at all.

That challenge is especially common in what people call phantom vehicle cases. Those are crashes where another driver causes the wreck but is never identified or never stops.

Why proof becomes the whole case

A key challenge in hit-and-run UM claims is the physical contact rule and proving a phantom driver existed. Without witness corroboration or physical evidence of contact, insurers may deny the claim, which is why prompt reporting and evidence collection are so important, as discussed in Fang Law Firm’s explanation of Colorado hit-and-run UM issues.

That means the evidence strategy cannot be casual.

What helps prove a phantom vehicle claim

- Independent witnesses who saw the other car cut you off, strike you, or force you off the road

- Physical damage patterns that match your account

- Debris transfer, paint transfer, or impact marks

- Police reporting made promptly, before the story can be portrayed as an afterthought

- Scene photos and nearby camera footage, including business or traffic cameras if available

If you were involved in a fleeing-driver collision, this guide on Colorado hit-and-run crashes may help you understand the next practical steps.

Important: In a phantom vehicle case, delay is dangerous. Witnesses disappear. Video gets overwritten. Road evidence gets cleared. Early documentation can determine whether the claim survives.

What to say to your insurer

Be accurate. Be concise. Do not guess.

If you do not know the answer to a question, say you do not know yet. If treatment is ongoing, say that treatment is ongoing. If you suspect a head injury, mention symptoms clearly and get medical evaluation.

You are reporting a claim, not delivering polished testimony. Precision matters more than confidence.

How the claim usually develops

A UM or UIM claim often unfolds in stages:

| Stage | What happens |

|---|---|

| Notice | You report the crash to your insurer |

| Investigation | The carrier reviews liability, coverage, and medical records |

| Documentation | You gather treatment records, wage loss proof, and evidence of pain and limitations |

| Valuation | The insurer places a number on the claim, often lower than the injured person expects |

| Negotiation or litigation | The dispute turns on fault, coverage, causation, or damages |

When the crash involved no direct impact

One of the hardest scenarios is the no-contact crash. Another vehicle swerves into your lane, you jerk the wheel to avoid a head-on collision, and you hit a guardrail while the other driver disappears.

People naturally ask, “If they never touched my car, is this still a UM claim?”

Sometimes yes. Sometimes the insurer contests it aggressively. That is why corroboration matters so much. A witness, nearby camera, or some physical evidence that supports your account can transform a doubtful file into a viable claim.

Keep your focus narrow and practical

After an uninsured-driver crash, do these things early:

- Get care

- Report the crash

- Preserve evidence

- Do not speculate

- Track every expense and missed day of work

Those simple moves often make the difference between a supported claim and a disputed one.

How to Review Your Policy and File Your Claim

Individuals often do not read their auto policy until something has gone wrong. That is normal. But once a crash happens, the declarations page becomes one of the most important documents in your household.

Start with the declarations page

Your declarations page is the summary sheet that lists coverages and limits. Look for abbreviations like UM, UIM, or UM/UIM.

Compare those entries with your bodily injury liability coverage. If the numbers match, that often means you accepted UM/UIM coverage at the same level as your liability protection. If the UM/UIM line is missing, reduced, or marked as rejected, that deserves closer review.

What to gather before filing

Do not file a bare-bones claim if you can avoid it. File a supported one.

Useful documents include:

- The crash report

- Photos from the scene

- Names of witnesses

- Medical records and bills

- Proof of missed work or reduced hours

- Repair estimates and vehicle photos

- Any communication showing the at-fault driver was uninsured or unavailable

If you need a broader overview of the injury-claim process, this guide on how to file a personal injury claim helps frame the larger picture.

What your notice to the insurer should accomplish

Your first notice does not need to prove every dollar of damage. It should do three things well:

- Identify the crash clearly

- State that an uninsured, underinsured, or hit-and-run driver may be involved

- Preserve your ability to pursue UM/UIM benefits under the policy

A short, accurate notice is usually better than an overexplained one sent in panic.

Why policy review matters in Colorado

This problem is not new. As far back as 1999, a report to the Colorado Division of Insurance estimated that 16.6% of personal automobiles, approximately 484,000 vehicles, were uninsured, according to the Colorado Uninsured Motorists Report submitted to the Division of Insurance.

That long history matters for one reason. Colorado drivers have been exposed to uninsured-driver risk for decades. Reviewing your policy is not an overreaction. It is basic financial housekeeping.

A practical policy review checklist

| What to check | Why it matters |

|---|---|

| UM/UIM listed on the declarations page | Confirms whether the coverage appears active |

| Coverage limits | Shows how much protection may be available |

| Named insureds and household drivers | Helps identify who may qualify under the policy |

| Notice requirements | Tells you how and when to report a claim |

| Endorsements or exclusions | These can affect how the insurer reads the claim |

Practical tip: Save a digital copy of your declarations page and full policy now, not after a crash. People often discover they cannot easily access old documents when they need them most.

If the insurer says you rejected UM/UIM

Ask for the written rejection. Ask for the full policy. Ask for every endorsement tied to UM/UIM.

Do not assume the insurer’s first description of your coverage is the final word. Paperwork issues matter in Colorado, and they can change the claim.

Common Pitfalls and When to Call a Personal Injury Attorney

A common scene goes like this. You report a hit-and-run, tell your insurer another vehicle forced you off the road, and expect your UM coverage to step in. Then the adjuster asks a harder question than you expected. How do we know another car caused this?

That is where many valid claims start to wobble, especially phantom vehicle cases where the other driver never made contact and never stopped. UM/UIM claims can feel personal because you are dealing with your own insurer, but the claim is still being tested like any other injury case. If the file is thin early, the insurer may treat uncertainty as a reason to pay less or deny the claim.

Mistakes that can weaken a claim

Some errors happen in the first day or two, before an injured person even realizes a dispute is coming.

- Giving a recorded statement before the facts are settled in your mind. Pain, shock, and medication can blur timing, speed, and sequence. Small gaps in an early statement often get treated as bigger credibility problems later.

- Minimizing pain at the scene or in early medical visits. Adrenaline works like a temporary mask. If your records sound mild at first, the insurer may argue the injury was mild all along.

- Treating a phantom vehicle crash like an ordinary single-car wreck. In these cases, proof is the whole case. Skid marks, debris, surveillance video, 911 calls, dashcam footage, eyewitness names, and photos of the roadway can matter as much as medical records.

- Waiting too long to gather evidence. Video gets erased. Witnesses forget details. Road conditions change.

- Taking the first settlement offer before you know the full medical picture. A quick check can feel like relief. It can also leave you paying later bills yourself.

- Assuming the adjuster’s reading of the policy is the final answer. UM/UIM disputes often turn on exact policy wording, rejection forms, and how Colorado law applies to them.

Phantom vehicle claims deserve special care. A no-contact crash can be real, but it is also easier for an insurer to question. The stronger approach is to build the file the way you would build any proof-heavy case. Start with a timeline. Identify every person who saw anything. Preserve photos, vehicle data, and app location history. Ask nearby businesses for video quickly. If law enforcement responded, request the report and check whether it accurately describes the unknown vehicle.

Signs the claim is moving into dispute

Some warning signs are subtle. Others are obvious.

Call for legal help when these issues appear

| Warning sign | Why it matters |

|---|---|

| Serious or lasting injuries | Larger claims get closer review, and low early offers can miss future care or lost income |

| Hit-and-run or phantom vehicle facts | These claims often rise or fall on evidence gathered in the first days |

| Coverage denial or reservation of rights letters | The insurer may be preparing to contest whether UM/UIM applies at all |

| Fault arguments | Reducing your share of recovery often starts with blaming your driving |

| Repeated requests for the same records or statements | The carrier may be looking for inconsistencies rather than updating the file |

| Pressure to settle before treatment is complete | Closing the claim too early can shift future costs onto you |

Why an attorney can change the path

A lawyer helps in practical ways that matter early. In a hit-and-run or phantom vehicle case, that may include securing witness statements before memories fade, preserving video, organizing a clear event timeline, reviewing whether the police report needs correction, and presenting the evidence in a way the carrier cannot easily dismiss.

An attorney also helps address a problem many people do not expect. Your UM claim may involve two separate fights at once. One is about the injury value. The other is about whether the insurer accepts that an uninsured or unknown driver legally caused the crash. Those are different questions, and each needs proof.

If the claim starts heading in that direction, it may help to speak with a firm that handles Colorado crash and insurance disputes, such as Nares Law Group LLC, or another attorney with UM/UIM litigation experience.

Attorney perspective: The best time to get legal help is often before the insurer hardens its position. Early evidence usually decides phantom vehicle claims.

Trust your instincts

If something feels off, pause and ask direct questions. What evidence is missing? What part of the policy is the insurer relying on? If the company says you rejected UM coverage, ask for the signed rejection form and every endorsement in effect on the crash date.

That is not overreacting. It is the careful response a worried driver should have when a claim could decide who carries the financial weight of the crash.

Frequently Asked Questions About Colorado UM Coverage

Does UM/UIM cover vehicle damage

Typically, UM/UIM is focused on bodily injury, not ordinary vehicle repair. Property damage is often handled through other parts of the claim, such as the at-fault driver’s liability coverage if available, or your own collision coverage. The exact answer depends on your policy language.

Does UM/UIM protect passengers

Often, yes. Coverage questions can depend on who is insured under the policy and how the policy defines covered persons. Passengers should not assume they are excluded, but they should review the policy carefully.

What if I was a pedestrian or bicyclist

UM/UIM can still become relevant in some situations, depending on the policy and the facts of the collision. The key issue is often whether you qualify as an insured person under the policy terms.

Will a hit-and-run always qualify as an uninsured motorist claim

Not always automatically. Hit-and-run claims often turn on proof. The harder it is to show another vehicle caused the crash, the more likely the insurer is to challenge the claim.

What if I cannot find my policy documents

Ask your insurer for the declarations page, the full policy, and all endorsements in effect on the crash date. Request them in writing and keep a copy of the request.

UM/UIM Coverage at a Glance

| Damage Type | Covered by UM/UIM? | Notes |

|---|---|---|

| Medical expenses | Yes | Subject to policy language and proof |

| Lost wages | Yes | Documentation from employers helps |

| Pain and suffering | Yes | Depends on the bodily injury claim |

| Vehicle repair | No | Often handled through collision or other property coverage |

| Hit-and-run bodily injury | Sometimes | Proof issues often matter |

| Pedestrian or passenger injuries | Sometimes | Depends on who qualifies as an insured under the policy |

Should I keep uninsured motorist coverage colorado on my policy

For many Colorado drivers, yes. When another person breaks the rules and cannot pay, UM/UIM may be the only realistic source of recovery for bodily injury losses. That is why this coverage matters so much in real cases, not just in policy language.

If you were hurt in a Colorado crash and an uninsured, underinsured, or hit-and-run driver is involved, Nares Law Group LLC can help you understand your policy, evaluate a denied or disputed UM/UIM claim, and take the pressure off while you focus on medical care and recovery.